- column

- STATE & LOCAL TAXES

Comparing the Value-Added Tax to the Retail Sales Tax

Please note: This item is from our archives and was published in 2008. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

State tax history at the United States’ 250th anniversary

Calculating and presenting state income tax effects under ASC Topic 740

State private letter rulings: What to consider before you ask

Editor: Scott Salmon, CPA, M. Acc.

Over the past few decades, the value-added tax (VAT) has become the fastest-growing indirect tax globally (see Schenk and Oldman, Value Added Tax: A Comparative Approach 1 (Cambridge University Press 2007)). With the exception of the United States, most countries’ fiscal authorities rely far more heavily on VAT than on any other taxes for revenue. With the pace of globalization accelerating, multinational businesses increasingly seek advice on VAT and other indirect taxes, which may constitute a large percentage of their aggregate tax liability. A recent KPMG International study shows that two-thirds of multinational companies are concerned about the complexity of VAT, and 55% are worried about their VAT compliance obligations (see “Indirect Tax Increasingly Important for Global Businesses” (May 20, 2008)).

The United States is the only member of the Organisation of Economic Cooperation and Development that does not levy a VAT on a national level; however, VAT has become widely recognized as an important option in federal tax reform debates.

In January 2005, President Bush established the bipartisan President’s Advisory Panel on Federal Tax Reform to present options to reform the Internal Revenue Code to make it simpler and more pro-growth. In November 2005, the panel issued its report, which included analysis of a VAT that could potentially replace a portion of both individual and corporate income taxes (President’s Advisory Panel on Federal Tax Reform, Simple, Fair, and Pro-Growth: Proposals to Fix America’s Tax System, 191–92 (November 1, 2005). Although the panel did not ultimately recommend the VAT proposal, it evaluated and analyzed the proposal extensively (President’s Advisory Panel on Federal Tax Reform at 191–205).

In April 2008, at the request of the House Ways and Means Committee, the Government Accountability Office issued a report that examined the VAT imposed in Australia, Canada, France, New Zealand, and the United Kingdom and described VAT compliance costs, administration, and implementation (U.S. Government Accountability Office, Value-Added Taxes: Lessons Learned from Other Countries on Compliance Risks, Administrative Costs, Compliance Burden, and Transition, GAO-08-566 (April 2008)).

A number of bills have also been introduced in the current session of Congress that, if enacted, would levy some type of VAT to replace all or part of the current federal income tax system, including a bill proposing to levy a VAT for national health insurance (see, e.g., H.R. 25 and S. 1025, Fair Tax Act of 2007; H.R. 1040, To Amend the Internal Revenue Code of 1986 to Provide Taxpayers a Flat Tax Alternative to the Current Income Tax System; S. 1111, Fair Flat Tax Act of 2007; S. 1040, Tax Simplification Act of 2007; H.R. 5105 and S. 2547, Fair and Simple Tax Act of 2008; H.R. 4159, Simplified USA Tax Act of 2007; S. 1081, Flat Tax Act of 2007; and H.R. 15, National Health Insurance Act). Despite these numerous proposals, the U.S. government has given no indication that it will soon move to a VAT system.

Most U.S. taxpayers are unfamiliar with VAT. On the state and local level, only New Hampshire, with its business enterprise tax, currently imposes a VAT-type tax. That tax is assessed on the enterprise value tax base, which is the sum of all compensation paid or accrued, interest paid or accrued, and dividends paid by the business enterprise, after special adjustments and apportionment. Until January 1, 2008, Michigan also used a value-added type tax called the single business tax.

What is well known in the United States is the general sales and use tax or retail sales tax currently imposed by all states and the District of Columbia, with the exception of Alaska, Delaware, Montana, New Hampshire, and Oregon.

This column explores the similarities and differences between the VAT and retail sales tax systems. To set the groundwork for this comparison, it will first analyze the typical VAT system.

Overview of VAT

More than 130 countries use VAT as a key source of government revenue (Schenk and Oldman at 459–62). VAT is a general, broad-based consumption tax assessed on the value added to goods and services. VAT is generally levied on value added at every stage of production, with a mechanism allowing the sellers a credit for the tax they have paid on their own purchases of goods and services (input tax) against the taxes collected on their sales of goods and service (output tax). Generally, VAT is:

- A general tax that applies to all commercial activities involving the production and distribution of goods and the provision of services;

- A consumption tax ultimately borne by the consumer;

- An indirect tax levied on the consumer as part of the price of goods or services;

- A multistage tax visible at each stage of the production and distribution chain; and

- A fractionally collected tax that uses a system of partial payments whereby a seller charges VAT on all of its sales with a corresponding claim of credit for VAT that it has been charged on all of its purchases (Ebrill et al., “The Allure of the Value-Added Tax,” 39 Fin. and Dev. (June 2002)).

There are three methods of calculating VAT liability: the credit-invoice method, the subtraction method, and the addition method (Schenk and Oldman at 38). This column deals with only the credit-invoice method, which is the most widely used.

The credit-invoice method highlights the VAT’s defining feature: the use of output tax (tax collected on sales) and input tax (tax paid on purchases). A taxpayer generally computes its VAT liability as the difference between the VAT charged on taxable sales and the VAT paid on taxable purchases (Schenk and Oldman at39). This method requires the use of an invoice that separately lists the VAT component of all taxable sales. The sales invoice for the seller becomes the purchase invoice of the buyer. The sales invoice shows the output tax collected and the purchase invoice shows the input tax paid. To summarize, taxpayers use the credit-invoice method to calculate the amount of VAT to be remitted to the taxing authorities in the following manner:

- Aggregate the VAT shown in the sales invoices (output tax);

- Aggregate the VAT shown in the purchase invoices (input tax);

- Subtract the input tax from the output tax and remit any balance to the government; and

- In the event the input tax is greater than the output tax, generally a refund is due.

General VAT Computation

To see VAT in action, consider Exhibit 1, which provides a simple illustration of how VAT is implemented in the production of bread. A farmer grows and sells wheat to a miller, who grinds the wheat into flour. The miller sells the flour to a baker, who makes the dough and bakes the bread. The bread is then sold to the grocer, who sells the bread to the final consumer. In each stage of bread production, value is added by the seller, and VAT is levied on that amount.

To ensure that VAT is levied only on the value added by the producer, VAT uses the credit-invoice mechanism. Thus, on selling the bread to the grocer, the baker collects $30 in VAT and claims an input credit of $15, the VAT paid when the baker purchased flour from the miller. The baker ends up remitting a net VAT liability of $15 to the tax authorities. The total revenue created by VAT is the sum of VAT liability collected in each stage of bread production, in this case $50.

Although VAT is a broad-based general consumption tax (i.e., it applies to all final consumption), there are instances when the application of VAT is avoided. For example, in a pure VAT state, the tax base would theoretically include services rendered by the government, isolated sales of one’s personal effects, and sales of personal services; however, no nation employs a VAT with this tax base for administrative, political, or social reasons (Schenk and Oldman at 46). Thus, VAT provides exemptions or applies zero tax rating to certain transactions. “Exemption” means that the trader does not collect VAT on its sales and does not receive credits for VAT paid on its purchases of inputs. “Zero rating” means that a trader is liable for an actual rate of VAT, which happens to be zero, and receives credit for input VAT paid. Like transactions, potential taxpayers can be exempt or zero rated. An exempt trader is not part of the VAT system and is instead treated as a final purchaser. A zero-rated business does not collect VAT on sales but is compensated for any input VAT it pays.

VAT Computation with Exemption

The effect of exemption or zero-rate transactions on the VAT revenue and the tax burden depends on where in the production process the exemption or zero rating occurs. To demonstrate how the exemption and zero rating generally work and their potential effect on VAT revenue and tax burden, consider Exhibits 2 and 3, which are based on the value-added output tax and input tax presented in Exhibit 1.

As shown in Exhibit 2, if the exemption occurred in the middle of the production process, it would have the counterintuitive effect of increasing the VAT revenue and the tax burden compared with Exhibit 1. If the miller is exempt from VAT, then the miller would not collect VAT from its sales to the baker and would not be able to claim the $5 input tax it paid to the farmer. Compared with the total VAT revenue in Exhibit 1 ($50), the total VAT revenue raised in Exhibit 2 increases by $5. The reason is that the value added by the farmer ($50) is taxed twice, once at the farmer’s stage of production (before the exemption) and again at the baker’s stage of production (after the exemption).

Note also that the baker’s tax burden increases by $15 ($30 minus $15), which corresponds to the tax on the value added by the farmer (taxed the second time ($5)) plus the tax on the value added by the miller ($10), which is not paid by the miller. An exemption from tax generally decreases the tax revenue because no tax is collected from an exempt transaction. However, this does not apply to the example in Exhibit 2 because an exemption occurring at one stage of production (the miller) would mean shifting and increasing the tax burden to the next stage of bread production (the baker). This example shows that if the chain of input credits is broken, overtaxation can occur.

The counterintuitive effect of increasing the VAT revenue and the tax burden would also result if the exemption occurred at the baker’s stage of production because of the break in the chain of input credits. Exemption at the first stage of production (the farmer) would be tax neutral because there is no break in the chain of input credits. The chain would just start on the baker’s stage of production (after the exemption).

However, if the exemption occurs at the last stage of production, there is a corresponding decrease in VAT revenue because there is no shifting and increase of tax burden; the value added at the final stage simply escapes from VAT. As shown in Exhibit 3, exempting the grocer from VAT means the grocer would not collect VAT and would not be able to claim credit for the tax it paid on its purchase. The exemption at the last stage means that the grocer would become the final consumer of the bread. As a final consumer, the grocer would pay the VAT as part of the purchase price. No shifting and increase of tax burden would occur because the grocer would not be able to pass on the tax it paid from its input. An exemption occurring at the last stage of production means that the chain of input credits would cease at the stage prior to the last stage (the baker’s stage). Any value added after the baker’s stage would simply escape the VAT, resulting in a decrease in government revenue due to the exemption.

VAT Computation with Zero Rating

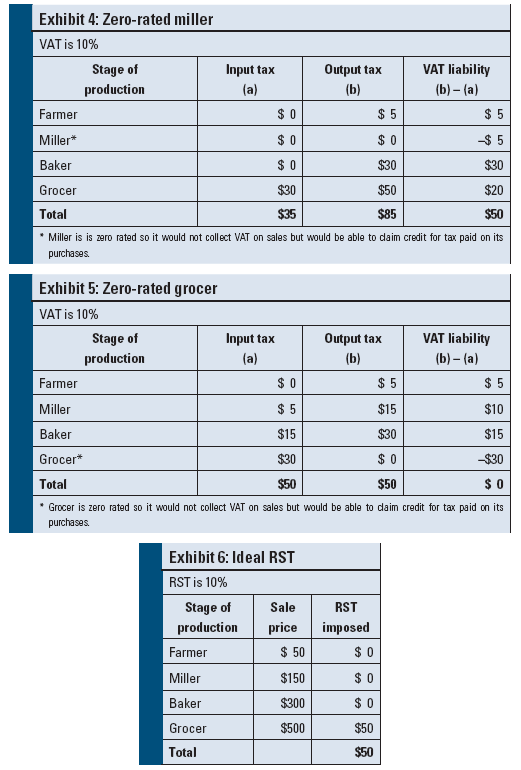

Exhibit 4 shows that if zero rating occurred at the middle of the production process, the total VAT revenue would be the same because there would be no break in the VAT chain. VAT revenue would be the same if the zero rating occurred at the farmer’s or baker’s stage of production. The miller would not charge VAT on its sales but would get credit for the VAT it paid from the farmer (the miller would be entitled to a refund). The VAT not charged by the miller would be picked up by the baker, thereby continuing the VAT chain—that is, the baker would still continue to claim credit for the tax it paid from its input. The increase in the baker’s VAT liability is due not to an increase in tax burden but to an unavailability of input tax to credit against its output tax. This example shows that a zero rating in the middle of the production process does not affect the total revenue of the VAT system.

The same is not true, however, if the zero rating occurs at the end of the production process. As depicted in Exhibit 5, having a zero-rated grocer would reduce the total VAT liability and revenue to zero because all the value added throughout the production process would be credited back to the grocer. The grocer in this example would be entitled to a $30 refund representing the input tax it paid to the baker.

Overview of Retail Sales and Use Tax

Before considering some of the similarities and differences between VAT and the retail sales tax (RST), this column next considers a typical retail sales tax system. The retail sales and use tax imposed by U.S. states is generally levied on all retail sales of tangible personal property that are not explicitly exempted. For services, only those explicitly enumerated are taxable (Hellerstein and Hellerstein, State Taxation ¶12.04[1] (Warren, Gorham and Lamont 1998)). The tax is generally stated on the sales receipt and is collected from the consumer at the point of sale. The retailer is responsible for remitting the tax collected to the tax authorities.

In theory, retail sales tax is a single-stage tax imposed on the ultimate consumer, which means that the tax should apply only to final sales for personal use and consumption (Hellerstein and Hellerstein at ¶12.01). Accordingly, intermediate transactions in the economic process are excluded from the scope of the sales tax. Using the same bread production example above, sales tax would be imposed only on the final stage of production as the grocer is selling the bread to the ultimate consumer (see Exhibit 6).

However, under the U.S. sales tax system, the general sales tax is not confined to transfers to ultimate consumers of final products manufactured in the economic process (Hellerstein and Hellerstein at ¶12.01). For example, absent an exemption, sales tax is imposed on the baker’s purchases of supplies for the trucks it uses to deliver the bread to the grocer. The reason behind the taxation is that the truck supplies do not form part of the bread and the baker is considered the ultimate consumer of the supplies (see Exhibit 7). However, to achieve some semblance of a balanced retail sales tax, many states’ sales taxes exclude or exempt many intermediate transactions. These exclusions or exemptions include, but are not limited to, the following: (1) sales for resale; (2) sales of components or ingredients of property produced for sale; (3) sales of property consumed in the manufacture or production of goods for sale; (4) sales of manufacturing machinery and equipment; and (5) sales of containers and packaging.

VAT vs. Sales Tax

Some of the differences between VAT and retail sales tax are summarized and enumerated in Exhibit 8. One major difference between the VAT and retail sales tax systems is the treatment of intermediate transactions. For VAT, any intermediate transaction within the bread production process would not be subject to a net VAT liability because any tax paid (whether involving capital, goods, or services) would be claimed back through the input tax mechanism inherent in the VAT system. If the baker paid VAT on supplies it purchased for its trucks, the baker would be able to use the tax paid as input tax credit against its output tax liability even though the supplies do not form part of the final product (see Exhibit 1 in general).

As a corollary to the application of input tax credit, VAT has a broad-based application that taxes not only the sale of goods but also the sale of services, thus ensuring that most intermediate transactions would have an input tax component that could be used to reduce the taxpayer’s net VAT liability. Zero rating would also contribute to the application of the input tax credit for intermediate transactions (see Exhibits 4 and 5 and the corresponding discussion). The input tax mechanism, however, would not apply in cases in which the intermediate transaction involved an exempt transaction, when taxation would occur twice (see Exhibit 2 and the corresponding discussion).

{kind=link}

Although retail sales tax excludes or exempts many intermediate transactions, the application of these exclusions or exemptions is limited. If the intermediate transaction does not fall under the limited exclusion or exemption, it will be subject to sales tax. In the example given in Exhibit 7, the baker’s purchase of supplies not related to the production of bread would be subject to sales tax. The tax incurred by the baker would likely be passed forward by the baker to the grocer through an increased sales price. This could have a potential tax cascading effect (i.e., tax on tax).

Another difference, at least with respect to a credit-invoice VAT and the retail sales tax, is the dependence on supporting documents for efficient administration. Under the credit-invoice method VAT, an entity is required to maintain supporting documentation to substantiate its claim for input tax credit (Schenk and Oldman at 40). The invoice shows the VAT paid in a particular transaction. A VAT shown on a sales invoice of one entity would be the same as the VAT shown on the purchase order of another. Thus, each firm relying on the invoice has a vested interest in receiving an invoice and making sure that the VAT stated on the invoice is not understated so the entity can properly receive full credit against its VAT liability. Thus, the credit-invoice VAT seems to be self-policing.

The retail sales tax’s main policing mechanism involves the use of exemption certificates to identify exempt transactions. The purpose of the exemption certificate is to relieve the seller of its obligation to collect sales tax. In most states, if a purchaser claiming an exemption issues a properly executed exemption certificate to the seller, the seller is absolved of liability, provided that the certificate was accepted in good faith. In this case, generally only the seller has a vested interest in the exemption certificate being properly issued by the purchaser.

Conclusion

In general, both the VAT system and the retail sales tax system, using the same tax rate, would be considered equivalent in terms of revenue raised. Thus, in the examples discussed above, the entire bread production would result in $50 in VAT, and the grocer selling the bread to the consumer for $500 would result in $50 in retail sales tax (see Exhibits 1 and 6). The similarity ends there because in actual practice, VAT and retail sales tax would likely ultimately produce different tax results (see Exhibits 2-3, 4-6, and 7).

{kind=link}

{kind=link}

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser. This article represents the views of the author only and does not necessarily represent the views or professional advice of KPMG LLP. ©2008 KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

EditorNotes:

Scott Salmon is a partner in KPMG LLP in its Washington National Tax Practice in Washington, DC. He is immediate past chair of the AICPA Tax Division’s State & Local Taxation Technical Resource Panel. Benedict Cabaltica is a manager in the KPMG LLP Washington National Tax State and Local Tax Group in Washington, DC. For more information about this column, contact Mr. Cabaltica at bcabaltica@kpmg.com.