- column

- TAX PRACTICE RESPONSIBILITIES

Practitioners’ Responsibilities in Complying With Records Requests

Please note: This item is from our archives and was published in 2014. It is provided for historical reference. The content may be out of date and links may no longer function.

Related

IRS raises standard mileage rates for remainder of 2026

IRS designates certain CRAT arrangements as listed transactions

Eligible taxpayers to get automatic IRS penalty relief

Editor: Thomas J. Purcell III, CPA, J.D., Ph.D.

It is common for a tax practitioner to gain new clients. However, that likely means another tax practitioner is losing a client. The turnover of clients is one of the primary reasons a client will request the return of tax records from a CPA. Other possible reasons might include a pending lawsuit or the need to provide financial or tax records to a bank to obtain financing.

When responding to such requests, the tax practitioner must be cognizant of, and adhere to, the collective body of applicable professional standards and law, including the AICPA Code of Professional Conduct (AICPA Code); Treasury Circular 230, Regulations Governing Practice Before the Internal Revenue Service (31 C.F.R. Part 10); the authority of applicable state boards; and the Internal Revenue Code. A practical consideration is whether the CPA must comply with a request before being compensated for services already provided to the client.

This column examines the interplay of the aforementioned standards, including key definitions of the types of records that may be in a client’s file. In addition, this column provides practical guidance in responding to such requests. In this column, any reference to a “client” includes either a current or a former client, and a request for records includes a request for records to be provided either to the client directly or to a successor tax practitioner. “CPA” refers to an individual who has an active license to practice and thus is covered by Circular 230. Unless otherwise indicated, a CPA is also assumed to be a member of the AICPA.

Analysis of the AICPA Code

The AICPA Code and related Interpretations address the responsibilities of Institute members (and, by reference, of practitioners in those states where the governing board of accountancy has incorporated the AICPA Code into the state-specific code of conduct) when they perform professional services. Interpretations of the AICPA Code are adopted by the professional ethics division’s executive committee to provide guidelines on the application of the rules.

Rule 501, Acts Discreditable, states that “[a] member shall not commit an act discreditable to the profession.” Interpretation ET Section 501-1, “Response to Requests by Clients and Former Clients for Records,” guides a member in how to respond to a client’s request for records. The following terms are defined solely for use with Interpretation ET Section 501-1:

- The term “client” includes current and former clients.

- “Client-provided records” are accounting or other records belonging to the client that were provided to the member by, or on behalf of, the client, including hard copy or electronic reproductions of such records.

- “Member-prepared records” are accounting or other records that the member was not specifically engaged to prepare and that are not in the client’s books and records or are otherwise not available to the client, with the result that the client’s financial information is incomplete. Examples include adjusting, closing, combining, or consolidating journal entries (including computations supporting such entries) and supporting schedules and documents that are proposed or prepared by the member as part of an engagement (e.g., an audit).

- “Member’s work products” are deliverables as set forth in the terms of the engagement, such as tax returns.

- “Member’s working papers” are all other items prepared solely for purposes of the engagement and include items:

•Prepared by the member, such as audit programs, analytical review schedules, and statistical sampling results and analyses, and

•Prepared by the client, at the request of the member and reflecting testing or other work done by the member.

Note that Rule 501 was promulgated primarily from an auditing engagement perspective. As such, it is at times difficult to interpret and apply in tax situations.

A member’s failure to comply with a client’s request for a return of client records could constitute a violation of Rule 501 as an act discreditable to the profession. Client-provided records include both original and electronically reproduced documents that the client provided directly to the member or that were provided on behalf of the client and include documents prepared by the client, client employees, or a third party. Examples of client-provided records are general ledgers; trial balances; asset purchase or sale documents; brokerage statements; Forms W-2, Wage and Tax Statement; and receipts for charitable contributions.

When a client requests member-prepared records or work products that are in the member’s custody, the requested documents (copies of the originals should suffice) should generally be provided to the client, unless the member and client have agreed otherwise. As ET Section 501-1 indicates (see below), there is some flexibility in the format of the documents that must be provided.

In several situations, member-prepared records related to a completed and issued work product may be withheld:

- If fees are due to the member for the specific work product;

- If the work product is incomplete;

- For purposes of complying with professional standards (e.g, withholding an audit report due to outstanding audit issues); or

- If threatened or outstanding litigation exists concerning the engagement or member’s work.

ET Section 501-1 acknowledges that a member’s working papers are the member’s property and does not require a member to provide those records to the client; however, state or federal statutes and regulations or contractual agreements may require the member to do so.

Additional guidance outlined in ET Section 501-1 states:

- Once the member has complied with outlined requirements, the member is generally not obligated to respond to a client’s repeated requests for the records.

- The member may charge the client a reasonable fee for retrieving and reproducing the records and may require the fee to be paid before releasing the records.

- Although the member is not required to convert records to an electronic format or convert from one electronic format to another electronic format, the member is encouraged to comply with the client’s request for a specific format if the format is available.

- The member may retain copies of any records provided to the client.

- The member should comply with the client’s request in an expedient manner but generally within 45 days after the request is made.

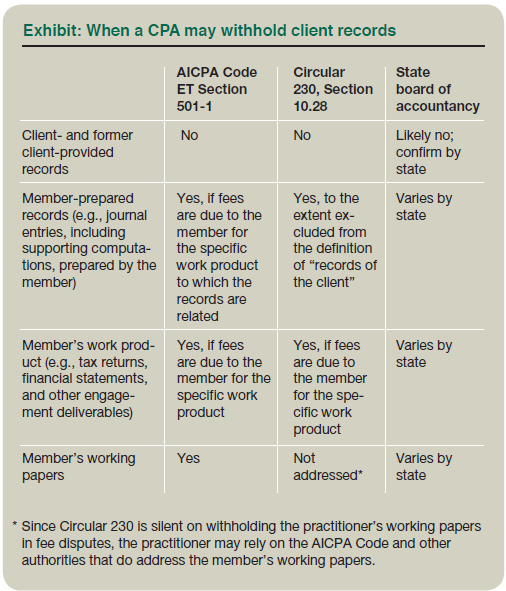

Since tax practitioners are governed by several sets of ethical rules, requests for client records are more complex in the tax engagement. The different rules do not provide consistent standards for tax practitioners in responding to client requests. Many times, the client has not paid for the professional services, and the CPA may wish to withhold requested records until the client pays the unpaid professional services invoices. This exhibit summarizes the rules in these situations.

{kind=link}

Analysis of Circular 230

Circular 230 applies to professionals who practice before the IRS. Section 10.28(a) of Circular 230 generally requires a practitioner to promptly return all “records of the client” necessary for the client to comply with his or her federal tax obligations. Records of the client include:

- All documents or materials, written or electronic, provided to the practitioner or obtained by the practitioner in the course of representing the client, which preexisted the client’s retention of the practitioner;

- Materials prepared by the client or a third party (other than an employee or agent of the practitioner) at any time and provided to the practitioner; and

- Any return, claim for refund, schedule, affidavit, appraisal, or any other document prepared by the practitioner, including employees or agents, that was previously provided to the client if the document is necessary for the taxpayer to comply with his or her current federal tax obligations (Circular 230, §10.28(b)).

However, “records of the client” do not include any return, claim for refund, schedule, affidavit, appraisal, or any other document prepared by the practitioner or the practitioner’s firm pending the client’s fulfillment of his or her contractual obligation to pay fees with respect to the document.

A dispute over fees does not generally relieve the practitioner of his or her responsibility to return client records, as previously defined. If applicable state law allows the practitioner to retain a client’s records in the case of a fee dispute, the practitioner must return the records that must be attached to the taxpayer’s return. However, the practitioner must provide the client with access to review and copy additional records of the client that are necessary for the client to comply with his or her federal tax obligations.

Example 1: M, CPA, has been engaged by client J to prepare J’s 2013 individual federal and state income tax returns. Since not all of J’s Forms K-1 were received by the original filing deadline, J agreed that M should file an application to extend the returns, and valid extensions were filed. After the extensions were filed but before the returns were completed, J informs M that he is moving his account to Whitney CPA firm, which will complete J’s 2013 tax returns. M agrees and submits an invoice for the time incurred to extend the 2013 returns. J fails to pay the invoice. J requests the return of (1) the documents he provided (e.g., Forms W-2, 1099, 1098, etc.); (2) the extension calculation; and (3) Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. M is a CPA and a member of the AICPA.

M prefers to return the minimal number of documents that fulfill her professional responsibilities until J pays the invoices. What documents, if any, may M withhold until she receives payment from J?

As a CPA and a member of the AICPA, M is subject to the requirements of the AICPA Code and Circular 230. Both governing bodies will generally require M to return the documents (e.g., Forms W-2, 1099, 1098, etc.) that J provided to her to be used in preparing his return (and extension).

Under AICPA Code ET Section 501-1, the extension calculation that M prepared would likely be considered the “member’s working papers,” as it was prepared by M in support of the final work product, which in this case is the extension, Form 4868. The member’s working papers are the member’s property and do not need to be provided to the client unless a requirement is imposed by state or federal authority or by contractual agreement. Circular 230 does not include the practitioner’s working papers in the definition of “records of the client” and thus should not prevent M from withholding the extension calculation until she receives payment from J.

If applicable state statutes and regulations permit her to withhold the extension calculation, she may do so until she receives payment or permanently, since she is under no compunction by the applicable professional standards to release it.

The extension itself, Form 4868, would likely meet the definition of “member’s work product” under ET Section 501-1 and, thus, could be withheld for payment of the invoice related to the extension. Circular 230 also allows M to withhold the extension for payment, as the term “records of the client” provides an exception for any return or other document prepared by the practitioner pending the client’s fulfillment of his or her contractual obligation to pay fees with respect to the document. If applicable state statutes and regulations permit her to withhold the extension, she may do so until she receives payment. Note that, although Form 4868 is not a “return” for purposes of Circular 230, it is an “other document” and thus covered.

Example 2: Assume the same facts as in Example 1, except that J has paid the invoice related to the 2013 extension but failed to pay an invoice for his 2012 tax return. What documents may M withhold pending payment for preparation of the 2012 tax return?

Since the unpaid invoice does not relate to the documents the client is requesting, M would have no basis to withhold the extension Form 4868 under ET Section 501-1 and Circular 230. The analysis regarding the extension calculation remains constant, and she could withhold or provide it at her discretion. Note that M would have more leverage for payment if she had negotiated for payment of the 2012 return before commencing the 2013 tax work. The reasons for her failure to do so are irrelevant to the issue at hand and beyond the scope of this column.

Example 3: C, CPA, prepares and delivers the 2013 federal and state income tax returns for W Inc. However, W is disputing the amount invoiced for the return preparation and has notified C that it will be using P, CPA, for future services. L, the president of W, calls C and demands copies of C’s working papers to provide to P. Must C provide a copy of the W engagement working papers?

Generally, C does not have to provide copies of the W working papers as long as the fee dispute is unresolved. However, if the working papers contain any information that was previously presented to W that it needs to fulfill its future tax obligations, that information should be provided to W as required under Section 10.28(b) of Circular 230. This would include items such as tax depreciation schedules and tax inventory records prepared by C in the course of the engagement.

Example 4: Assume the same facts as Example 3 and that C used SuperTax software to prepare the return. P, the successor accountant, also uses SuperTax software, and W has requested a copy of the data file. Must C provide a copy of the SuperTax file to W?

There is no specific requirement that C provide a copy of the SuperTax file. However, if the SuperTax software was used to maintain W’s tax depreciation records, there would be a requirement to provide the file under Section 10.28(b) of Circular 230 and AICPA Code Interpretation 501-1. Section 10.28(b) provides that “[r]ecords of the client include . . . any return, claim for refund, [or] schedule . . . prepared by the practitioner . . . that was presented to the client with respect to a prior representation if such document is necessary for the taxpayer to comply with his or her current Federal tax obligations.” It appears that the depreciation records maintained using the SuperTax software would fall within this definition. Further, AICPA Code Interpretation 501-1 states that, with respect to member-prepared records or members’ work products, “The member is not required to convert records that are not in electronic format to electronic format. . . . However, if the client requests records in a specific format, and the records are available in such format within the member’s custody and control, the client’s request should be honored.” Considering Section 10.28(b) and Interpretation 501-1 together, it appears that C should furnish a copy of the SuperTax file to W if the depreciation records are maintained within the file.

Other Matters to Consider Before Releasing Client Records

Before releasing client records, the practitioner should consider and discuss with the client any concerns about the possible compromise of confidentiality under Sec. 7525, the Kovel doctrine (296 F.2d 918 (2d Cir. 1961)), or similar issues. In addition, if the records are being provided directly to a third party at the client’s behest, the CPA should be certain to comply with Sec. 7216.

Although not required by either the AICPA Code or Circular 230, it is advisable to consider documenting the request and release of client records in the member’s files to prevent misunderstandings between the client and practitioner. The practitioner may consider providing the client with a letter (to be returned to the practitioner) for the client’s signature, acknowledging receipt of the documents being requested by the client, the purpose of the request (e.g., for preparation of the client’s 201X tax returns), and the possible compromise of confidentiality. Some practitioners have involved legal counsel in drafting such letters, which may also include language protecting the rights of the practitioner, particularly when releasing the practitioner’s working papers.

Before releasing records, the practitioner should consider whether any conflicts of interest exist, such as a divorced or separated couple who have previously filed joint returns, that would require the practitioner to receive additional permission to release records from a party other than the requesting party. A conflict of interest may be an issue if the requested records are for an entity. The member should make certain that the requesting individual is an authorized person (i.e., officer of a corporation or general partner of a partnership) since the client is the entity, as opposed to the requesting individual. (See Mathers and Schrock, “Practical Approaches to Common Conflicts of Interest,” 45 The Tax Adviser 360 (May 2014), for a deeper discussion of matters relating to conflicts of interest.)

If a client requests that the records be provided to a successor tax practitioner (or anyone other than the client), the practitioner will need to comply with Sec. 7216; Regs. Secs. 301.7216-1 through 301.7216-3; and Rev. Proc. 2013-14, as modified by Rev. Proc. 2013-19. The member should also consider the need to have the successor sign a release indicating that the member will not be liable for the future use of any information contained in the records. (For more guidance, see Bond and Schreiber, “Current Tax Return Disclosure Issues Involving Sec. 7216,” 44 The Tax Adviser 546 (August 2013).)

Summary

A practitioner must adhere to multiple bodies of authority when responding to a client’s request for records. Knowledge of the relevant sections of the AICPA Code, Circular 230, and applicable state(s) public accounting statutes and regulations, as well as the interplay of Sec. 7216, will enhance the practitioner’s ability to effectively respond to a client’s request while protecting the practitioner’s rights to payments for services rendered.

Notes: A revised AICPA Code of Professional Conduct will become effective Dec. 15, 2014 (and practitioners can choose to implement it earlier). Rule 501, Acts Discreditable, discussed in this column, will become Rule 1.400.001 in the revised code. Interpretation ET Section 501-1, “Response to Requests by Clients and Former Clients for Records,” will be Section 1.400.200.02 in the revised code.

State professional codes of conduct for accountants and tax practitioners can generally be accessed through each state’s respective board of accountancy website. The National Association of State Boards of Accountancy provides contact information for each board. State laws and regulations can be accessed through each state’s respective website.

| Contributors | |

| Thomas Purcell is a professor of accounting at Creighton University in Omaha, Neb. Kristy Rempalski is a partner with the National Tax Office of Crowe Horwath LLP. James Sansone is a regional director of Tax Quality and Risk Management with McGladrey LLP. Prof. Purcell, Ms. Rempalski, and Mr. Sansone are members of the AICPA Tax Practice Responsibilities Committee. For more information about this column, contact Ms. Rempalski at kristy.rempalski@crowehorwath.com or Mr. Sansone at james.sansone@mcgladrey.com. |