The impact of filing status on student loan repayment plans

EXECUTIVE | |

|

The volume of student loans continues to grow, as the number of borrowers and the amounts borrowed have increased significantly over the past decade. During the 2018-2019 academic year, the federal government issued $76 billion in new student loans to 7.6 million students.1 As of December 2019, outstanding student loans issued or guaranteed by the federal government totaled $1.5 trillion.2

The volume of student loans continues to grow, as the number of borrowers and the amounts borrowed have increased significantly over the past decade. During the 2018-2019 academic year, the federal government issued $76 billion in new student loans to 7.6 million students.3 As of December 2019, outstanding student loans issued or guaranteed by the federal government totaled $1.5 trillion.4

Income-driven repayment plans are available for federal student loans for borrowers incurred after a certain date. The plans take into account family size and income and generally limit payments to 10% of discretionary income (defined below), but no more than the current payment amounts. Unlike traditional student loans, which are usually repaid over 10 years, income-driven repayment plans are usually available for 20-to-25-year terms and may in some cases be forgiven at the end.

Both the number of borrowers and the volume of loans in income-driven plans grew significantly from 2010 to 2017. The percentage of borrowers using income-driven plans grew from 11% to 24% for those with undergraduate loans and from 6% to 39% for those with graduate loans. The Congressional Budget Office (CBO) estimates that in 2017 approximately 45% of direct loan balance repayments used an income-driven plan, up from about 12% in 2010.5

There are four income-driven plans:

- Revised Pay As You Earn Repayment Plan (REPAYE Plan);

- Pay As You Earn Repayment Plan (PAYE Plan);

- Income-Based Repayment Plan (IBR Plan); and

- Income-Contingent Repayment Plan (ICR Plan).

The borrower’s tax return filing status (married filing jointly (MFJ) or married filing separately (MFS)) affects the yearly loan payment amount under three of the plans (PAYE, IBR, and ICR). These three plans determine the yearly loan payment based on joint income if the couple file jointly and based on individual income if the spouses file separately. Depending on the couple’s income and loan balance, the yearly loan payment may be significantly lower when the payment amount is calculated using only the individual borrower’s income.

Many clients automatically assume that the benefit from reduced loan payments exceeds the additional tax cost of MFS. However, when questioned about the difference in payment associated with only using the individual borrower’s income, the clients eventually admit that they do not know the amount of the payment difference.

It is not clear how and for how long the COVID-19 pandemic will affect the employment market. However, it is clear that many families’ incomes have suffered as a result of the pandemic. This income reduction may lead additional student loan borrowers to consider changing their student loan repayment plan to one of the income-driven plans. Advisers should be ready to guide clients evaluating the potential benefits and costs of shifting to an income-driven repayment plan, including the possibility of further reductions in the student loan payment by filing separately.6

First, this article reviews the tax law differences between MFJ and MFS. Next, the three income-driven plans that calculate payments differently depending upon filing status are discussed. Using various taxpayer scenarios, this article compares the tax cost of MFS with the reduction in loan payments, using individual versus joint income under the three income-driven plans. Last, the article presents a few guidelines for tax advisers working with clients trying to minimize their student loan repayments through their tax filing status.

MFJ vs. MFS

A couple filing MFS returns generally incur a greater tax liability than if they file an MFJ return, because of the numerous differences in the tax law between the two filing statuses. The differences include tax rates, the opportunity to claim various exclusions and credits, and lower eligibility or phaseout levels.

The usual assumption that the higher marginal rate for couples filing separately results in a greater tax liability is true in most situations. However, couples with relatively equal incomes are not significantly affected by differences in marginal rates since the MFS marginal rate shifts occur at levels equal to one-half of the MFJ marginal rate amounts. (See the chart “2019 Marginal Tax Rates and Bracket Shift,” below.)

The tax liability of a couple filing MFJ with $100,000 of taxable income is $13,717. The tax liability of a married individual filing separately with $50,000 of taxable income each is $6,858.50, exactly one-half of the tax liability of the MFJ couple.

However, the tax liability of a married couple filing separately with $80,000 and $20,000 of taxable income is $13,458 and $2,206, respectively. The total tax liability of $15,664 is $1,947 greater than if the couple file MFJ. The additional tax liability results from the lower-income spouse’s not fully utilizing the 12% marginal rate and the higher-income spouse’s paying tax on a larger amount at the 22% marginal rate.

In addition to changing the way a married couple calculate their tax liability, choosing MFS affects the availability of certain credits, deductions, and exclusions. The MFS status prevents the taxpayer from taking the following credits:

- Credit for child and dependent care expenses;5

- Earned income tax credit;

- Adoption credit;6

- American opportunity credit and lifetime learning credit (education credits); and

- Credit for the elderly or disabled (if the taxpayers lived together at any time during the year).

Other limitations involving education-related provisions that affect taxpayers choosing MFS include:

- Neither can take the deduction for student loan interest or the tuition and fees deduction; and

- Neither can exclude interest income from qualified U.S. savings bonds used for higher education expenses.

Other deductions, exclusions, and credits affected by reduced income levels that apply to MFS taxpayers include:

- The income exclusion amount under an employer’s dependent care assistance program is limited to $2,500 ($5,000 on a joint return);

- The phaseout levels for the child tax credit, credit for other dependents, and retirement savings contributions credit are one-half of those for a joint return;

- The capital loss deduction limit is $1,500 ($3,000 on a joint return); and

- Both spouses must either take the standard deduction (one-half of the joint amount), or both spouses must itemize.

The prohibition on deducting student loan interest expense when choosing to file separately affects taxpayers with student loans and modified adjusted gross income under $170,000.7 Higher-taxable-income taxpayers approaching the student loan phaseout range are in the 22% marginal rate. For these taxpayers, losing the $2,500 student loan interest deduction increases their tax liability by $550.

After a couple have a child, the loss of the child care credit will increase the tax cost of MFS. The child care credit is $600 for one child ($3,000 of expenses at a 20% rate) and $1,200 for two or more children ($6,000 of expenses at a 20% rate) for couples MFJ with income in excess of $43,000.

Income-driven repayment plans

Developed as an option to make student loan repayment more manageable, income-driven plans reduce monthly payments for borrowers with low incomes or large balances. Of the four income-driven plans available, three consider filing status (PAYE, IBR, and ICR plans). The plans differ regarding student loan type, the timing of the borrowing, the required payment calculation, and when the remaining loan balance is forgiven. The fourth income-driven plan, REPAYE, uses total family income regardless of tax filing status. This exhibit includes detailed information regarding the types of federal student loans eligible for each income-driven repayment plan.

PAYE Plan

The PAYE Plan is available for Direct Loans8 only (including most direct consolidation loans), and borrowers must have received a disbursement of a Direct Loan on or after Oct. 1, 2011. Payments under the plan are limited to 10% of the borrowers’ discretionary income. The plan caps the payment amount so it cannot be more than under a 10-year standard repayment plan. Remaining loan balances are forgiven after 20 years of repayment.

Discretionary income is defined as household income above 150% of the federal poverty level based on the borrower’s family size and state of residence. Household income is generally defined as the borrower’s adjusted gross income (AGI) on his or her most recent tax return. If a married borrower files a joint tax return, then household income is the couple’s joint AGI.

IBR Plan

The IBR Plan is available for Direct Loans and most Federal Family Education Loans (FFEL loans). The FFEL loans that are not eligible for the plan are parent PLUS Loans and Consolidation loans that include at least one parent PLUS Loan.

The original IBR Plan became available in July 2009. The Health Care and Education Reconciliation Act of 20109 revised the plan for new borrowers on or after July 1, 2014. The original IBR Plan limits payments to 15% of the borrower’s discretionary income, capped at the payment amount determined under a 10-year standard repayment plan with remaining loan balances forgiven after 25 years of repayment. The revised IBR Plan limits payments to 10% of the borrower’s discretionary income with the same cap, with remaining loan balances forgiven after 20 years of repayment.

Discretionary income is defined as household income above 150% of the federal poverty level based on the borrower’s family size, the same calculation as for the PAYE Plan. Household income for a married borrower is the borrower’s AGI, if MFS, and the joint AGI of the borrower and his or her spouse, if filing MFJ.

ICR Plan

The ICR Plan is available for Direct Loans, including Direct Consolidation Loans. The ICR Plan allows the Direct Consolidation Loans to include parent PLUS loans and FFEL loans. This is the only income-driven plan available to parent PLUS Loan borrowers (after loan consolidation). The plan forgives remaining loan balances after 25 years.

Payments under the plan are equal to 20% of the borrower’s discretionary income, subject to a cap. The cap equals the amount the borrower would pay under a standard repayment plan with a 12-year repayment period, adjusted using a formula that takes the borrower’s income into account. Discretionary income is defined as household income above the federal poverty level based on the borrower’s family size and state of residence. Household income for a married borrower is the borrower’s AGI, if MFS, and the joint AGI of the borrower and his or her spouse, if MFJ.

REPAYE Plan

The REPAYE Plan is available for Direct Loans including most Direct Consolidation Loans. Payments are limited to 10% of the borrower’s discretionary income. Unlike the other income-driven plans, the payment is not capped. Remaining loan balances are forgiven after 20 years for undergraduate borrowers and 25 years for graduate borrowers.

Discretionary income is defined as household income above 150% of the federal poverty level based on the borrower’s family size and state of residence. For this plan, household income for a married borrower includes the joint AGI of the borrower and his or her spouse, regardless of their tax filing status.

Tax cost compared to loan repayment savings

To gain a better understanding of the impact of MFS on the income-driven plan repayment amount compared with the tax cost of MFJ, this article calculated the tax cost of MFS and the difference in loan payments for MFJ and MFS for various fact patterns. The tax difference is based on 2019 tax rate schedules. The loan repayment difference uses repayment calculations from the Loan Simulator provided on the Federal Student Aid website.10 The calculation used a 5% interest rate for the loans and a 2% increase in yearly earnings (the website’s default percentage increase).

A recent CBO study reports that undergraduate borrowers in income-driven and fixed payment plans had received, on average, $25,100 and $18,500, respectively, of loan disbursements.11 For a dependent undergraduate student, the current aggregate limit for federal loans is $31,000.12 Graduate students currently enrolled in income-driven plans received an average of $92,000 in loans.13 Based on these statistics, the loan payments and tax cost for the following married couples with no children are evaluated:

- Both spouses with student loans, $25,000 each, total student loans $50,000, student loan interest $2,500.

- One spouse with student loans, $90,000 total, student loan interest $4,500 (tax deduction limited to $2,500 for MFJ).

The examples used joint annual income levels ranging from $60,000 to $140,000 with varying combinations of income levels between spouses. These income ranges were chosen for a number of reasons. First, the student loan interest deduction of up to $2,500 for a married couple filing jointly begins to phase out at AGI levels over $140,000. For married couples filing jointly with children, the child and dependent care credit percentage becomes constant at 20% for married couples with AGI of $43,000 or higher. Also, for married couples filing jointly, the earned income tax credit for a couple with two children completely phases out at $52,500.

Married, no children, both spouses have student loans

Table 1 summarizes the results for taxpayers with no children when each spouse has individual loan amounts of $25,000. The results show that, as a broad generalization, as total income increases, the net benefit of the income-driven plans decreases, and eventually the tax cost of MFS exceeds the loan repayment savings.

The tax difference between MFJ and MFS with no children is attributable to the deduction for student loan interest on the MFJ return, which is not allowed when MFS, and the difference in marginal tax rates when the income levels of the two spouses differ. The difference in the loan repayment amount is attributable to the loan balances, the difference in individual income levels, and the loan program.

When both spouses have loans, the tax cost is lowest when the spouses’ incomes are relatively equal. With relatively equal incomes, the only tax cost of MFS is the tax savings associated with the student loan interest deduction that is allowed when MFJ. As the difference between the spouses’ incomes grows, the tax cost of MFS increases due to the increased marginal tax rate of the spouse with the higher income.

As the income of one spouse increases, the MFS loan payment for that spouse increases while the MFS loan payment for the spouse with the lower income decreases. The respective payment increase and decrease are not the same. Depending on the loan amount, at some income levels the PAYE and IBR payments are capped at the Standard Payment amount. At $20,000 of income, the MFS payment amount under the PAYE and IBR plans is $0.

In general, for couples with less than $100,000 of total income, the payment savings from using individual incomes instead of joint income in the PAYE, IBR, and ICR income-driven plans exceeds the tax cost of MFS.

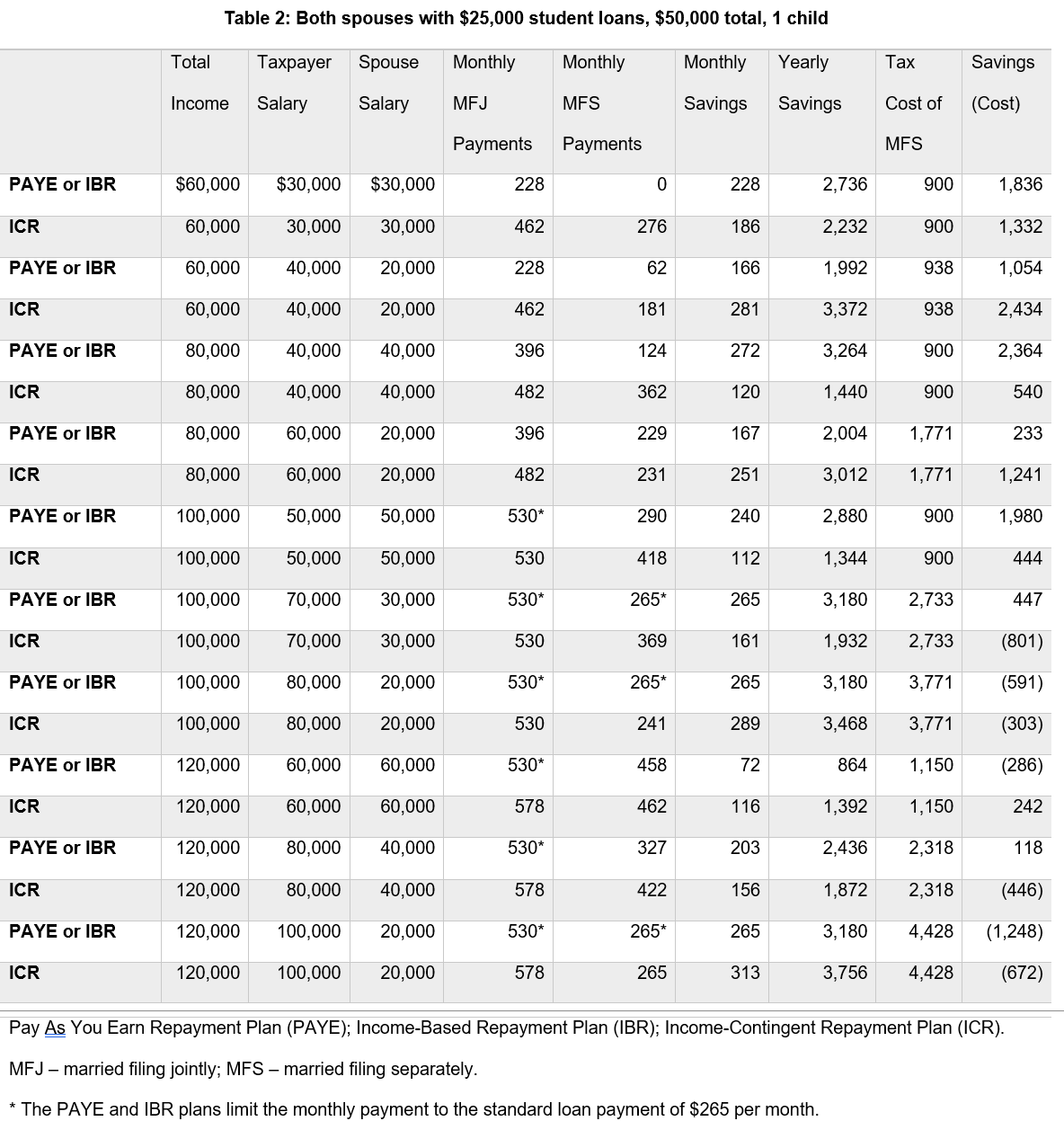

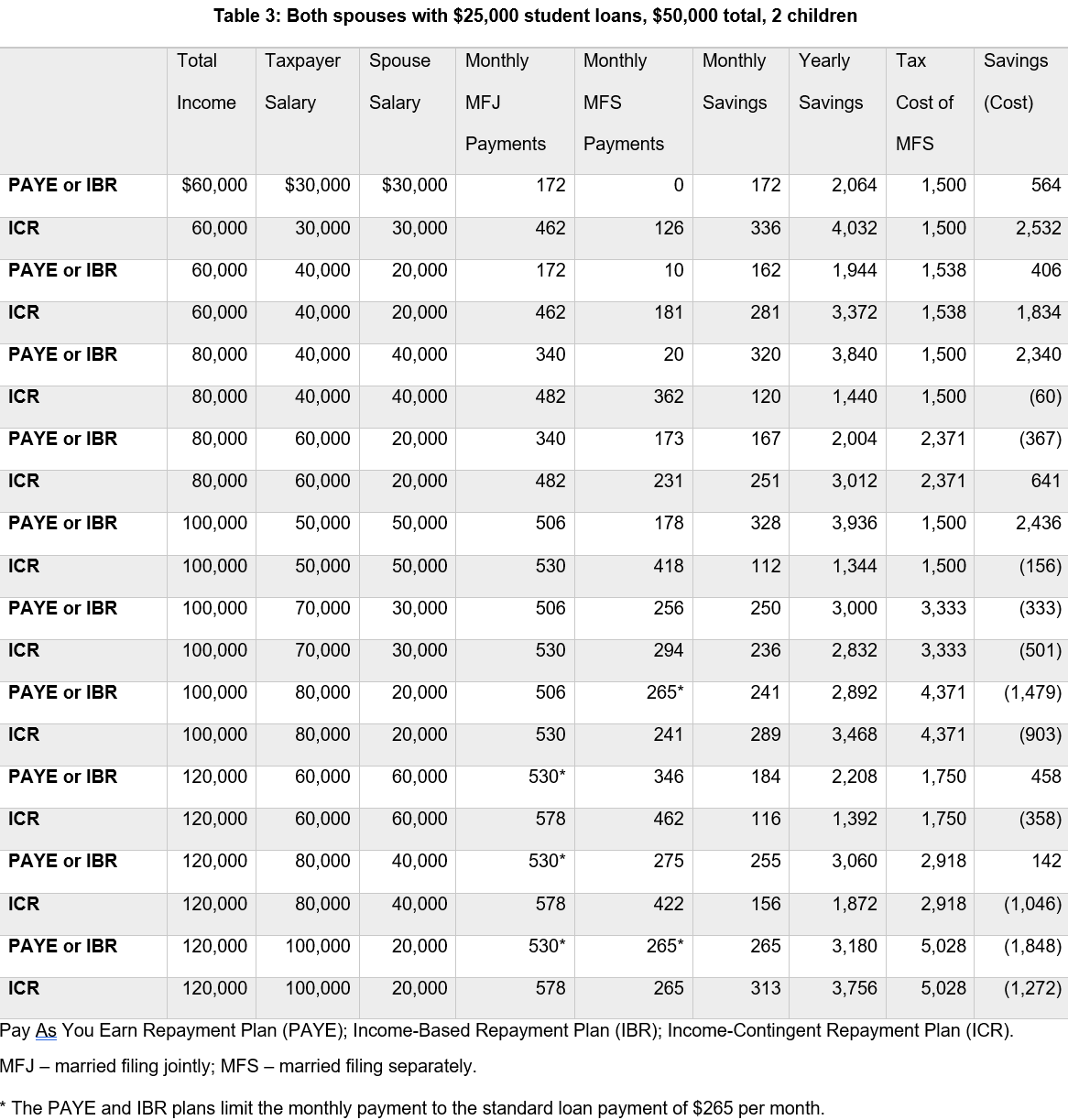

Married, with children, both spouses have student loans

Tables 2 and 3 show the impact of adding one child or two children, respectively, to the family. The tax calculations assume a $2,000 child tax credit (per child) and a child care credit of $600 (one child) or $1,200 (two children). When calculating the MFS tax liability, the child tax credit reduces the tax liability of the taxpayer with the larger income. The MFJ tax computations assume the taxpayers incur child care costs that result in a $600 or $1,200 child care credit for one child or two children, respectively. The child care credit is not allowed if the couple file separately. Losing the child care credit increases the tax cost of MFS by $600 and $1,200 for taxpayers with one child or two children, respectively.

The increase in family size reduces the loan repayment amount in most cases. The median reduction under the PAYE or IBR plans is $56 per month for one child (range from $0 to $112 per month). Family size has less impact on the ICR payment amount with a median reduction of $0 (range from $0 to $46 per month). Increasing the family size to four (from three) reduces the PAYE or IBR payment by a median of $56 per month (an additional $56 above the reduction, if any, for one child). The range is from $0 to $112 per month. The ICR payment is only reduced in four instances out of 14 (three reductions of $75 and one reduction of $150 per month).

Although the monthly savings from reduced loan payments when filing MFS increased in the majority of cases, the net savings after the tax cost decreased in the majority of cases. This result is due to the increase in the tax cost from the loss of the child care credit. With one child, the benefit of MFS remains constant through the $80,000 income level, but it is not certain at the $100,000 level and above. With two children, the loss of the $1,200 child care credit results in the net benefit from MFS remaining at the $60,000 income level but is not certain at the $80,000 income level and above.

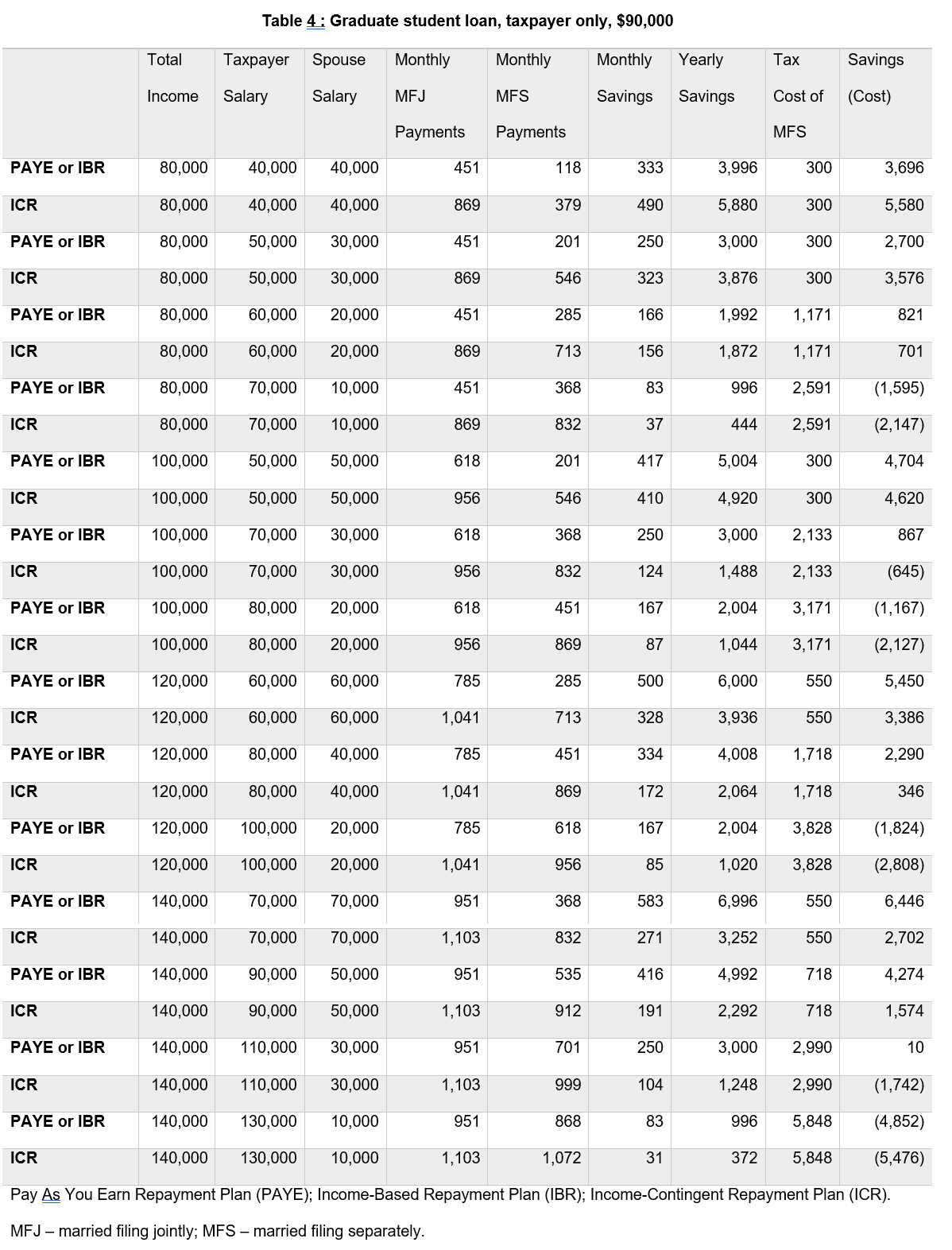

Married, no children, one spouse with student loans

Table 4 shows the net savings or cost when one spouse has $90,000 of student debt, the average debt level for a graduate student. The total income level begins at $80,000 because at income levels below $80,000, there is a net benefit of MFS regardless of the percentage of income earned by the spouse with the student loan (assuming that the spouse without the loan earns at least $10,000). As the income of the spouse with the loans represents a larger percentage of the joint income, the net benefit of MFS decreases and ultimately results in a net cost.

The net benefit decreases as the income of the spouse with the loan increases because (1) the loan payment savings decline and (2) the tax cost of MFS increases. The tax cost increases as the spouses’ income levels become more disparate. As the difference in the two incomes increases, the couple lose the benefit of the 12% tax bracket on a portion of their taxable income. This adds to the tax cost of losing the student loan interest deduction.

Tax planning for income-driven repayment plans

As the number of college graduates with large amounts of student loan debt increases, clients will expect their tax advisers to determine whether the reduction in loan repayment amounts under income-driven repayment plans is worth the tax cost of MFS. The following approach outlines the steps an adviser should consider in advising clients.

Estimate the student loan payment

Using a student loan repayment calculator, determine the required payments when filing jointly versus separately. The Federal Student Aid Loan Simulator is located at studentaid.gov/loan-simulator. This is the loan simulator used for the examples in this article, and it easily allows a change in the facts from MFJ to MFS.

Compare the tax liability

Most tax preparation packages provide an option comparing the tax liability for a married couple filing jointly versus filing separately.

Consider long-term consequences

This article focuses on a couple who chose an income-driven repayment plan and want to keep their student loan payments as low as possible. In addition to determining whether there is a net benefit from MFS, the tax adviser should remind the couple of the long-term consequences of choosing an income-driven repayment plan. Compared to the 10-year standard repayment plan, individuals will pay more interest under the 20- or 25-year income-driven repayment plans. The yearly earnings and loan balances of borrowers determine whether they will repay their loans in full. If the borrower has a remaining balance at the 20- or 25-year forgiveness point, the loan forgiveness is taxable under current law.

Tax planning to lower AGI

The income-driven plans determine the loan payment based on AGI. Lowering the AGI of the spouse with student loans or lowering the income of the higher-earning spouse if both spouses have loans can reduce the required student loan payment. Tax planning options for reducing AGI include contributing to a 401(k) plan, a traditional IRA, or a health savings account. Couples should also take advantage of pretax fringe benefits, including pretax health insurance benefits and transportation benefits.

Couples with children should consider using their employer’s dependent care flexible spending program (limited to $2,500 for those couples filing separately). The amount contributed to the dependent care flexible spending program reduces taxable wages and lowers AGI. When a couple file jointly, the dependent care flexible spending contribution reduces the child care expenses eligible for the child care credit. If the couple’s marginal tax rate is less than 20% (the child care credit percentage), then the couple are better off taking the credit. However, when an individual files MFS, the child care credit is not allowed, so the dependent care flexible spending contribution reduces AGI and provides a tax benefit at the individual’s marginal tax rate.

While identifying options to reduce AGI is a good idea for most taxpayers, it provides a double benefit to those with income-driven student loan repayment plans. Taking advantage of tax planning opportunities to reduce AGI lowers the couple’s tax liability whether they file MFJ or MFS. The lower AGI may also reduce their student loan payment under an income-driven repayment plan based on either joint or individual incomes.

Given the significant increase in student loans, tax advisers should have a basic understanding of the student loan repayment options available and the impact of tax filing status on loan payment amounts. For a young couple with debt levels used in our examples (starting at $30,000 in total debt), the loan payment savings under an income-driven repayment plan can exceed the MFS tax cost for combined salaries of up to approximately $100,000. Tax planning that reduces the AGI of the individual with the higher debt level increases the overall savings when the individual is using an income-driven repayment plan.

As the average student loan balance continues to rise, borrowers face larger monthly payments as they begin careers after graduation. In search of smaller monthly payments, many borrowers turn to income-driven repayment plans. Tax advisers can serve an important role in educating taxpayers about the impact of their tax filing status on their loan repayment calculation. By identifying tax planning strategies, tax advisers can help clients develop plans for paying off their student loans, taking into account their tax liability.

Footnotes

1Congressional Budget Office,Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (February 2020), available at www.cbo.gov. For more on student loan debt, see Kelley and Eiler, “Student Loan Debt: Tax and Other Considerations,” 51 The Tax Adviser 800 (December 2020).

2Center for Microeconomic Data, “Quarterly Report on Household Debt and Credit,” available at www.newyorkfed.org.

3Congressional Budget Office,Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (February 2020).

4The Coronavirus Aid, Relief, and Economic Security (CARES) Act, P.L. 116-136, suspended student loan payments, stopped collections on defaulted loans, and set interest rates to 0% through Sept. 30, 2020. On Aug. 8, 2020, President Donald Trump directed the Department of Education to continue these measures through Dec. 31, 2020.

5Taxpayers who are legally separated or living apart from their spouse may still be able to take the credit when filing separately.

6Taxpayers who are legally separated or living apart from their spouse may still be able to take the credit when filing separately.

7The student loan interest deduction phases out for married couples filing jointly with modified adjusted gross income between $140,000 and $170,000 in 2019 (Rev. Proc. 2019-44).

8Direct Loans are made under the U.S. Department of Education’s William D. Ford Federal Direct Loan Program. See U.S. Department of Education, “William D. Ford Federal Direct Loan Program,” available at studentaid.gov.

9Health Care and Education Reconciliation Act of 2010, P.L. 111-152.

10U.S. Department of Education, Loan Simulator, available at studentaid.gov/loan-simulator.

11Congressional Budget Office,Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (February 2020).

12U.S. Department of Education, “The U.S. Department of Education Offers Low-Interest Loans to Eligible Students to Help Cover the Cost of College or Career School,” available at studentaid.gov.

13Congressional Budget Office,Income-Driven Repayment Plans for Student Loans: Budgetary Costs and Policy Options (February 2020).

Contributors | |

| Nancy B. Nichols, Ph.D., M.S. (Taxation), is the Journal of Accounting Education professor, and Irana J. Scott, Ph.D., is an associate professor, both at James Madison University in Harrisonburg, Va. For more information about this article, contact thetaxadviser@aicpa.org.

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}