- feature

- INDIVIDUALS

Current developments in taxation of individuals

Related

IRS updates overtime deduction FAQs, adds reporting details

Planning for new charitable contribution limits

The end of deferral: Calculating QOZ gain recognition on Dec. 31, 2026

TOPICS

This semiannual update surveys recent federal tax developments involving individuals. It summarizes notable cases, rulings, and guidance on a variety of topics issued during the six months ending October 2023. The update was written by members of the AICPA Individual and Self-Employed Tax Technical Resource Panel. The items are arranged in Code section order.

Sec. 24: Child tax credit; Sec. 32: Earned income

Credits denied for lack of Social Security numbers: In Sowards,1 the taxpayer was unable to convince the Tax Court that child tax credits (CTCs), additional child tax credits (ACTCs), and earned income tax credits (EITCs) should be allowed when the taxpayer’s spouse and four children did not have Social Security numbers (SSNs) reported on his and his spouse’s jointly filed tax returns. The spouse did not have an SSN because she was not a citizen. In accordance with his religious beliefs, which included conscientious objection to reliance on public insurance and government benefits, the taxpayer had not obtained SSNs for the children and had intended to let them obtain an SSN at an appropriate age if they desired. To obtain individual taxpayer identification numbers (ITINs) for the children for income tax purposes, the taxpayer mailed requests for ITINs for them along with his 2010 tax return, but the IRS did not respond to these requests.

The taxpayer claimed the EITC and ACTC for the couple’s children for 2008 and 2009, and the CTC for the children for 2010. The IRS disallowed the credits and made assessments for each year. The taxpayer, in response to collection activity, in 2017 submitted amended returns for the years in question that listed the children’s newly obtained SSNs.

Because by the time the taxpayer filed the amended returns, Sec. 24(e)(1) had been amended to require taxpayers claiming a CTC or ACTC to include a taxpayer identification number of any qualifying child that is issued on or before the due date for filing the return, the Tax Court held that the SSNs provided on the amended returns did not comply with Sec. 24(e)(1) requirements at the time they were submitted. Therefore, the ACTCs for 2008 and 2009 and the CTC for 2011 were disallowed. The Tax Court denied the taxpayer’s arguments that equitable estoppel applied to bar the IRS from applying the amendment to the tax years at issue. The court also denied the taxpayer’s arguments based on due process rights and conscientious objection to participation in the Social Security system.

For the couple to have claimed the EITC, an SSN for the taxpayer’s spouse was required under Sec. 32 to be included on their joint return. The spouse was not eligible to obtain one when the original and amended returns for 2008 and 2009 were filed, so the Tax Court did not allow the EITCs claimed for those years.

Sec. 59(e): Optional 10-year write-off of certain tax preferences

In Letter Ruling 202320001 the IRS was asked to rule on a taxpayer’s request for a 120-day extension to elect under Sec. 59(e) to deduct research and experimental (R&E) expenditures ratably over a 10-year period. The facts disclosed that the taxpayer had intended to make an election under Sec. 59(e) but did not attach the required election statement to its income tax return, on which it capitalized and amortized its R&E expenditures under Sec. 59(e). The IRS ruled favorably and granted a 120-day extension to make the election, noting that the taxpayer acted reasonably and in good faith and that granting relief would not prejudice the government’s interests.

Sec. 61: Gross income defined

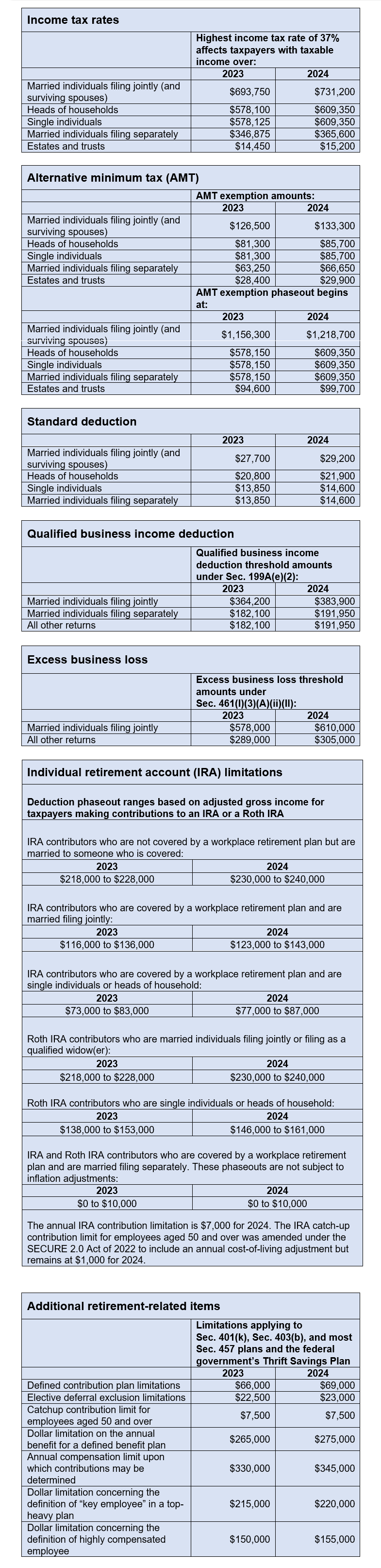

The IRS released Rev. Proc. 2023-34 and Notice 2023-75 to announce the annual inflation adjustments for the 2024 tax year, including various income tax provisions and the income tax rate schedules, along with the adjustments to pension plan limitations and other retirement-related items. A summary of some of these updates is available here.

Sec. 72: Annuities; certain proceeds of endowment and life insurance contracts

Income from IRAs: The Tax Court held that a taxpayer did not have an income inclusion from money his wife withdrew from his IRA beyond the scope of her authority under a power of attorney. In 2014, the taxpayer, Joseph Balint, was incarcerated. He gave his wife a power of attorney with broad powers. She withdrew $89,877 from his retirement account and $47,593 from his life insurance policy. She then moved to another state and used the funds to renovate a residence, care for her mother, and pay living expenses. She also started divorce proceedings. Balint was served divorce papers in October 2014 while he was still incarcerated. When he was released in early 2015, he reported all the income from the distributions even though he thought it was incorrect. He requested a Collection Due Process hearing and checked a box for innocentspouse relief. The Tax Court held that he received no economic benefit from the withdrawals, except for a portion from his IRA that he conceded had been deposited to a joint checking account, and that he was not taxable on the remainder.2 No innocent-spouse relief was granted because he had filed a separate return.

Income from lapsed life insurance loans: The Tax Court held that another incarcerated taxpayer constructively received distributions from the termination of his life insurance policies for which the insurer applied the policies’ cash value to repay loans.3 The taxpayer, Robert Doggart, was incarcerated in 2017. Previously, he had taken out loans against his Prudential life insurance policies. He stopped paying premiums while incarcerated, and Prudential offset the policy cash values against the loans. He received 2017 Forms 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., from Prudential for each policy, and Prudential explained why the forms were sent when he inquired about them.

Doggart filed no 2017 tax return; the IRS prepared a substitute for return in 2020 and assessed tax for 2017. In 2021, Doggart prepared his own 2017 return showing a loss of $77,675 in connection with a property he rented to his daughter at less than fair market value (FMV).

Doggart argued that he was not taxable on the distributions from the life insurance policies because he did not actually receive any money at the time the policies were terminated. The Tax Court disagreed, noting that although he did not physically receive money upon the lapse of his policies, he no longer had to repay his policy loans, so the distributions were income to Doggart even though no money changed hands.

The Tax Court did not allow the claimed loss in connection with the property, holding that he had used the property as a residence in 2017. In determining the number of days he used the property as a residence, the court counted the days he actually stayed at the property in 2017 and the days he rented it to his daughter at less than FMV during the year.

The Tax Court also held that Doggart’s being incarcerated was not reasonable cause for failing to file his return for 2017, and he was liable for a penalty for failure to file, regardless of the fact that he wrongly believed that he was not required to file while incarcerated.

Sec. 162: Trade or business expenses

The taxpayers in Sinopoli44 deducted rental expenses paid by an S corporation, Planet LA LLC, which they collectively owned. In tax years 2015– 2017, the S corporation deducted rent expense that had been paid to the taxpayers for use of their personal homes for business meetings. In addition, the petitioners reported the rental income on Schedule E, Supplemental Income and Loss, of their personal returns and relied on Sec. 280A(g) to exclude the rent from gross income under its exclusion rule for 14 or fewer days of rental of a taxpayer’s residence during a tax year.

On audit, the IRS questioned the reasonableness of the rent, which ranged between $3,000 to $4,000 per meeting and was paid to related parties. It allowed as deductible business expenses only rent for meetings that the taxpayers substantiated with meeting notes as taking place and limited the amount of rent for each meeting to $500, which the IRS had determined was a reasonable rental rate for local meeting space. The Tax Court held that the taxpayers had failed to prove through credible testimony or documentation that the rental expenses they claimed were reasonable, and it upheld the IRS’s limitation on their rental expense deduction. This case is a reminder that a deductible business expense must be reasonable and that related-party transactions will face additional scrutiny.

Kraske 5 illustrates the requirement of an activity to be a trade or business conducted with continuity and regularity and with the primary purpose of realizing income or profit in order for its ordinary and necessary business expenses to be deductible. The taxpayer, Wolfgang Kraske, included in his returns for 2011 and 2012 a Schedule C, Profit or Loss From Business (Sole Proprietorship), on which he deducted expenses of a purported business, referred to as Ovium, of developing new and highly innovative models of “self-organizing nanocomponents,” “a quantum computer,” and “communities of nanorobots.”

The Tax Court analyzed whether Ovium’s expenses were deductible under Sec. 162 as a trade or business or were limited to income from an activity not engaged in for profit, under the test of Regs. Sec. 1.183-2. The factors considered included the existence of a profit motive, whether operations were conducted in a businesslike manner, expertise of the taxpayer/advisers, time or effort expended by the taxpayer, expectation of business assets’ appreciation, success in similar or dissimilar activities, history of income or losses in the activity, amount of occasional profits, the taxpayer’s financial status, and elements of pleasure or recreation.

The court determined that Kraske did not demonstrate a good-faith expectation of profit, as the sustained losses year over year were not met with efforts to recoup them or improve profitability. Any expectation that assets used in the activity would appreciate was also lacking. Additionally, Kraske did not run Ovium in a businesslike manner due to a lack of a detailed business plan or budget, lack of a separate business bank account, vague payment terms in a consulting contract, an absence of bookkeeping, and incomplete records. Finally, the recreational and personal-motive elements in Ovium were evident to the court from the substantial receipts expensed for personal entertainment (movies, restaurants, hockey games, and a trip to Japan).

Sec. 165: Losses

Taxpayer Marc Johnson had been friends with John Harrison since they were teenagers. Johnson wanted to invest in real estate, in which Harrison had a reputation as a successful professional. They invested together in one property, and Johnson decided to invest more. He did this through two negotiated unsecured promissory notes in the amounts of $340,000 and $500,000. When Harrison was indicted on a charge of bank fraud, Johnson and his spouse reported on their joint return for 2012 the $840,000 in loans as short-term capital loss bad debts. Upon consulting tax advisers, they amended the 2012 and 2015 returns to treat the losses as theft losses.

When the IRS denied the refund claims, the taxpayers sued for a refund in district court, where they filed a motion for summary judgment on the grounds that the losses qualified under Sec. 165 as theft losses and that there was no dispute of material fact. The IRS filed a cross-motion stating, among other things, that the Johnsons were not defrauded.

To claim a theft loss deduction, a taxpayer must prove the existence of a theft, the amount of the deductible loss, and the year in which the loss was discovered.6 The existence of a theft loss must be shown under the law of the jurisdiction in which the alleged theft occurred, which in this case was South Carolina. This required that the funds were taken under false pretenses. The district court agreed with the government that the Johnsons did not prove that Harrison made fraudulent statements to induce them to make the loans. It also rejected the taxpayers’ contention that false pretenses were proved by Harrison’s pleading guilty to bank fraud. Accordingly, the district court held the Johnsons did not prove that false pretenses were involved and denied the claimed theft losses.7

Sec. 170: Charitable, etc., contributions and gifts

Courts in several cases were asked to determine whether taxpayers claiming charitable contribution deductions met the substantiation requirements of Sec.170. Taxpayers claiming deductions must adhere to statutory and regulatory substantiation requirements, which depend on the size of the contribution and whether the donation is of cash or property. They must also maintain adequate records to support items underlying the claimed deductions.

Substantiation requirement for certain contributions: In Braen,8 the taxpayers were family members and shareholders in an S corporation that undertook a “bargain sale” to a municipality of undeveloped real estate in connection with the settlement of zoning litigation. The S corporation asserted that the bargain sale was made with donative intent and thus claimed a charitable contribution deduction on its 2010 tax return for the difference between the FMV of the property sold and the purchase price. The IRS disallowed the charitable contribution claimed by the S corporation on the basis that it failed to show the value of all consideration received as part of the land sale and thus fell short of establishing the value of the charitable contribution. In turn, the proportionate charitable contribution deductions claimed by the shareholders on their individual income tax returns were disallowed. In addition, the IRS argued that the S corporation failed to satisfy the contemporaneous written agreement requirements of Sec. 170(f)(8).

The two principal requirements to claim a charitable contribution deduction in connection with a bargain sale are: (1) The FMV of the property donated must exceed the value of any benefits received, and (2) the taxpayer must supply a contemporaneous written acknowledgment from the recipient substantiating the contribution. Regarding the first requirement, the Tax Court considered the land sale agreement and the settlement of zoning litigation as an inseparable integrated transaction and determined that the zoning settlement was a benefit that was required to be valued in addition to the cash received for the land. However, the S corporation did not include the value of the zoning settlement for deduction purposes and thus failed to establish the value of the contribution.

Regarding the second requirement, the IRS argued that the S corporation failed to satisfy the requirement that a written acknowledgment must include a description and good-faith estimate of the value of any goods or services it received as consideration. The S corporation obtained a zoning change as part of the settlement and land purchase, and the written acknowledgment was required both to identify it as consideration and to provide a good-faith valuation of it. While the S corporation did receive a written acknowledgment letter from the town, the letter did not identify the zoning settlement as consideration and instead stated that the town did not provide “any goods or services … as consideration” other than cash. In the end, because the S corporation failed to meet the requirements to claim a charitable contribution deduction in connection with a bargain sale, none of the individual shareholders were entitled to a deduction.

In another case decided during this period,9 the taxpayer claimed a charitable contribution deduction of $25,000 for cash gifts to a church in connection with a benefit fashion show. The IRS disallowed the deduction (but later conceded that the taxpayer substantiated $13,050 of the amount) because the written acknowledgment did not indicate whether the church provided any goods or services in consideration for the donations. The Tax Court agreed, and the taxpayer’s deduction was limited to the amount that was properly substantiated.

Qualified appraisal and other documentation for certain contributions: Across three cases involving members of the same family, the Tax Court ruled on required documentation matters related to donations of conservation easements, denying efforts by the IRS to disallow the claims in full but upholding valuation penalties in two of the cases.

In Murfam,10 the taxpayer, Murfam Enterprises LLC, donated a perpetual conservation easement to a qualified organization for conservation purposes. The tract of land subject to the easement had been granted hog-farming certificates by the state. On its 2010 tax return, the taxpayer claimed a charitable contribution deduction, supported by an appraisal of the donated property. The appraisal valued the easement deduction based on the forgone value of the hog-farming certificates attached to the property. The tax return included an incomplete Form 8283, Noncash Charitable Contributions, that did not include the taxpayer’s basis in the land.

Upon examination, the IRS reduced the deduction on the premise that the value of the hog-farming certificates was zero and the easement should have been valued according to the land’s use as timberland. The taxpayer filed a petition in Tax Court asking the court to review the IRS’s determination. In its response to the taxpayer’s petition, the IRS made a new assertion that the deduction should be entirely disallowed because the taxpayer did not comply with the substantiation and reporting requirements when it failed to attach a fully completed appraisal summary to Form 8283. The taxpayer claimed reasonable cause on this aspect, citing reliance on its CPA.

In general, a taxpayer bears the burden of proof; however, since this was “new matter” in the case, the IRS had the burden of proving that the taxpayer did not have reasonable cause or demonstrated willful neglect with regard to the defective Form 8283. The court held that while Murfam did in fact fail to strictly or substantially comply with the reporting requirements of Sec. 170(f)(11), the IRS did not meet its burden of proof to show a lack of reasonable cause. Thus, the charitable contribution deduction was not entirely disallowed. The parties still disagreed as to the value of the easement and the amount associated with the deduction. The court considered the value of the forgone hog-farming certificates and redetermined the easement’s value as only slightly lower than what the taxpayer had originally claimed.

Murphy11 is a consolidated case involving two related married couples (belonging to the same family as in Murfam, above), who were shareholders in another S corporation that donated conservation easements on real estate that included recreational facilities and residential communities. The IRS examined the S corporation’s tax return and disallowed the deductions taken on the taxpayers’ individual tax returns. The Murphys challenged the IRS determination in Tax Court. As in Murfam, in its amended answer to the taxpayers’ petition, the IRS presented a new assertion: that the charitable contribution deductions should be disallowed entirely on the basis of defective Forms 8283, which did not include fully completed appraisal summaries.

The taxpayers claimed the failure to comply with reporting requirements was due to reasonable cause because they relied on their CPA. Once again, since this was “new matter” in the case, the IRS had the burden of proof. On this aspect, the Tax Court held in favor of the taxpayers, finding that the IRS did not meet its burden of proof to disprove reasonable cause. Unfortunately for the taxpayers, the court also held that the value of the easement donations was substantially lower than the taxpayers had reported, thus resulting in significantly reduced deductions and the upholding of accuracy-related gross valuation misstatement penalties.

Valuation of conservation easement at the time of donation: Sec. 170(h) allows a charitable contribution for the FMV of a qualified conservation contribution, which is defined as “a contribution (A) of a qualified real property interest, (B) to a qualified organization, (C) exclusively for conservation purposes.” 12 The Code and accompanying Treasury regulations provide the requirements that must be met before a contribution is deductible.

In 2012, Hawks Bluff Investment Group Inc. (Hawks Bluff) transferred undeveloped real estate that was part of an unsuccessful residential development to Glade Creek Partners LLC (Glade Creek) in exchange for a membership interest in Glade Creek. That same year, Glade Creek contributed a conservation easement on the undeveloped real estate and claimed a charitable contribution deduction. The Tax Court held that Glade Creek improperly took a charitable contribution deduction for the easement donation because the easement deed did not comply with the judicial extinguishment proceeds regulation and therefore did not satisfy the protectedin- perpetuity requirement under Sec.170(h).13

Glade Creek appealed to the Eleventh Circuit. After Glade Creek filed its appeal, the Eleventh Circuit issued its decision in Hewitt,14 which invalidated the proceeds regulation. Accordingly, in Glade Creek Partners, LLC,15 the Eleventh Circuit vacated the Tax Court decision and remanded the case for reconsideration without reliance on the regulation. On remand, the Tax Court was tasked with evaluating the IRS’s alternative arguments for disallowing the easement deduction. The IRS conceded that Glade Creek was entitled to an easement deduction, leaving the amount of the deduction as the sole issue to be decided.

Glade Creek claimed that the amount of the deduction was equal to the FMV of the easement. The IRS asserted that the deduction was limited to Glade Creek’s adjusted basis in the property because the donated property was inventory, not investment property, in the hands of Hawks Bluff, the partner that had contributed the property to Glade Creek. Of significance was the fact that Hawks Bluff had reported the easement property as inventory on its 2012 tax return and did not segregate it as investment property from its other inventory. The Tax Court placed great weight on Hawks Bluff ’s reporting and treatment of the easement property as inventory and, in accordance with Sec. 724(b), determined that the property retained its character as ordinary-income property in the hands of Glade Creek.16

Sec. 170(e)(1)(A) provides that if donated property had been sold by the donor at its FMV and if such a sale would have generated ordinary income or short-term capital gain, the charitable contribution deduction is reduced by the amount of ordinary income or shortterm gain and is thus limited to the taxpayer’s adjusted basis in the property. Consequently, because the Tax Court held upon remand in Glade Creek that the donated easement property was inventory, Glade Creek’s deduction was limited to the adjusted basis pursuant to Secs. 724(b) and 170(e).

Conservation purposes, qualified appraisal, valuation of conservation easement: The case of Mill Road 36 Henry, LLC17 highlights the ongoing conflicts between the IRS and syndicators of conservation easements. Ultimately, the Tax Court held that the value of the easement in question was less than one-twentieth of what was claimed and upheld a 40% accuracy-related penalty for a gross valuation misstatement.

Mill Road Partners, an LLC, was organized by real estate professionals to buy and sell land. The entity acquired 117 acres of undeveloped suburban property for $10,700 per acre in December 2014. Forty acres were partitioned to create a new tract, which was then contributed to MR36, a TEFRA partnership.18 In September 2016, an investment fund acquired a 97% ownership interest in MR36 and subsequently donated a perpetual conservation easement on 33 acres of the tract to a qualified organization for conservation purposes under Sec. 170(h)(1)(C). With an appraisal in hand, MR36 claimed a charitable contribution deduction of $8,935,000, or about $270,800 per acre. Form 8283 reported MR36’s basis in the property as $416,563, which derived from the purchase by the original partners in Mill Road Partners. The IRS examined MR36’s tax return and challenged the syndicated conservation easement deal on a number of fronts.

The IRS first argued that MR36 lacked donative intent and was simply trying to manufacture tax deductions for investors. The Tax Court rejected this argument based on the fact that a perpetual conservation easement was donated, no matter what the intent of the donor. The IRS also challenged whether the easement satisfied one of the four potential qualifying conservation purposes. Satisfying any one of the tests suffices to establish a conservation purpose. The court looked to the easement deed, which specified two of the qualifying conservation purposes: first, the “protection of a relatively natural habitat of fish, wildlife, or plants, or similar ecosystem,”19 and second, the “preservation of open space” for the scenic enjoyment of the general public or pursuant to a clearly delineated governmental conservation policy.20 The IRS argued that the easement was not high-quality enough to meet the “relatively natural habitat” standard in the Code and that it did not preserve open space pursuant to a government policy. The court rejected these challenges and held that the easement satisfied the conservation purposes stated in the deed.

The IRS also took issue with the appraisal, asserting that the appraiser was not qualified and that individuals who also contributed to the appraisal failed to sign it. Regs. Sec. 1.170A-13(c) (5) (ii) provides that an appraiser is not qualified if “the donor had knowledge of facts that would cause a reasonable person to expect the appraiser falsely to overstate the value of the donated property.” The IRS claimed that MR36 knew of zoning issues that caused the valuation to exceed FMV, but the Service did not get far with this argument. The court concluded that appraisers are not disqualified merely because donors know of an overstatement or of facts causing a value overstatement. The court also held that the appraiser’s employees who worked on the appraisal were not required to sign the appraisal.

The IRS fared better in its challenge to the value of the easement donation. The court found fault with the appraiser’s assumptions regarding comparable sales and the highest and best use of the property as a prospective assisted-living facility with a capacity that the court found to be excessive in light of licensing and other obstacles. Initially, the court restated the easement’s value to $900,000, almost 10 times lower than the amount MR36 reported. But on top of this, the court held that the property was inventory in the hands of the contributing partners. Pursuant to Sec. 170(e)(1)(A), this meant that the deduction was limited to the adjusted basis of $416,563. As a result of the drastically reduced deduction, MR36 faced the 40% accuracy-related penalty for a gross valuation misstatement under Sec. 6662(h), which the court upheld.

(Editor’s note: Congress and the IRS have taken recent steps to curb abusive syndicated conservation easement schemes. Under a provision enacted in 2022, a qualified conservation contribution is disallowed if the amount is more than 2½ times the sum of each partner’s or shareholder’s relevant basis in the partnership or S corporation, with certain exceptions (Sec. 170(h)(7); see also REG-112916-23). And in December 2022, the IRS proposed regulations that would identify certain syndicated conservation easement transactions and substantially similar transactions as listed transactions (REG-106134-22)).

Charitable contributions of artwork: In News Release 2023-185, issued Oct. 5, 2023, the IRS advised higher-income taxpayers to be wary of schemes involving overstated deductions for contributions of artwork. The alert includes red flags and procedures for properly claiming an art donation. The unscrupulous arrangements involve promoters convincing the taxpayer to purchase art that is promised to be worth significantly more than the purchase price, hold the art for at least one year, then donate the art and claim a tax deduction for an exaggerated FMV. Red flags include the promoters lining up specific appraisers for participants’ use, with the resulting appraisals lacking required information, such as sufficient description of the art and not addressing value characteristics, such as rarity, age, quality, condition, stature of the artist, price paid, and the quantity purchased. The news release reminds taxpayers that the IRS has a team of professionally trained appraisers who assist and advise the Service and taxpayers on valuation questions related to personal property and works of art. In connection with these schemes, the IRS has multiple active abusive art donation promoter investigations underway.

Sec. 172: Net operating loss deduction

In Bryan,21 the Tax Court agreed with the IRS that a taxpayer who held interests in two movie production LLCs was not entitled to deduct certain carryover net operating losses (NOLs). For tax years 2010–2012, the taxpayer claimed deductions for NOL carryovers resulting from passthrough losses deducted on his 2007, 2008, and 2009 tax returns. The IRS disallowed the original losses, thereby disallowing the subsequent NOL deductions.

With respect to the first LLC, the taxpayer held an indirect interest through his partnership. He gave a $2.7 million promissory note to his partnership, which in turn gave a substantially similar promissory note to the movie production LLC. Neither note was secured or collateralized or included a repayment schedule. The movie production LLC then obtained a loan in connection with its filmmaking activity. Neither the taxpayer nor his partnership pledged any assets as collateral or security for the movie production LLC’s loan, nor was the taxpayer or his partnership a guarantor of the loan. The taxpayer claimed passthrough losses in 2007 stemming from the movie production LLC that passed through his partnership to him as an individual. The Tax Court held that neither the taxpayer nor his partnership acquired outside basis as a result of the promissory notes. In the absence of sufficient outside basis, the taxpayer was not allowed to deduct the original passthrough losses. Furthermore, the court concluded that the promissory notes given by the taxpayer and his partnership were not bona fide debt, and, as such, he failed to establish that he was at risk in the moviemaking business of the LLC.

With respect to the second LLC, the taxpayer executed a $1 million promissory note in 2009 in exchange for his interest in the entity. He reported a $1 million passthrough loss from the LLC for tax year 2008. Since he first became a member of the LLC in 2009, the court held that he was not entitled to deduct a passthrough loss from the LLC for a year before he became a member. The taxpayer also claimed a $1 million passthrough loss from the LLC in 2009, relying on the existence of outside basis due to the promissory note. However, the court again held that the taxpayer did not acquire outside basis as a result of the promissory note.

With these findings, the court upheld the IRS’s disallowance of the original passthrough losses, which in turn disqualified the carryover NOLs.

Sec. 183: Activities not engaged in for profit

In Gregory, the Tax Court had concluded in a 2021 decision that the taxpayers’ 2014 and 2015 hobby losses under Sec. 183(b)(2) were subject to the 2% floor on miscellaneous itemized deductions established by Sec. 67(a).22 The taxpayers appealed to the Eleventh Circuit, which denied their petition for review in May 2023, thus affirming the Tax Court’s decision.23

Carl and Leila Gregory chartered their yacht, Lady Leila, in 2014 and 2015. The chartering activity was a hobby and not conducted for profit. The hobby generated income and also incurred considerable expenses each year. The Gregorys deducted some of those expenses under Sec. 183(b)(2) and placed them “above the line” on their individual income tax return, thereby reducing their gross income. Upon examination, the IRS determined that the Sec. 183(b)(2) deductions were miscellaneous itemized deductions under Sec. 67, such that they belonged “below the line” and reduced adjusted gross income (AGI), not gross income.

In 2014 and 2015, the Gregorys’ total income reached into the tens of millions of dollars. At that time, the Code allowed miscellaneous itemized deductions to the extent that they exceeded 2% of AGI. Because the Gregorys’ miscellaneous itemized deductions did not rise above 2% of AGI, the Sec. 183(b)(2) deductions were disallowed. Sec. 183(b)(2) allowed the Gregorys a deduction for their expenses from the hobby activity, but Sec. 67 precluded them from taking that deduction because they did not meet the 2% threshold for miscellaneous itemized deductions.

In the Eleventh Circuit, the Gregorys contended that the Tax Court had erred in classifying their hobby losses as miscellaneous itemized deductions subject to below-the-line treatment and the 2% floor. The appellate court denied the petition for review, with two members of the three-judge panel holding that the plain text of the Code settles the matter and that Sec. 183(b)(2) expenses are below-the-line miscellaneous itemized deductions. The third judge, in a concurring opinion, reasoned that the relevant Code provision is ambiguous but that the legislative history of the provision made it clear that Congress’s intent was to treat them as miscellaneous itemized deductions subject to the 2% floor.

Sec. 215: Alimony, etc., payments

In Aragoni,24 the Tax Court held that payments of an ex-spouse’s attorneys’ fees in connection with a 2017 divorce proceeding were not deductible as alimony. Under Sec. 71(b)(1)(D) (subsequently repealed), payments are not considered alimony if the liability for the payments would continue even if the payee spouse died. Here, the Tax Court concluded, based on reviewing the divorce instrument and California law, that the taxpayer’s obligation to pay his ex-spouse’s attorneys’ fees of $15,000 would survive her death. Therefore, the payments were not deductible as alimony.

Note: Alimony is no longer deductible for divorce or separation agreements executed, or in some cases modified, after Dec. 31, 2018.

Sec. 401: Qualified pension, profit-sharing, and stock bonus plans

The IRS has issued recent guidance on required minimum distributions (RMDs) from retirement accounts, including changes to the required beginning date and the 10-year rule for inherited accounts.

Required beginning date for RMDs: Under SECURE 2.0,25 the date that retirement distributions are first required was increased to age 73, effective for those reaching age 73 in 2024 or later. This means that taxpayers born in 1951 begin RMDs in 2024 and not 2023. The IRS issued Notice 2023-23 to give custodians additional time to correct Form 5498, IRA Contribution Information, reporting as to the first year for RMDs. In July 2023, the IRS followed up with Notice 2023-54, which allowed those taxpayers born in 1951 to return their RMDs by Sept. 30, 2023, and have them treated as a taxfree 60-day rollover.

The IRS also indicated that qualified plan administrators were allowed to follow this new date. Qualified plans could lose that status if they fail to follow the current law, so it is necessary for the IRS to let administrators know when a requirement has been changed.

Beneficiaries and the 10-year rule: Proposed regulations issued in 2022 indicated that beneficiaries subject to the 10-year rule had to take RMDs beginning the year after the account owner’s death if that owner had been taking RMDs before they died. This was a controversial provision made worse by the fact that many of those beneficiaries were already late in taking RMDs. The IRS issued Notice 2022-53 in October 2022, indicating that no RMDs would be required for those beneficiaries for 2022 or 2023 and that final regulations would be forthcoming. Notice 2023-54 also gave until 2024 for that class of beneficiaries to begin RMDs for an inheritance in 2020 or later.

Sec. 408: Individual retirement accounts

In Gomas, a district court held that the taxpayers, Dennis and Suzanne Gomas, could not deduct $1,174,020 that they withdrew from their IRA and pension accounts, of which they were defrauded by Suzanne Gomas’s daughter, Suzanne Anderson.26 Dennis Gomas inherited a business from his brother. After firing the business manager, who was stealing from the couple, they moved the business to Florida, and Anderson began helping in the business. Dennis Gomas retired, and Anderson took over the business.

Anderson created an elaborate scheme, convincing the Gomases that former employees were using Dennis Gomas’s personal information to defraud internet customers. To make the ruse more convincing, she posed as an intermediary with an attorney to represent the couple, sending them fake emails purportedly from the attorney. She also fabricated legal and business documents to perpetuate her fraud.

The Gomases withdrew money from their retirement accounts to fund the fictitious legal expenses that Anderson claimed they owed. In all, she defrauded them of almost $2 million. Friends of the Gomases who also were defrauded reported the scam to them, and the couple went to the police, who uncovered the extent of the fraud. Anderson was convicted and given a prison sentence.

On the Gomases’ 2017 tax return, they reported more than $1.17 million of pension and IRA withdrawals. They amended the return in 2020 to report that they issued a Form 1099-MISC, Miscellaneous Information, to Anderson to report the $1.17 million as deductible compensation and claimed a refund of more than $400,000. The IRS denied the claim, and the Gomases sued in district court.

In court, the Gomases argued that Anderson should be considered to have received the IRA and pension distributions because she enjoyed their benefit through her fraudulent scheme. Alternatively, they contended they could deduct the amounts as ordinary and necessary business expenses, since they believed that Anderson was using them to resolve legal matters related to their closed business.

The court disallowed the deduction due to the fact the business had been closed prior to 2017, there was no profit motive, and the amounts were not used to pay any actual business expenses (or any legal fees). Rather, the purpose was, the Gomases thought, to shield Dennis Gomas from personal liability and arrest.

Although the Gomases were, in the court’s words, “astonishingly” liable for tax on the stolen funds, and this result “seems unjust,” they nonetheless could not “recharacterize the facts from what they are — a theft loss — to something else.” The court noted that, under the TCJA, individual theft loss deductions are suspended for tax years 2018 through 2025.

The estate of the late actor James Caan ran into trouble with the rollover rules in Estate of Caan.27 The case underscores the need for taxpayers to exercise care when they invest their IRAs in assets that are not readily tradeable.

Caan had two IRAs with the Union Bank of Switzerland (UBS); one held stocks and bonds, but the other held a hedge fund partnership interest as well as stocks and bonds. Custodians generally do not want to hold investments without a readily obtainable FMV, and custodians willing to handle those items charge higher fees. The UBS custodial agreement provided that the account owner (Caan) was required to provide the year-end FMV of the hedge fund investment every year. This was to allow UBS to properly complete Form 5498 for the IRA.

Although an FMV was furnished as of Dec. 31, 2013, Caan did not provide the Dec. 31, 2014, FMV during 2015, and UBS was unable to obtain it from the hedge fund. In accordance with the custodial agreement Caan had signed, UBS resigned as the IRA custodian and informed him that he had 60 days to roll the IRA over to another custodian. Further correspondence indicated that the resignation was effective Nov. 25, 2015, and the rollover period would expire 60 days later. The letter also provided the names of two IRA custodians who handled IRA investments such as the hedge fund partnership. After receiving no response, UBS issued Form 1099-R in January 2016, valuing the IRA at the $1.9 million value provided for Dec. 31, 2013, for the hedge fund and the stocks and bonds at current value.

Caan had delegated his financial affairs to a couple of managers and advisers. Beginning in 1999, Caan hired a firm to act as his business manager. Individuals handling his account were CPAs. The firm received his mail and dealt with all financial matters, including preparing his income tax returns and acting as a liaison between Caan and lawyers, investment advisers, and others who assisted him. His investment adviser had moved Caan’s IRAs to UBS in 2008 from two previous brokerage firms he worked at. He left UBS in 2015 and moved to Merrill Lynch. He convinced Caan to transfer the IRAs to Merrill Lynch in October 2015, and everything was transferred to one new IRA, except for the partnership. Merrill Lynch would not accept the partnership interest as an IRA asset.

In March 2016, the business management firm contacted Merrill Lynch because the hedge fund still listed UBS as the custodian. Merrill Lynch personnel found that UBS no longer had any assets belonging to Caan’s IRAs. In December 2016, Caan’s Merrill Lynch broker directed the hedge fund to liquidate the investment and transfer the funds to the Merrill Lynch IRA for Caan.

The 2015 return prepared by the business management firm for Caan reported about $2.3 million in IRA distributions, with only $388,000 as taxable. The balance was shown as a rollover. The hedge fund liquidation proceeds were received by Caan’s Merrill Lynch IRA early in 2017 and totaled $1.5 million.

The IRS issued a CP2000 notice, wanting tax on the $1.9 million reported on Form 1099-R that was treated as a rollover. The business manager requested that UBS revise the 1099-R, but it would not.

The business manager next requested an IRS private letter ruling allowing more than 60 days to complete the rollover. The request was filed three months after the IRS issued a notice of deficiency and just a few days before Caan filed his Tax Court petition in response to the notice. The IRS denied the ruling request while Caan’s Tax Court case was pending.

The Tax Court held that the partnership interest was distributed in 2015, which was consistent with the reporting on Caan’s tax return. The receipt of the proceeds from liquidation of the partnership interest in 2017 did not change the value of the income to be reported or make it nontaxable. Sec. 408(d)(3)(A)(i) allows a distribution to be nontaxable if “the entire amount received (including money and any other property)” is contributed to another IRA within 60 days. If the partnership interest had been contributed to another IRA within 60 days of the UBS resignation in 2015, the distribution would have been a nontaxable rollover distribution. However, that did not happen. The Tax Court held that Caan’s estate, which succeeded Caan in the case upon his death in 2022, was liable for tax in 2015 on the partnership interest’s value at the time UBS distributed it.

As this case highlights, taxpayers need to be particularly careful when investing in assets not readily tradeable in their IRAs, and they especially need to read all mail received from the custodian and the IRS to diminish problems before a visit to Tax Court is necessary.

Sec. 414: Definitions and special rules

The IRS granted transition relief from a new requirement that high-income wage earners must designate their catch-up retirement contributions as Roth contributions.28

SECURE 2.0 made changes to the rules for qualified plans that have a Roth provision. Participants over age 50 are allowed to have their catch-up contribution allocated to the Roth portion of the qualified plan beginning in 2024. Further, participants with wages greater than $145,000 (inflation-adjusted) the prior year are required to have those catch-up amounts allocated to the Roth portion. This means that the catch-up would go from a pretax deferral to a post-tax amount. (This new requirement does not apply to SEP and SIMPLE IRA plans.)

On Aug. 25, 2023, the IRS issued Notice 2023-62 to delay until 2026 the effective date for requiring high-income wage earners to designate their catch-up contributions as Roth.

Sec. 1411(c): Net investment income

In Christensen,29 the Court of Federal Claims allowed U.S. citizens residing in France a foreign tax credit against the net investment income tax, based on the 1994 U.S.–France Tax Treaty.

The issue in the case arose because Sec. 27 and Sec. 901(a) state that foreign tax credits can only be used against taxes imposed by Chapter 1 of the Code. The net investment income tax under Sec. 1411 is imposed by Chapter 2A of the Code, and therefore a taxpayer would not be allowed to offset the net investment income tax with a foreign tax credit under these provisions.

The Christensens challenged this result. They were U.S. citizens residing in France who sought a refund for net investment income taxes paid on foreign-source passive income. Paragraph 2(a) of Article 24 of the 1994 Treaty states that the allowance of foreign tax credits is subject to the provisions and limitations of U. S. law. As explained above, Secs. 27 and 901(a) do not allow this credit against net investment income tax. But Paragraph 2(b) of Article 24 of the 1994 Treaty describes how the tax credit should be applied between the United States and France, known as the “three-bite” rule, and does not contain the same limitations as Paragraph 2(a).

To address the conflict between the treaty and U.S. statutory provisions, the court relied on relevant precedential cases, which instruct courts to interpret the Code in a way that avoids conflict with international obligations. Sec. 6511(d)(3)(A) recognizes a distinction between foreign tax credits under Sec. 901(a) and foreign tax credits under any treaty to which the United States is a party. This distinction indicates that a foreign tax credit may be allowed by treaty provisions that is not also allowed by Sec. 901(a). Relying on this interpretation, the court allowed the plaintiffs a foreign tax credit against net investment income tax based on Paragraph 2(b) of Article 24 of the 1994 U.S.–France Tax Treaty.

Footnotes

1Sowards, T.C. Memo. 2023-99.

2Balint, T.C. Memo. 2023-118.

3Doggart, T.C. Summ. 2023-25.

4Sinopoli, T.C. Memo. 2023-105.

5Kraske, T.C. Memo. 2023-128.

6Sec. 165(c)(3) and Regs. Sec. 1.165-1(d)(3). The case concerns the taxpayer’s 2012 tax year. However, itemized deductions by individual taxpayers of casualty and theft losses are not allowable for tax years 2018 through 2025 unless attributable to a federally declared disaster (Sec. 165(h)(5)(A), added by the law known as the Tax Cuts and Jobs Act (TCJA), P.L. 115-97).

7Johnson, No. 2:22-cv-00217-BHH (D.S.C. 9/18/23).

8Braen, T.C. Memo. 2023-85.

9Tucker, T.C. Memo. 2023-87.

10Murfam Enterprises LLC, T.C. Memo. 2023-73.

11Murphy, T.C. Memo. 2023-72.

12Sec. 170(h)(1).

13Glade Creek Partners, LLC, T.C. Memo. 2020-148.

14Hewitt, 21 F.4th 1336 (11th Cir. 2021), in which the Eleventh Circuit held that the IRS’s interpretation of Regs. Sec. 1.170A-14(g)(6)(ii) was arbitrary and capricious and violated the procedural requirements of the Administrative Procedure Act.

15Glade Creek Partners, LLC, No. 21-11251 (11th Cir. 8/22/22).

16Glade Creek Partners, LLC, T.C. Memo. 2023-82.

17Mill Road 36 Henry, LLC, T.C. Memo. 2023-129.

18I.e., subject to the audit procedures under the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA), P.L. 97-248.

19Sec. 170(h)(4)(A)(ii).

20Sec. 170(h)(4)(A)(iii). The remaining two purposes are preservation of (1) land areas for outdoor recreation by, or education of, the general public or (2) a historically important land area or certified historic structure (Secs. 170(h)(4)(A)(i) and (iv)).

21Bryan, T.C. Memo. 2023-74.

22Gregory, T.C. Memo. 2021-115.

23Gregory, 69 F.4th 762 (11th Cir. 2023).

24Aragoni, T.C. Summ. 2023-3.

25The SECURE 2.0 Act, Division T of the Consolidated Appropriations Act, 2023, P.L. 117-328.

26Gomas, No. 8:22-cv-1271-TPG-TGW (M.D. Fla. 7/17/23).

27Estate of Caan, 161 T.C. No. 6 (2023).

28Sec. 414(v)(7).

29Christensen, No. 20-935T (Fed. Cl. 9/13/23).

Contributors

Elizabeth Brennan, CPA, is a practitioner in New Orleans. Jodi Eckhout, CPA, is a shareholder with Woods & Durham, Chartered, in Holdrege, Neb. Mary Kay Foss is a CPA in Carlsbad, Calif. Amie Kuntz, CPA, is a partner in the national tax group of RubinBrown LLP. Michael Levy, CPA, is a partner with Crowe LLP in New York City. Dana McCartney, CPA, is a partner with Maxwell Locke & Ritter LLP in Austin, Texas. Tracy Tinnemeyer, J.D., is senior manager, Deloitte Washington National Tax, in Washington, D.C. Robert L. Tobey, CPA, is managing member of Robert L. Tobey, CPA, LLC, in New York City. McCartney is the chair, and the other authors are members, of the AICPA Individual and Self-Employed Tax Technical Resource Panel. For more information about this article, contact thetaxadviser@aicpa.org.

AICPA & CIMA RESOURCES

CPE self-study

Individual Tax Fundamentals — Tax Staff Essentials

Tax Staff Essentials — Individual Taxation Bundle

Tax Section resources

Individual Income Taxation library

For more information or to make a purchase, visit aicpa-cima.com/cpe-learning or call 888-777-7077.

{kind=link}