Does an EIN/name mismatch invalidate a refund claim?

Editor: Melissa L. Wiley, J.D.

The IRS rejects or delays processing millions of refund claims each year due to technical defects, costing taxpayers billions in rightful refunds. Frequently, such claims become time–barred before the errors can be corrected. In a 2024 Annual Report to Congress, the national taxpayer advocate (NTA) identified refund claim processing as a serious problem facing taxpayers, causing them to lose legitimate refunds due to minor errors that could be easily corrected (p. 26). Such errors are common because refund claims are governed by strict technical requirements that can trap even experienced practitioners. This column examines a discrete but critical issue that affects many business taxpayers: whether a refund claim filed under the correct business’s name but incorrect employer identification number (EIN) satisfies statutory requirements under Sec. 6402.

Sec. 6402(a) provides that the IRS “may credit the amount of [an] overpayment, including any interest allowed thereon, against any liability” and shall refund any balance to the person who made the overpayment. This statutory authority creates the framework for administrative refund claims. However, the right to a refund is not unlimited. Congress has imposed specific requirements that taxpayers must follow to access this remedy. When Sec. 6402 addresses various types of offsets and collections, it uses the phrase “named person” without any reference to taxpayer identification numbers (see Sec. 6402(d)(1) (“[u]pon receiving notice from any Federal agency that a named person owes a past–due legally enforceable debt”); Sec. 6402(e)(1) (“[u]pon receiving notice from any State that a named person owes a past–due, legally enforceable State income tax obligation”)). This use of “named person” throughout the statute suggests Congress intended the taxpayer’s name to be the critical element for identifying the proper recipient of a refund.

As discussed below, business taxpayers whose refund claims are stymied by a mismatch caused by an incorrect EIN can take various steps to address the problem and obtain the refund to which they are otherwise entitled.

The regulatory framework: Regs. Sec. 301.6402-2

A good starting point for this discussion is to look at what the regulations say.

Elements of a refund claim

Regs. Sec. 301.6402–2 goes into detail about specific administrative requirements that govern the form in which refund claims must be presented to the IRS:

- Claims must be made in writing.

- Claims must set forth in detail each ground upon which a credit or refund is claimed. They must include facts sufficient to apprise the IRS of the exact basis for the claim. The statement of the grounds and facts must be verified by a written declaration that it is made under the penalties of perjury. Taxpayers must provide enough specific information for the IRS to evaluate the merits of their claim without conducting an independent investigation.

- A separate claim must be made for each tax year or period. This means taxpayers cannot bundle multiple years into a single refund claim, even if the issue is identical across years.

However, absent from the second requirement above (Regs. Sec. 301.6401–2(b)(1)) is any explicit requirement that the taxpayer’s EIN be correct. The regulation requires sufficient facts to “apprise the Commissioner,” which should be satisfied when the correct taxpayer name is provided along with all substantive information about the overpayment.

The Treasury regulations require that refund claims be made on the form prescribed by the IRS for the particular type of tax at issue. This is a jurisdictional requirement. For individual income tax refunds, Regs. Sec. 301.6402–3(a)(2) specifically requires the use of Form 1040, U.S. Individual Income Tax Return, or Form 1040–X, Amended U.S. Individual Income Tax Return. Corporate income tax claims require Form 1120, U.S. Corporation Income Tax Return, or 1120–X, Amended U.S. Corporation Income Tax Return (Regs. Sec. 301.6402–3(a)(3)).

While form selection gets attention in published cases, in practice, taxpayer identification errors are a common reason refund claims fail, and these failures often go unnoticed until it is too late to correct them. Regs. Sec. 301.6402–2(b)(1) requires that every claim contain information sufficient to identify the taxpayer and the basis for the refund, but the regulation does not state that an EIN must be correct when the taxpayer’s name correctly identifies who is seeking the refund. The distinction between requiring a correct name versus a correct EIN in some cases determines whether taxpayers can recover millions of dollars in overpayments or lose them to procedural technicalities that the IRS could easily resolve through basic research.

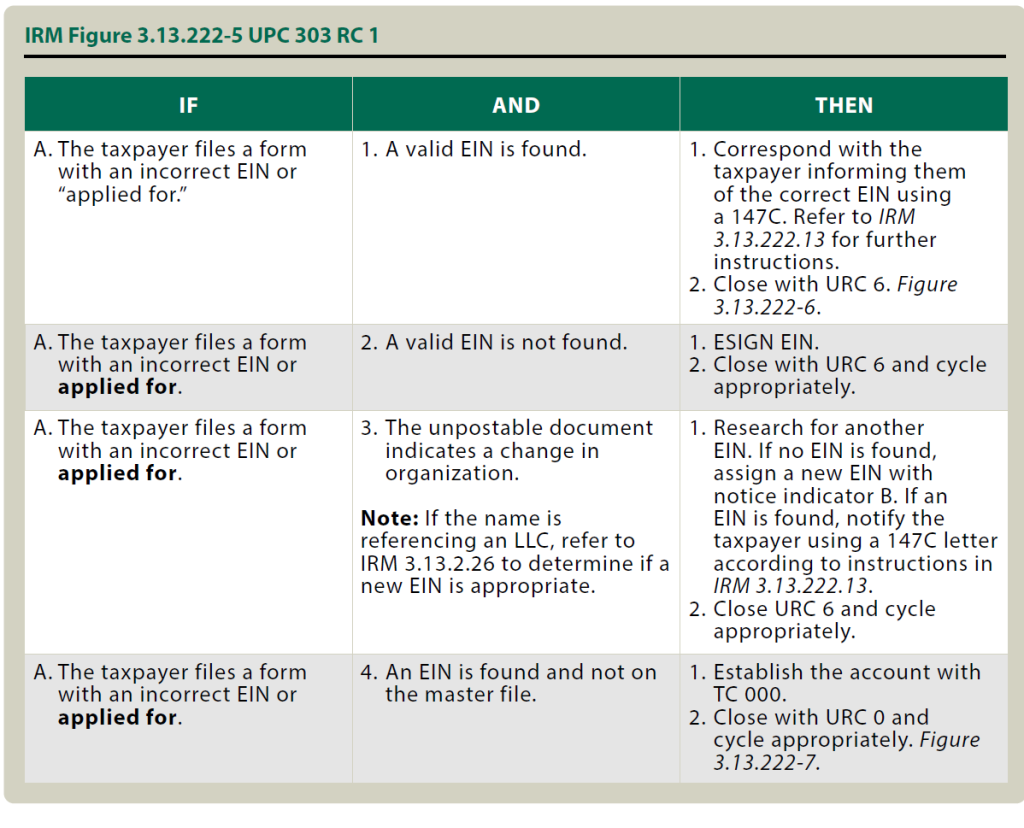

IRM Section 3.13.222.45 research requirements

When the IRS receives a return or refund claim with mismatched name and EIN information, the Internal Revenue Manual (IRM) requires IRS personnel to follow specific procedures to discover the correct tax module to post the tax return rather than mechanically rejecting the claim (IRM §3.13.222.45 (Jan. 1, 2023)). See the table, reproduced from this IRM, showing a portion of Figure 3.13.222–5 UPC 303 RC 1, to follow the sequence of actions IRS personnel are instructed to take in this and related instances.

These procedures acknowledge that taxpayers may inadvertently use incorrect EINs, particularly in complex corporate structures or following mergers and acquisitions, and that such mistakes occur in practice due to human error. The IRM’s requirement to research and correct such errors before rejecting claims or posting claims under the incorrect EIN demonstrates that the IRS should do research before posting tax returns with an EIN/name mismatch to improper tax modules. Despite these clear procedures, the NTA has reported that in thousands of cases annually, the IRS has improperly rejected refund claims (National Taxpayer Advocate, Annual Report to Congress, 2024 (documenting systemic failures in return processing)).

The consequences of name/EIN mismatches are illustrated by this hypothetical example:

Example: XYZ Corp. was acquired by ABC Corp. in September 2020, requiring XYZ to file a short–period return for September through December 2020. The tax preparer, knowing about the acquisition and having ABC’s information, inadvertently used ABC’s EIN (which was obtained in 2021) on XYZ’s 2020 year–end return, though the return correctly showed XYZ’s name. ABC did not even have an EIN in 2020 and was not required to file any tax returns in 2020, making the error obvious upon examination. The return showed XYZ owed $260,000 but had made payments of $640,000, entitling it to a $380,000 refund.

If the IRS posted the return to ABC’s EIN without conducting the research required by IRM Section 3.13.222.45, the following would occur: The $640,000 in payments would remain credited to XYZ’s correct EIN; the $260,000 liability would be assessed against ABC’s EIN; collection actions could begin against ABC for taxes it never owed; and XYZ’s $380,000 refund effectively could be lost. If XYZ later files a corrected return with the proper EIN and the statute of limitation under Sec. 6511 has expired, the IRS would deny the refund claim as untimely (Sec. 6511(a)). The IRS’s failure to follow IRM research procedures can create a huge problem, transforming a simple clerical error into a $380,000 loss for the taxpayer.

The informal claim doctrine as a safety valve for name/EIN mismatches

In the situation described above, one of the ways the taxpayer may be able to “rescue” the imperfect but timely refund claim filed by XYZ Corp. is to make “the informal claim doctrine” argument. The informal claim doctrine was established by the Supreme Court in Kales,314 U.S. 186, 194 (1941), and it recognizes that formal defects in a refund claim may be cured by subsequent amendment even after the limitation period has expired if the original filing provided adequate notice to the IRS about the taxpayer seeking the refund.

When a refund claim contains the correct taxpayer’s name and all substantive information except the EIN, it should qualify as an informal claim that can later be perfected, even if it is perfected after the statute of limitation has expired but before the claim is formally denied by the IRS. The doctrine requires that the informal claim be in writing, be filed timely within Sec. 6511 limitations, provide adequate notice of the refund sought and its basis, and be subsequently perfected with a formal claim.

The Supreme Court held in Angelus Milling Co., 325 U.S. 293, 297–98 (1945), that the IRS may waive formal defects by investigating and acting upon a claim’s merits. When the IRS processes a return, posts it to an account (even the wrong one), and takes collection action based on that return, it has clearly understood and acted upon the filing, potentially waiving any formal defect in the EIN. In the XYZ Corp. example, the IRS’s assessment of tax against ABC and the initiation of collection procedures demonstrate that the Service received, processed, and understood the return. It simply posted it to the wrong account due to its failure to follow IRM research procedures.

Because the informal refund claim doctrine is a court–created doctrine, in many cases taxpayers would not gain the IRS’s full attention with this argument until the case is reviewed by the IRS Independent Office of Appeals or during a refund litigation process. Based on the authors’ experience, the first–level reviewers are not receptive to the informal refund claim argument. This may be because the first–level reviewers are primarily compliance–oriented and rarely consider hazards–of–litigation arguments that are usually reviewed at the appeals level.

TAS can help

The name–versus–EIN distinction exemplifies a crisis in tax administration where mechanical processing causes taxpayers to forfeit legitimate refunds due to minor clerical errors the IRS could easily correct. Sec. 6402’s “named person” language and Regs. Sec. 301.6402–2(b)(1)’s requirement to “apprise the Commissioner” are satisfied when correct names and substantive information are provided, regardless of EIN accuracy.

Taxpayers and practitioners facing wrongful refund denials due to EIN mismatches should consider contacting the Taxpayer Advocate Service (TAS), an independent organization within the IRS that assists when normal administrative channels fail. The TAS can issue taxpayer assistance orders compelling the IRS to properly research and process claims, particularly when taxpayers face economic harm from wrongful denials. To request assistance, taxpayers should submit Form 911, Request for Taxpayer Advocate Service Assistance, detailing how the IRS’s failure to follow its own procedures has caused significant hardship, especially when refund delays exceed 30 days beyond normal processing times.

Until Treasury clarifies that correct taxpayer names satisfy refund claim requirements and the IRS implements systematic reforms, practitioners must protect clients’ refund rights through preventive measures, advocacy, and strategic use of available resources, including TAS intervention.

Contributors

Alina Solodchikova, J.D., LL.M., LL.B., is a principal and leader of the tax controversy practice of RSM US LLP in Washington, D.C. Alice Tsvilikhovski, J.D., LL.M., is a tax controversy supervisor with RSM US LLP in New York City. Melissa L. Wiley, J.D., is a partner with Kostelanetz LLP in Washington, D.C. Solodchikova is vice chair, and Wiley is chair, of the AICPA IRS Advocacy & Relations Committee. For more information about this column, contact thetaxadviser@aicpa.org.