Current Developments in Taxation of Individuals: Part 1

This semiannual update surveys recent federal tax developments involving individuals. It summarizes notable cases, rulings, and guidance on a variety of topics issued during the six months ending October 2025. The update was written by members of the AICPA Individual and Self–Employed Tax Technical Resource Panel. It begins with selected new and changed provisions of H.R. 1, P.L. 119–21, known as the One Big Beautiful Bill Act (OBBBA) and subsequently, for developments in prior–law provisions, is arranged in Code section order.

A quick reference chart summarizing OBBBA changes is available here.

OBBBA updates

On July 4, 2025, President Donald Trump signed the OBBBA into law. The act introduced many new provisions affecting individual taxpayers and permanently extended or modified many provisions from the Tax Cuts and Jobs Act (TCJA), P.L. 115–97, that had been scheduled to sunset at the end of 2025, including the following:

Tax brackets and tax rates

The TCJA not only reduced the top income tax rate from 39.6% to 37% but also modified the income tax brackets (causing more taxable income to be subject to lower rates). Both changes were scheduled to sunset after Dec. 31, 2025, but the OBBBA makes these updates permanent. In addition, the act provides the 10% and 12% income tax brackets with an additional year of inflation adjustments. The IRS reflected these updates in Rev. Proc. 2025–32, which included the inflation–adjusted income tax brackets for tax year 2026.

Personal exemptions

For tax years 2018 through 2025, the TCJA suspended a deduction that had been available for the taxpayer, spouse, and each qualifying dependent. In 2017 the amount was $4,050 per person. The OBBBA permanently eliminates this deduction.

Standard deduction

The standard deduction was nearly doubled by the TCJA for tax years 2018 through 2025 but was set to revert to pre–TCJA amounts beginning in 2026. The OBBBA made the increased standard deduction amounts permanent, with additional slight increases for tax year 2025.

Alternative minimum tax (AMT) exemption

The TCJA increased AMT income exemption and phaseout thresholds for tax years 2018 through 2025, making the AMT less applicable. The OBBBA made those higher exemption amounts permanent but, beginning in tax year 2026, reverts the exemption phaseout threshold to 2018 levels of $500,000, or $1 million for married taxpayers filing jointly (indexed for inflation thereafter).

Child tax credit

The OBBBA permanently increased the child tax credit to $2,200 per child, starting with the 2025 tax year ($1,700 of this amount being refundable). The credit is indexed for inflation and subject to an overall income phaseout threshold of $200,000 ($400,000 in the case of married taxpayers filing a joint return). A $500 nonrefundable credit is also available for all dependents other than a qualifying child.

Dependent care annual exclusion

The OBBBA provides an increase to the annual income exclusion cap for dependent care assistance programs, such as pretax dependent care flexible spending arrangements for day care. A $5,000 limit had been in place since 1986, and other than a temporary change during the COVID–19 pandemic, had not increased. Effective in 2026, the $5,000 dependent care exclusion increases to $7,500.

Child and dependent care tax credit

Also starting in 2026, the child and dependent care tax credit is increased for those with lower income. The maximum percentage of eligible expenses in the credit calculation increases from 35% to 50% (phased down to 35% for taxpayers with $15,000 or more in adjusted gross income (AGI) and further reduced for taxpayers with AGI above $75,000). The maximum eligible expenses of $3,000 for one qualifying individual or $6,000 for two or more were not changed.

Modifications to charitable contributions

60% AGI limitation extended: The TCJA temporarily increased the AGI cap on cash contributions to public charities and donor–advised funds from 50% to 60% for tax years beginning after Dec. 31, 2017. This provision was originally set to expire at the end of 2025, but the OBBBA makes the 60% AGI limit permanent.

Charitable deduction for nonitemizers: For tax years 2020 and 2021, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, P.L. 116–136, enabled nonitemizing taxpayers to claim a $300 deduction for cash contributions to public charities ($600 for married taxpayers filing jointly for contributions made in 2021). The OBBBA not only reinstates the charitable deduction for nonitemizing taxpayers for tax years beginning after Dec. 31, 2025, but also increases the deduction to $1,000 ($2,000 for married taxpayers filing jointly).

0.5% floor on charitable contributions: Charitable contributions made by individuals have historically been subject to an overall limitation (i.e., a ceiling) based on a percentage of AGI. As indicated above, the deduction available for cash contributions to public charities and donor–advised funds is currently limited to 60% of AGI, with any excess carried forward for five years; separate percentage limitations apply, depending upon the type of property donated and the type of charitable donee. For tax years beginning after Dec. 31, 2025, the OBBBA introduces a new, separate limitation, a floor on an individual’s charitable contribution deduction equal to 0.5% of their “contribution base,” which is defined as AGI without regard to any net operating loss (NOL) carrybacks under Sec. 172.

As a result of the new floor, individual taxpayers may claim a charitable deduction only to the extent that the aggregate of their contributions exceeds 0.5% of AGI; thus, an itemizing taxpayer with an AGI of $100,000 receives no benefit for their first $500 of charitable contributions ($100,000 × 0.5%). The OBBBA provides that charitable contributions disallowed by the floor are carried over to subsequent years but only if the taxpayer is also carrying forward an excess charitable contribution that was already limited by the ceiling. Note that the 0.5% floor applies only to taxpayers who itemize deductions; it does not apply to individuals claiming the special $1,000 ($2,000 for married taxpayers filing jointly) charitable deduction for nonitemizing taxpayers described earlier.

35% cap on tax benefit of itemized deductions: For tax years prior to Jan. 1, 2018, Sec. 68 imposed a limitation (colloquially referred to as the Pease limitation) on itemized deductions for taxpayers whose AGI exceeded certain statutory thresholds. The TCJA suspended the Pease limitation for tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026. Rather than allow the Pease limitation to come back into effect, the OBBBA repealed the provision and replaced it with a new limitation on itemized deductions for taxpayers in the highest income tax bracket.

The practical effect of the new limitation is to reduce the tax benefit of itemized deductions for those in the top bracket from 37% to 35%; this is accomplished by requiring taxpayers to reduce the amount of their itemized deductions by 2/37ths of the lesser of (1) the taxpayer’s otherwise allowable itemized deductions or (2) the excess of the taxpayer’s taxable income (increased by otherwise allowable itemized deductions) over the dollar amount at which the top tax rate bracket begins with respect to the taxpayer. For example, an individual in the highest income tax bracket with $1 million of itemized deductions may receive a tax benefit of $370,000 in 2025 from those deductions ($1,000,000 × 37%), compared to a $350,000 tax benefit in 2026 from those same deductions ($1,000,000 × 2/37 = $54,054; $1,000,000 – $54,054 = $945,946; $945,946 × 37% = $350,000 tax benefit). Notably, the new limitation has no carveouts for charitable contributions or any other itemized deductions. Therefore, taxpayers in the highest income tax bracket may see their charitable contributions subject to two separate and independent limitations beginning in 2026: first, the new 0.5% floor and, second, the new limitation on itemized deductions.

Miscellaneous 2% itemized deductions

The TCJA temporarily suspended certain itemized deductions that were subject to a 2%-of–AGI floor. Unreimbursed employee business expenses, investment–related expenses, and tax preparation fees were among these expenses. Starting in 2026, unreimbursed employee expenses of eligible elementary and secondary educators are removed from the list of miscellaneous itemized deductions.

Personal casualty losses

Prior to the TCJA, personal casualty or theft loss deductions were available to itemizers if they experienced a sudden, unexpected, or unusual event. However, the TCJA limited those deductions to federally declared disaster events for tax years 2018 through 2025. The OBBBA made the TCJA changes permanent but adds state–declared disasters beginning in 2026.

Qualified opportunity zones

The opportunity zone program was enacted as part of the TCJA to spur economic development in lower–income and distressed communities by providing tax incentives to those who invest in qualified opportunity funds (QOFs). Taxpayers who invested capital gains into a QOF were afforded several key tax benefits, including deferral of the gain until Dec. 31, 2026; 10% and 15% basis increases for investments held for five years and seven years (respectively); and permanent elimination of any capital gains ultimately realized on an investment held for at least 10 years.

The OBBBA permanently extends the opportunity zone program for investments made after Dec. 31, 2026, with certain modifications. Among other things, any deferred gains rolled into an opportunity zone will now be recognized on the earlier of (1) five years after the date of the initial investment or (2) the date the investment is sold. Investments that satisfy the five–year holding period requirement will also be eligible for a 10% basis step–up (30% in the case of an investment in a qualified rural opportunity fund), but the additional 5% basis step–up for investments held seven years has been eliminated.

Taxpayers who hold their investment for at least 10 years will still be eligible to exclude their gain by electing to increase their basis in the investment to fair market value (FMV) on the date of sale; however, if the taxpayer’s holding period is longer than 30 years, the election to increase the investment’s basis to FMV will be capped at the FMV of the investment on the 30–year anniversary date of the investment. Thus, any appreciation in the opportunity zone fund investment after the 30–year anniversary date will be subject to income tax once the investment is sold.

Qualified small business stock (QSBS)

Shareholders of QSBS who hold their stock for at least five years can exclude all or a portion of capital gains on the sale of their stock for the greater of $10 million or 10 times the basis of the stock. The QSBS exclusion’s requirements include that the stock must be of a domestic C corporation and acquired by the shareholder by original issue after 1993, with the corporation not engaged in a disqualified trade or business and subject to a $50 million asset limit.

The OBBBA enhanced the QSBS exclusion for stock acquired after July 4, 2025. These changes include:

- A partial exclusion of 50% for stock held three years, or 75% for stock held four years;

- An increased per-issuer gain limitation amount of $15 million, indexed for inflation, versus $10 million previously; and

- An increased maximum asset limit of $75 million, versus $50 million previously.1

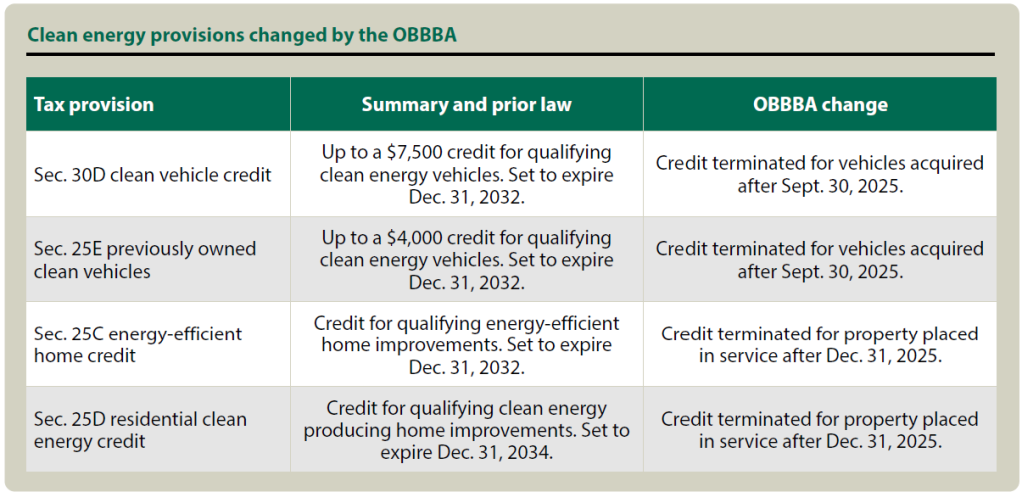

Clean energy credits affected by the OBBBA

While the Inflation Reduction Act of 2022, P.L. 117–169, greatly enhanced and extended clean energy tax credits and incentives, the OBBBA reversed course and ended several much earlier. See the table “Clean Energy Provisions Changed by the OBBBA,” below, for a list of these provisions that may affect individuals.

Sec. 199A: Qualified business income deduction

The qualified business income (QBI) deduction allows a 20% individual–level deduction on passthrough income, certain real estate investment trust dividends, and publicly traded partnership income. Created by the TCJA, it was part of the individual provisions set to expire at the end of 2025. The OBBBA made the deduction permanent with increased phaseout amounts of $150,000 for married taxpayers filing jointly and $75,000 for all others. Additionally, a new minimum deduction of $400 will be allowed beginning in 2026 for taxpayers who have at least $1,000 of QBI from an activity in which they materially participate.

Sec. 461(l): Limitation on excess business losses of noncorporate taxpayers

The TCJA imposed a loss limitation for passthrough business owners from 2018 through 2025. Later legislation extended the expiration date to 2028, and now the OBBBA makes the limitation permanent. Disallowed losses become NOL carryforwards. Net business losses over a certain amount are limited in the current year; for 2025, the amounts are $313,000, or $626,000 for married taxpayers filing jointly.

Sec. 1245: Gain from dispositions of certain depreciable property

The OBBBA added a paragraph to Sec. 1245, which treats certain disposals of capital assets as ordinary income, effective after July 4, 2025. The law has added to the definition of Sec. 1245 property “any qualified production property (as defined in section 168(n)(2)).”2

Qualified production property is nonresidential real property (1) that is used by the taxpayer as an integral part of a qualified production activity; (2) that is placed in service in the United States or any possession of the United States; (3) the original use of which commences with the taxpayer; (4) the construction, reconstruction, or erection of which by the taxpayer begins after Jan. 19, 2025, and before Jan. 1, 2029; (5) a portion of which is designated by the taxpayer in an election; and (6) generally, is placed in service after July 4, 2025, and before Jan. 1, 2031. Since Sec. 168 provides for a special allowance of a 100% deduction of this type of property, Sec. 168(n)(5) states that Sec. 1245 shall be applied to this type of property to have ordinary income recapture if disposed of during the 10–year period beginning on the date that any qualified production property is placed in service.

New temporary deductions for tips, overtime, vehicle loan interest, and seniors

For 2025–2028, taxpayers may be eligible for new below–the–line deductions: up to $25,000 of qualified tips; up to $12,500 ($25,000 in the case of a joint return) of overtime premium pay; up to $10,000 of interest on loans for new, U.S.-assembled vehicles; and an additional senior deduction of up to $6,000 if they are age 65 or older. These new deductions are available either to those who itemize or those who claim the standard deduction. Each deduction is subject to income phaseouts and specific eligibility rules.

State and local tax (SALT) deduction

The SALT deduction cap is increased in 2025 from $10,000 to $40,000 for both single and joint filers, phased down to $10,000 for filers with modified adjusted gross income between $500,000 and $600,000. The $40,000 limitation and phaseout thresholds increase by 1% each year until 2029. After 2029, the SALT cap reverts to $10,000 for single and joint filers (in the case of a married person filing separately, all the preceding dollar amounts are half those for single and joint filers). This may affect whether it is beneficial for clients to itemize deductions and their overall tax planning.

Non-OBBBA items

Sec. 2(b): Definition of head of household

Tax Court denies head–of–household filing status to married couple: The Tax Court held that a taxpayer and spouse could not file as heads of household because they were still legally married during the years at issue.3

The taxpayers, Garaad Mohamed Muse and Shukri Jeylani Abdalla, married in Kenya in 1994. Both taxpayers subsequently moved to Minnesota and filed joint income tax returns from 1999 until 2020, at which time they had a “ceremonial divorce” due to irreconcilable differences. The ceremonial divorce was performed in accordance with their religious tradition before two witnesses. Although the petitioners considered themselves divorced, they did not obtain a decree of dissolution of marriage from Minnesota. On their 2020 and 2021 income tax returns, Muse and Abdalla filed separately, each claiming head–of–household filing status. The couple previously had five children together, whom they both financially supported; Muse also supported his elderly father. The IRS audited their 2020 and 2021 income tax returns and determined that their filing status should be married filing separately, resulting in additional taxes and penalties.

To qualify as a head of household, the taxpayer must: (1) be unmarried at the end of the tax year; (2) not be a surviving spouse; and (3) maintain a household where a qualifying child or relative of the individual is a member. Before examining the second and third requirements, the court focused its attention on the first requirement, that the taxpayer be unmarried. Not only were the petitioners originally married in Kenya under foreign law, but their divorce was also settled through a religious ceremony (and not through a divorce decree approved by any Minnesota court). Thus, the Tax Court needed to determine how a foreign marriage should be analyzed for federal income tax purposes.

According to the court, a foreign marriage is normally recognized for federal income tax purposes so long as it would be recognized under the laws of at least one state, possession, or territory of the United States. A taxpayer’s marital status is typically determined in accordance with the law of their state of domicile. Under Minnesota law, a divorce does not have legal effect unless the parties obtain a decree of dissolution of marriage from a Minnesota court; thus, religious and other ceremonial divorces are not recognized under state law.

Because Muse and Abdalla were Minnesota domiciliaries during the years at issue, and because they did not obtain an official divorce decree from a Minnesota court, they were both considered married under state law and, by extension, under federal law. Accordingly, they could not claim head–of–household filing status.

Sec. 61: Adjusted gross income defined

The taxation of legal settlements continues to generate tax cases. Taxpayers often assume that legal settlements are not taxable when in fact they often are.

In Fortune–Paladino,4 the taxpayer received a settlement of $135,000 for sex discrimination and retaliation in violation of federal and Pennsylvania state law. As the Tax Court noted, the complaint only alleged “unlawful sexual harassment, discrimination, and retaliation” and requested damages for emotional distress but “made no mention of any physical injury incurred or manifestation of physical harm arising from emotional distress.” Since there were no physical injuries, the court held Sec. 104(a) did not apply, and the settlement was taxable. The court noted in its opinion that the legal fees of $54,000 were deductible.

In Mennemeyer,5 Adrienne Mennemeyer received a settlement involving “employment and/or termination of employment” that related to a Financial Industry Regulatory Authority (FINRA) arbitration case. Mennemeyer’s employer had filed a Form U5, Uniform Termination Notice for Securities Industry Registration, with FINRA. The form claimed that she was dishonest, which was the reason for her termination. In FINRA arbitration, she asserted claims for defamation, wrongful termination, unfair competition, tortious interference with business expectancy, and expungement. Mennemeyer was awarded $1.8 million in arbitration, and a settlement for $1,510,000 was reached. The settlement stated that she had no other claims against her former employer.

In the Tax Court proceedings, Mennemeyer testified that she began having health issues including a rash and fatigue during her employment. She alleged that the settlement was written to preclude her from filing a lawsuit for additional damages related to her health issues. There was no contemporaneous support for these claims. The Tax Court found that “the facts and circumstances … overwhelmingly demonstrate that the court held that the settlement was to resolve defamation and related economic claims.” Thus, the court held that the settlement proceeds were taxable since they did not fall within the Sec. 104(a) exclusion.

The deductibility of attorneys’ fees was also addressed in the case. Sec. 62(a)(20) allows for an above–the–line deduction of attorneys’ fees for a claim of unlawful discrimination. Sec. 62(e)(18)(ii) defines unlawful discrimination as an unlawful act under any provision of federal, state, or local law “regulating any aspect of the employment relationship, including claims for wages, compensation, or benefits, or prohibiting the discharge of an employee, the discrimination against an employee, or any other form of retaliation or reprisal against an employee for asserting rights or taking other actions permitted by law.” The Tax Court found that Mennemeyer’s claims against her employer for lost wages fell within this definition and allowed a deduction of the legal costs.

Sec. 83: Property transferred in connection with the performance of services

In Feige,6 the Tax Court held that the taxpayer was liable for tax and penalties related to stock transferred to her following her separation from her employer.

The taxpayer was employed by Linc Energy Operations Inc. from February 2010 through November 2014. She participated in the Linc Energy Performance Rights Plan, allowing her to receive Linc Energy stock as part of her compensation for services. During her employment, she received in August 2011 an allocation of 60,000 unvested rights in Linc Energy stock and another allocation of 400,000 unvested rights in July 2013. In 2014, Linc Energy was having financial difficulties and on Nov. 24, 2014, entered into a separation agreement with the taxpayer. As part of that agreement, the taxpayer’s unvested performance rights were to be forfeited at the time of termination of her employment.

However, on Dec. 3, 2014, Linc transferred 100,000 shares of Linc Energy stock to the taxpayer. The taxpayer was unaware of the transfer until she received her December brokerage statement in January 2025 showing the shares. While the taxpayer reached out to Linc Energy employees to inquire about the potential error in issuing these shares, she did not receive an explanation, due to the fact those employees had also been terminated. Subsequently, she received a Form W–2, Wage and Tax Statement, from Linc Energy reporting an additional $75,660 in compensation related to the nonstatutory stock options. The taxpayer did not file a 2014 tax return and received a notice from the IRS in 2019 assessing a deficiency.

Sec. 83(a) provides that property transferred to a taxpayer in connection with the performance of services shall be included in the taxpayer’s gross income in the first year in which the taxpayer’s rights in the property are transferable or not subject to a substantial risk of forfeiture, at an amount equal to the excess of the FMV of the property over the amount paid for it, if applicable.

The taxpayer argued that she was not required to include the value of the Linc Energy shares in her gross income because they were transferred in error, and therefore she did not have dominion and control over them.

The Tax Court held that as of Dec. 3, 2014, (1) the taxpayer could transfer the 100,000 shares she received from Linc and (2) there was no substantial risk of forfeiture. Accordingly, the value of the disputed shares that was reported to the taxpayer on her Form W–2 should have been included in her gross income for 2014.

Sec. 117: Qualified scholarships

In Kramarenko,7 the Tax Court held that income received by a resident alien who worked at a university’s medical school on a postdoctoral fellowship was not exempt from tax under the Russia–U.S. tax treaty because she was an employee, not a grantee.

The taxpayer was from Russia, where she completed her M.S. degree in medical biophysics in 2001 and Ph.D. in biophysics in 2006. She came to the United States in 2006 after applying for and being hired in a postdoctoral fellowship position at the Medical University of South Carolina (MUSC). She obtained a J–1 visa to travel and work in the United States, which she extended twice through September 2011, when she obtained an H–1B visa valid through September 2014.

As part of her hiring process in 2006, she signed several forms as an employee, including Form W–4, Employee’s Withholding Certificate; Form W–8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals); and U.S. Citizenship and Immigration Services Form I–9, Employment Eligibility Verification. She received a salary, various employment benefits, and additional training in laboratory techniques as compensation for her services as a postdoctoral fellow. She worked in various laboratories at MUSC over the years but in each case signed as an employee an “assignment information sheet” that detailed the terms of her employment, including her monthly salary, method of payment, deductions, and benefits.

During her time at MUSC, the principal researcher in the labs where she worked applied for and received grants from organizations and agencies such as the American Heart Association and the National Institutes of Health to fund laboratory expenses, including the taxpayer’s salary. The taxpayer worked on a variety of experiments, including treating living cells with drugs and measuring the results and studying signal transduction in highly specialized cells. She was the co–author of multiple published papers related to the research she and the scientists she worked for performed.

In 2008, the taxpayer married an American citizen, and they continued to reside in South Carolina until the petition was filed in 2014. She had twins in 2012 and became a permanent resident of the United States in October 2012. Her employment with MUSC terminated in December 2012.

The taxpayer filed a Form 1040–NR–EZ, U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents, for tax years 2010 and 2011. She indicated that she was single when in fact she was married. She was a resident alien during both of those years, even though she filed a nonresident alien tax return. She reported her tax home as Russia and excluded all of her MUSC income as exempt from taxation under the Russia–U.S. treaty.

The Tax Court concluded that the taxpayer’s income from MUSC was taxable in the United States. The taxpayer admitted she was a resident alien and that the Code imposes “an income tax on the income of every individual who is a citizen or resident of the United States,”8 including resident aliens. The Russia–U.S. treaty permits the host country to tax “salaries, wages, and other similar remuneration derived … in respect of an employment.”9

The court looked to Baturin10 to inform the meaning of “grant, allowance, or other similar payments” as also found in the treaty. Baturin considered certain facts to indicate whether a taxable salary or a nontaxable grant existed, including whether the project could be performed by another individual, whether the lab retained the rights to the individual’s work, whether the project pre– or post–dated the work done in that lab, whether the individual had discretion in their day–to–day work, and whether there was a quid pro quo. Since the taxpayer could have been replaced in her work, did not have rights to her work, worked on projects that pre– and post–dated her work in the lab, did not have overall discretion in her day–to–day work, and did receive a quid pro quo, the Tax Court held that she received a salary instead of a grant.

Sec. 164: Taxes

In Besaw,11 the taxpayer, John Henry Besaw, represented himself in Tax Court. His case was heard by the court pursuant to the small–claims provisions of Sec. 7463.

Four issues surrounded Besaw’s 2020 tax return: whether (1) he was entitled to deduct an amount for SALT greater than what the IRS determined; (2) he was entitled to deduct gambling losses; (3) he proved that the amount of gambling winnings reported on his joint federal return should be reduced; and (4) he was liable for accuracy–related penalties.

With regard to SALT, Besaw claimed real estate taxes, local personal property taxes, and state and local general sales taxes. These figures exceeded the SALT cap of $10,000, so the cap amount was reported. Sec. 164 provides specific rules for deducting state and local real property taxes and personal property taxes and also provides for a deduction for state and local income taxes but says that a taxpayer may instead elect to deduct state and local sales taxes. To deduct the actual amount of sales taxes paid, substantiation is required, or the Code permits taxpayers to calculate the amount by using IRS guidelines. Besaw requested the court to determine the state and local sales tax deduction, and the court found the deduction to be lower than what Besaw reported, thus reducing the claimed SALT deduction.

With respect to gambling losses and winnings, usually, a taxpayer seeks to show that gambling losses equal or exceed gambling winnings. In his brief, Besaw did not dispute the amount of gambling losses that the IRS allowed in the notice of deficiency, even though the amount was less than that reported on the tax return. At trial, though, Besaw argued that his total gambling winnings were less than what he reported on his 2020 joint tax return and less than the amount of allowable gambling losses.

Unfortunately for Besaw, the documents to support this claim were not admitted into evidence, and further, as the Tax Court noted, they appeared to be from his spouse, who was neither a party to this case nor called as a witness by Besaw. Besaw testified that he “didn’t know exactly how much my wife lost or won, so I was trying to be careful” and went with an estimated figure of $30,000. Documents admitted into evidence included win–loss statements from casinos that did not present a clear picture of gambling winnings during the year, and IRS information returns, such as Form W–2G, Certain Gambling Winnings, were not reported. Further, neither Besaw nor his wife provided testimony with a diary or other verifiable documentation as to the winnings.

The Tax Court found that Besaw’s testimony was not credible and he had not met his burden of proving that the IRS’s determination in the notice of deficiency was incorrect. Because he had not provided a reasonable basis to estimate gambling winnings in 2020, he did not meet his burden of proving that the amount of gambling income should be reduced to less than what he reported on his tax return.

With regard to whether Besaw was subject to a Sec. 6662(a) accuracy–related penalty, the Tax Court also concluded that Besaw did not have reasonable cause and did not act in good faith in underpaying his 2020 income tax, so he was subject to the penalty. In making the reasonable–cause determination, the court found that the most important factor is usually the extent of the taxpayer’s effort to assess his or her proper tax liability. Although the court appreciated Besaw’s preparing his own return and that the Code is complex, it stated that Besaw seemed “to have simply guessed at the amount of gambling winnings and losses.” And with respect to his state and local taxes, Besaw failed to keep receipts or other proof to substantiate his claimed deduction. Therefore, the court determined that Besaw failed to maintain adequate records to calculate his tax liabilities and thus did not act with the reasonable cause and good faith necessary to avoid the Sec. 6662(a) accuracy–related penalty.

Sec. 166: Bad debts

Two recent cases have involved bad debts. In Anaheim Arena Management, LLC,12 Anaheim Arena Management (AAM) managed a sports and entertainment arena in Anaheim, Calif. During the course of managing the facility, AAM would advance deposits and other funds in connection with the operation and management of the facility, with interest accruing annually. Over the tenure of the contract, AAM advanced more than $50 million in principal and $1 million in interest, totaling nearly $51.5 million. The primary matter being litigated was whether funds advanced by AAM were considered debt and subject to a bad–debt deduction.

Sec. 166(a)(1) allows a deduction against ordinary income for debt that becomes worthless within the tax year. A bona fide debt is a debt that arises from a debtor–creditor relationship based upon a valid and enforceable obligation to pay a fixed or determinable sum of money. In the Ninth Circuit, to which an appeal of the case would lie, 11 factors are considered to determine whether there is a debt for federal income tax purposes.13 The court found that in AAM’s case, none of the factors indicated the advances constituted debt and therefore sustained the IRS’s disallowance of AAM’s bad–debt deduction.

In another recent case, Kelly,14 Michael Kelly appealed a Tax Court ruling related to cancellation–of–debt and nonbusiness bad–debt write–offs. Kelly had transferred funds between his business entities and characterized them as loans. On Dec. 31, 2010, Kelly canceled many of these loans. He reported them on his 2010 tax return as cancellation of debt but excluded them from income due to his personal insolvency. He also reported a short–term capital loss due to a nonbusiness bad–debt write–off, claiming the discharge of the debt automatically or presumptively rendered it worthless.

To claim a nonbusiness bad–debt deduction under Sec. 166, a taxpayer must establish that the debt is bona fide, the taxpayer has adjusted tax basis sufficient to claim the deduction, and that the debt became wholly worthless within the tax year. Kelly argued that a discharged debt under Sec. 61(a)(11) is the same as a worthless debt under Sec. 166. However, according to the Ninth Circuit, “worthless” and “discharged” are not synonymous. Rather, “worthless” is defined as “lacking value or utility,” and “discharged” is defined as “released from repayment.”

Although a debt obligation might lack value at the time of discharge, the Ninth Circuit explained, determining lack of value requires examining the objective facts and stated that debt discharge does not, as a matter of law, eliminate the debt’s prior objective value and render it worthless. Kelly was not able to show that his debt was wholly worthless, so the Ninth Circuit held, affirming the Tax Court, that the debt was not worthless and that Kelly was not entitled to a bad–debt deduction for it.

Footnotes

1See Nance, “QSBS Gets a Makeover: What Tax Pros Need to Know About Sec. 1202’s New Look,” 56-11 The Tax Adviser 16 (November 2025).

2Sec. 1245(a)(3)(G).

3Muse, No. 15191-24S (Tax Ct. 6/12/25) (bench op.).

4Fortune-Paladino, T.C. Memo. 2025-101.

5Mennemeyer, T.C. Memo. 2025-80.

6Feige, T.C. Memo. 2025-88.

7Kramarenko, T.C. Memo. 2025-61.

8Regs. Sec. 1.1-1(a).

9Convention for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion With Respect to Taxes on Income and Capital, Russia–United States, June 17, 1992, Article 14(1).

10Baturin, 31 F.4th 170 (4th Cir. 2022).

11Besaw, T.C. Summ. 2025-8.

12Anaheim Arena Management, LLC, T.C. Memo. 2025-68.

13See A.R. Lantz Co., 424 F.2d 1330, 1333 (9th Cir. 1970).

14Kelly, 139 F.4th 854 (9th Cir. 2025), aff’g T.C. Memo. 2021-76.

Contributors

Karmen Hoxie, CPA, is a solo practitioner in the Minneapolis area. Amie Kuntz, CPA, is a partner in the national tax group of RubinBrown LLP. Stephen Mankowski, CPA, CGMA, is owner and founder of Mankowski Associates CPA, LLC, in Hatboro, Pa. Dana McCartney, CPA, is a partner with Maxwell Locke & Ritter LLP in Austin, Texas. Matthew Mullaney, CPA, is a managing director, Private National Tax, with PwC US Tax LLP in Florham Park, N.J. Patrick Sanford, CPA, is president of Probity Accounting PLLC in Van Buren, Ark. Kuntz is the chair, and the other authors are members, of the AICPA Individual and Self-Employed Tax Technical Resource Panel. For more information about this article, contact thetaxadviser@aicpa.org.

MEMBER RESOURCES

CPE self-study

Individual Tax Fundamentals — Tax Staff Essentials

Tax Staff Essentials — Individual Taxation Bundle

Tax Section resources

Individual Income Taxation library

For more information or to make a purchase, visit aicpa-cima.com/cpe-learning or call 888-777-7077.