Dissolving business taxpayers: Selected procedural implications

Editor: Alexander J. Brosseau, CPA

Dissolving a business does not always end the business’s involvement with the IRS. This item discusses common procedural tax issues related to state–law dissolutions, including final returns and IRS audits.

Note: This item focuses on procedural issues for state–law dissolutions; it does not address check–the–box liquidations, F reorganizations, and acquisitive reorganizations; it does not address qualification issues such as those under Sec. 332 or Sec. 331; and it does not address the numerous substantive issues involved in dissolving an entity (e.g., recapture, treatment of goodwill, gain or loss on distribution of assets); employment tax implications; or state tax issues. Additionally, this item does not address the legal question of when a taxpayer is considered to have dissolved.

Final returns

All dissolving entities must file a final return with the IRS, which sounds simple, but taxpayers should remember that the due date of final returns is based on the date of dissolution (not the full tax year). Additionally, while checking the “final return” box on the relevant return form is straightforward, there can be issues with determining or reporting the final year (e.g., the taxpayer forgets to mark the box, the taxpayer did not know it was the final year, or the supposed final year turns out not to be the actual final year). In addition, there can be IRS processing errors (e.g., the Service mistakenly applies overpayments to the December year end instead of the short period).

Marking the return final

When a taxpayer files its final return, it should select the “final return” box on the form. When a taxpayer marks a return final, the IRS will update its system to reflect that the taxpayer will not be filing future returns. If the taxpayer does not mark the return final, the IRS will assume the taxpayer will file a return for the next year, and it may send a notice the following year alerting the taxpayer that it failed to file a tax return.

If a taxpayer inadvertently failed to check the “final return” box, it could attempt to contact the IRS to have the account marked “final” or file an amended return to check the “final” box.

If a taxpayer accidentally marked a return “final,” it will need to call the IRS to have the account “turned back on” so the IRS system will allow the taxpayer to electronically file.

Final return due dates

Corporations must file their final income tax return (or request an extension) by the 15th day of the fourth month after the date the corporation ceases business and dissolves, which marks the end of the corporation’s tax year that otherwise occurs at the normal close of its tax year (Regs. Secs. 1.6072–2(a)(1)(i) and (a)(2)). The IRS considers a corporation dissolved for federal tax purposes even if state law treats it as continuing for certain limited purposes connected with winding up its affairs (Regs. Sec. 1.6012–2(a)(2)). If a corporation was in existence for any part of the year, it must file a return for the fractional part of the year during which it was in existence (id.).

Example: ABC Corp., a calendar–year taxpayer, ceases operations on Jan. 4, 2026. It must file a tax return for the period Jan. 1 to Jan. 4, 2026. The return is due May 15, 2026 (or Nov. 15, if ABC Corp. timely requests an extension).

Partnerships must file their final tax return (or request an extension) by the 15th day of the third month after the partnership terminates (Sec. 6072(b); Internal Revenue Manual (IRM) §3.14.2.6.10.2(5)). A partnership terminates when the operations of the partnership are discontinued and no part of any business, financial operation, or venture of the partnership continues to be carried on by any of its partners in a partnership (Sec. 708(b)(1); Regs. Sec. 1.708–1(b)(1)).

S corporations must file their final tax return (or request an extension) by the 15th day of the third month after the S corporation terminates (Regs. Sec. 1.6072–2(a)(1)(ii)). Like C corporations, an S corporation terminates when it ceases business, dissolves, and does not retain any assets (see Regs. Sec. 1.6012–2(a)(2)).

Form 966, Corporate Dissolution or Liquidation

A taxpayer must file Form 966, Corporate Dissolution or Liquidation, within 30 days of adopting a resolution or plan for dissolution or for liquidation of capital stock (Sec. 6043(a)(1)). The due date is triggered by the adoption of the plan, not the date of dissolution. If, after filing Form 966, the taxpayer amends or supplements the plan, it must file another Form 966 within 30 days of adopting the amendment or supplement (Regs. Sec. 1.6043–1(a)). However, taxpayers do not need to file a new Form 966 if the liquidation did not conclude by the stated date (as long as there has been no actual change or amendment to the plan of liquidation).

Although the Internal Revenue Code requires taxpayers to file Form 966, there is no express penalty for failure to file Form 966. Moreover, failure to file the form does not prevent liquidation treatment (Rev. Rul. 65–80; Rendina, T.C. Memo. 1996–392 (“the filing of Form 966 is not a condition of liquidation treatment under any provision of the Internal Revenue Code”)). If a taxpayer fails to timely file Form 966, it should file the form as soon as possible.

Closing a business account

Before closing an account, the taxpayer should request account transcripts to confirm that there are not any outstanding issues with the IRS (e.g., no balances due or refunds owed).

The IRS advises taxpayers to close their employer identification number (EIN) and business account (see IRS webpage, “Closing a Business“). Per IRS instructions, the taxpayer should send a letter to the IRS with the business’s name, EIN, and address. In addition, the letter should state the reason the taxpayer wishes to close the account. The taxpayer should attach a copy of the notice assigning the taxpayer’s EIN. The IRS will not close the account until the taxpayer has filed all returns and paid all taxes.

Audits of dissolved entities

Audits of dissolved entities are generally the same as audits of ongoing entities but with two additional considerations: (1) who can act on behalf of the entity and (2) how the IRS collects any additional tax owed.

Generally, the IRS has three years to audit the tax return of a dissolved taxpayer. (As with all taxpayers, exceptions may apply to extend the IRS’s assessment statute of limitation.) It is irrelevant whether the corporation dissolved under state law; state law cannot shorten the federal statute of limitation (IRM §4.10.13.3.3.3(2)).

Conducting the audit

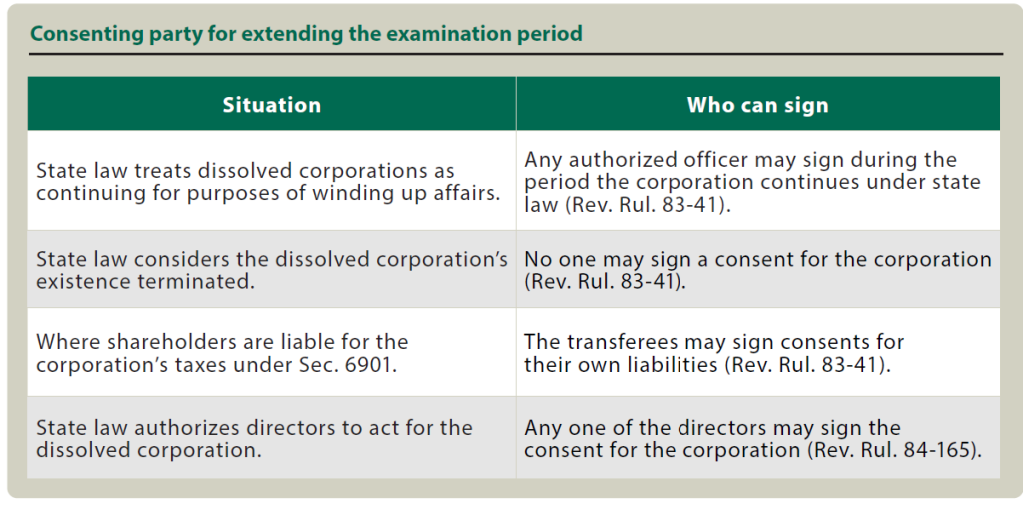

Although state law does not control the IRS’s ability to audit an entity, it does control who can act on behalf of a dissolved entity during the audit and for how long. Some states will provide the entity a windup period or provide which individuals are authorized to act for a dissolved corporation (IRM §4.10.13.3.3.3(3)). The state–law procedures may terminate the rights of others previously authorized to act on behalf of the company (i.e., officers before dissolution) (id.). State law may limit the time individuals are authorized to act on behalf of a dissolved entity (id.). The relevant state law is the law of the state of incorporation (not the principal place of business) (IRM §4.10.13.3.3.3(5)).

A key consideration for the IRS will be securing consent to extend the statute of limitation from the proper person. The IRS has guidance on who can sign the consent for the situations in the table “Consenting Party for Extending the Examination Period,” below.

Collecting additional tax

Similar to who can act on behalf of a dissolved entity, it can be a complicated legal question to determine whom the IRS can assess any additional tax owed. Below is a high–level description of factors the IRS may apply when looking to collect tax owed by a dissolved entity.

A preliminary question is whether there is a successor or a transferee to the dissolved entity. If there is a successor under state law, the successor is generally primarily liable for the merged entity’s debts by operation of state law (Chief Counsel Advice (CCA) 201136020 (“A successor corporation to a merger is not a transferee; rather it assumes primary liability for the debts of the merged corporation as a successor to the merged corporation by operation of law.”)).

If a dissolved entity does not have any assets from which the IRS can collect and does not have a successor, the IRS may invoke transferee liability provisions in Sec. 6901 (IRM §4.10.13.3.3.3(1)). Generally, Sec. 6901 applies only to income, estate, and gift taxes, but it can apply to other taxes if there is a liquidation of a corporation or partnership or upon the reorganization of a corporation pursuant to Sec. 368(a) (Sec. 6901(a)(2)). If the IRS determines it will need to collect from a transferee, it will develop a concurrent examination against the transferee (IRM §4.10.13.3.3.3(1)). The IRS has additional time to assess any tax against a transferee — it has one year after the expiration of the transferor’s assessment statute of limitation (Sec. 6901(c)). The extended statute of limitation applies only if transferee liability applies; if a taxpayer is primarily liable for the debt under state law (e.g., a successor corporation to a merger), the IRS does not have an additional year to collect (CCA 201136020 (stating that Sec. 6901(c)’s extended statute of limitation does not apply when there is an entity with primary liability for the additional tax)).

BBA: Cease-to-exist partnerships

For partnerships subject to the Bipartisan Budget Act (BBA), P.L. 114–74, and their partners, there are special rules if the partnership ceases to exist when the IRS finishes its exam. (These rules are nuanced and complicated; therefore, this item provides only a high–level overview.)

Normally, at the end of a BBA audit, the partnership is liable for the imputed underpayment resulting from partnership adjustments unless it elects to push out the adjustments to its partners (Sec. 6225). However, if a BBA partnership ceases to exist before the IRS makes a partnership adjustment, the partnership is no longer liable for the imputed underpayment (Regs. Sec. 301.6241–3(a)(2)). Instead, the adjustments are taken into account by the former partners (Regs. Sec. 301.6241–3(a)(1)). Former partners are the partnership’s partners during the year in which the IRS adjustment is final (i.e., “adjustment year”) (Regs. Sec. 301.6241–3(d)(1)(i)). If there are no partners during the adjustment year, the partners during the last tax year for which the partnership return was filed are “former partners” for purposes of the IRS’s collecting additional tax owed by the ceased–to–exist partnership (Regs. Sec. 301.6241–3(d)(2)).

The rules apply only if the partnership “ceases to exist” (Regs. Sec. 301.6241–3(b)(3)). Under the regulations, a partnership does not cease to exist if the partnership representative or designated individual (1) timely elects to push out adjustments under Sec. 6226 or (2) pays the imputed underpayment within 10 days of the IRS’s notice and demand for payment (id.).

Procedural and legal concerns

In summary, when taxpayers are dissolving entities, they should consider the procedural implications as well as the substantive legal considerations. Specifically, taxpayers should consider the due date of final returns, closing their accounts with the IRS, and who will act on behalf of the entity if it is selected for audit post–dissolution. To the extent possible, taxpayers should attempt to resolve any procedural issues, receive all refunds, and pay additional tax before dissolution.

Editor

Alexander J. Brosseau, CPA, is a senior manager in the Tax Policy Group of Deloitte Tax LLP’s Washington National Tax office.

For more information about these items, contact Brosseau at abrosseau@deloitte.com.

Contributors are members of or associated with Deloitte Tax LLP.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.