Navigating the Form 1099-DA reporting maze

In 2021, Congress enacted the Infrastructure Investment and Jobs Act (IIJA), P.L. 117-58, which requires brokers to report digital asset transactions to the IRS and taxpayers. In enacting the IIJA, Congress intended to deter underreporting of digital asset transactions and their contribution to the tax gap.

What is the default reporting requirement for digital asset transactions?

In 2024, Treasury and the IRS finalized regulations (T.D. 10000) requiring custodial brokers to report customers’ digital asset sales and exchange transactions via Form 1099-DA, Digital Asset Proceeds From Broker Transactions. Custodial brokers are brokers that take possession of customers’ digital assets. Custodial brokers include centralized cryptocurrency exchanges and digital asset payment processors (PDAPs). As of September 2025, over 80% of digital assets’ trade volume arose from custodial exchanges (theblock.com). Therefore, the regulations are designed to capture most domestic digital asset transactions, but some transactions still may not trigger a Form 1099-DA filing requirement.

What digital asset transactions might not be reported?

Noncustodial brokers (e.g., decentralized exchanges and unhosted wallet providers) are outside the scope of these regulations. The following transactions identified in IRS Notice 2024-57 are also deferred from the scope of the regulations until studied further by Treasury and the IRS:

- Wrapping and unwrapping transactions;

- Liquidity provider transactions;

- Staking transactions;

- Transactions involving lending of digital assets;

- Transactions involving short sales of digital assets; and

- Notional principal contract transactions.

Note that these transaction types are only deferred from the scope of the Form 1099-DA sale and exchange reporting until further notice but may otherwise be in scope of other Form 1099 reporting requirements, such as interest in lending on Form 1099-INT, Interest Income, or staking rewards on Form 1099-MISC, Miscellaneous Information.

Additionally, the regulations exempt certain types of transactions from the reporting requirements, namely (1) the exchange of qualifying stablecoins for other digital assets, (2) tokenized securities that represent interests in money market funds, and (3) digital assets sold to pay transaction costs or backup withholding taxes but only when paid from the acquired asset in a crypto-for-crypto exchange. Finally, the regulations provide the following annual de minimis thresholds for reporting sales or exchanges of certain types of digital assets:

- Qualifying stablecoins sold for cash or other qualifying stablecoins: $10,000 (Regs. Sec. 1.6054-1(d)(10)(i)(B));

- Specified nonfungible tokens (NFTs): $600; and

- PDAP sales: $600 (Regs. Sec. 1.6045-1(d)(2)(i)(C)).

Although certain transactions may be excepted from Form 1099-DA reporting, they may still be important for reconciling the taxpayer’s cost basis and proceeds.

Form 1099-DA reporting basics

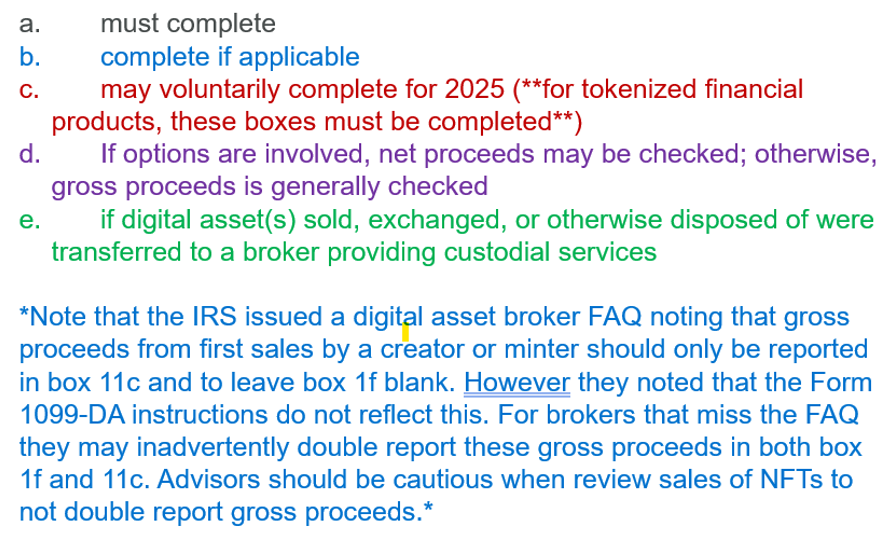

What’s on Form 1099-DA?

The following copy of Form 1099-DA illustrates the information that is required to be reported for sales or exchanges of digital assets, if applicable, and that which may voluntarily be reported for 2025 transactions.

Note that the IRS issued digital asset broker frequently asked questions noting that gross proceeds from first sales by a creator or minter should be reported only in box 11c and to leave box 1f blank. However, the Service noted that the form 1099-DA instructions do not reflect this. Brokers unaware of the FAQs may inadvertently double-report these gross proceeds in both boxes 1f and 11c. Advisers should be cautious when reviewing sales of NFTs to not double-report gross proceeds.

What to expect from brokers furnishing Forms 1099-DA

Brokers are not required to report cost basis information (acquired value and acquisition date) on Forms 1099-DA for digital asset sale transactions in 2025. Although they will begin reporting cost basis information on Forms 1099-DA for 2026 transactions, they might not furnish Forms 1099-DA or complete ones in many instances:

- Taxpayers might not receive a Form 1099-DA for the following transactions:

- Sales on non-U.S. exchanges (pending further coordination with the Organisation for Economic Co-operation and Development’s Crypto-Asset Reporting Framework (CARF)) — it is possible that non-U.S. exchanges may furnish information reporting in the future only if they are subject to Form 1099-DA requirements; otherwise, taxpayers will not receive a Form 1099-DA for transactions that are reportable by non-U.S. exchanges that are instead subject to CARF reporting.Decentralized finance (DeFi) transactions when there is no controlling third-party intermediary effectuating the sale or exchange.Sales of qualifying stablecoins and specified NFTs below de minimis reporting thresholds.Sales exempted from reporting, such as sales of qualifying stablecoins for other digital assets (e.g., USD Coin (USDC) sold to buy Ethereum (ETH)).Sales or exchange transactions deferred from reporting under IRS Notice 2024-57 (e.g., lending, liquidity pools, wrapping/unwrapping transactions, etc.).Transfers where there is no intermediary facilitation (e.g., where a customer directly transfers a digital asset to a retailer who does not use a third-party payment processor or other digital asset broker for the transfer; see Regs. Sec. 1.6045-1(b)(12), Examples (12) and (13)).

- Transactions that are not sales or exchanges of a digital asset, though such transactions may be reportable on other Forms 1099 (e.g., airdrops, staking rewards, or interest from lending transactions).

- A taxpayer may receive a Form 1099-DA but without cost basis information for the following transactions:

- Sales of assets that were transferred in (from another broker or self-custody wallet);

- Sales on noncustodial platforms that may touch the crypto but not hold it;

- Sales of assets purchased before 2026 (not covered securities);

- Sales of most crypto exchange-traded funds (ETFs) that are structured as grantor trusts (as trusts are not covered securities); and

- Sales of qualifying stablecoins and specified NFTs that are reported in aggregate.

Additionally, taxpayers may receive aggregated Forms 1099-DA for reporting specified NFTs and qualifying stablecoins, but note that they may still be required to report such transactions as separate transactions on Form 8949, Sales and Other Dispositions of Capital Assets.

What are some common misconceptions about Form 1099-DA reporting?

- Myth: Digital asset reporting was tabled by the administration.

Centralized (custodial) broker reporting remains intact and effective. However, Congress enacted House Joint Resolution 25 to remove the decentralized broker reporting regulations.

- Myth: Digital asset transactions have no tax consequences if no Form 1099-DA is issued.

Taxpayers are required to report items of income, gain, and loss on their digital asset transactions that trigger a realization event regardless of whether they receive a Form 1099-DA and whether a broker has custody of the digital assets. Likewise, taxpayers should maintain records to substantiate their tax returns.

- Myth: Digital asset transactions under the de minimis reporting thresholds do not trigger items of income, gain, or loss.

The de minimis reporting thresholds apply to the broker for determining when to furnish tax information reports. Digital assets are treated as property for federal income tax purposes under IRS Notice 2014-21, so items of income, gain, and loss may still trigger a realization event and should be considered on a transaction-by-transaction basis.

- Myth: Staking rewards are tax-free because the taxpayer did not sell them or because they were not reported on Form 1099-DA.

Rev. Rul. 2023-14 provides guidance that staking rewards are ordinary income upon receipt of the rewards to the extent the taxpayer has dominion and control, regardless of whether the taxpayer received a Form 1099. As a staking reward is income and not a sale or exchange of a digital asset reportable on Form 1099-DA, it may be reportable by certain payers on Form 1099-MISC, or other form, where the payer has control of the payment (e.g., centralized exchanges).

Keeping tabs on your tokens: Basis tracking

What cost basis tracking methods are acceptable?

The regulations instructed brokers to apply first-in, first-out (FIFO) as the default for tracking cost basis in digital assets (Regs. Sec. 1.1012-1(j)(3)). The regulations allow taxpayers to use specific identification or standing orders. Other acceptable methods for native crypto tokens include highest-in, first-out (HIFO) and last-in, first-out (LIFO). Regs. Secs. 1.1012-1(j)(3)(ii) and 1.6045-1(d)(2)(ii)(B)(2) provide that taxpayers can adopt a standing order to track lots in a manner that is consistent with the broker’s tracking requirements. This could be an attractive option for taxpayers seeking simplification rather than reconciling lot identification inconsistencies. Average cost is available only for tokenized mutual funds and tokenized ETFs but not for native crypto such as bitcoin.

To use specific identification, taxpayers must identify the specific lots prior to the sale. If digital assets are in the broker’s custody, taxpayers must notify the broker of the specific identification method prior to the sale. Regardless of whether the digital assets are in the broker’s custody or a noncustodial wallet, maintaining appropriate books and records is critical to substantiating the specific-identification method.

Because not all brokers have systems in place to accept taxpayer-designated specific identification or standing orders, the IRS issued Notice 2025-7, which afforded transition relief allowing taxpayers with custodial accounts to adequately identify digital assets in their personal books and records rather than with the custodial broker; however, such relief was effective only from Jan. 1, 2025, until Dec. 31, 2025.

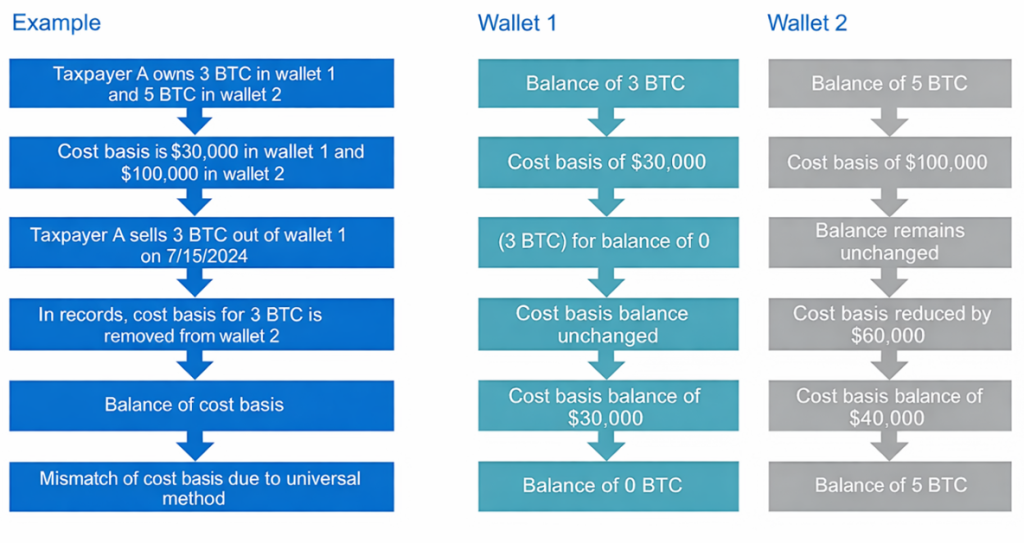

What about taxpayers who used the universal method to relieve lots across all wallets and exchanges?

The IRS issued Rev. Proc. 2024-28 to provide transition relief for taxpayers who in a previous tax year used the universal method of relieving cost basis upon sale or disposition. Under the universal method, taxpayers specifically identified the digital assets sold across all accounts, which may have resulted in a digital asset with used basis and an “orphaned” basis with no digital asset. Rev. Proc. 2024-28 provided a safe harbor allowing taxpayers to make a reasonable allocation of units of unused basis to an account, provided that the account held the same number of remaining digital assets and the unused basis units were the same type of digital asset as the remaining digital assets.

Generally, taxpayers who did not satisfy the safe harbor by Jan. 1, 2025, became ineligible for penalty relief for prior periods in which they had used the universal method. However, taxpayers are still required to transition away from the universal method to a wallet-by-wallet method to better capture that their digital assets have basis allocated to them. In Fahrer and Hauffe, “Universal Accounting for Digital Assets Concludes, but Safe Harbor Available,” The Tax Adviser (Oct. 29, 2024), we outlined various methods to satisfy the safe harbor. If a client used the universal method and missed the safe-harbor deadline, advisers should inform them of the requirement to make a reasonable allocation of digital assets. Although the consequences of missing the safe harbor are unclear, it is possible that failure to satisfy the safe-harbor requirements would allow the IRS to redetermine a taxpayer’s basis in digital assets in prior periods, resulting in unexpected tax liabilities, penalties, and interest.

What are suggested cost basis tracking and recordkeeping practices?

- Completeness and accuracy of wallets and accounts:

- Upon movement and transfer of digital assets across multiple wallets, associated cost basis moves with the asset from one wallet to the next. Thus, a list of wallets or accounts solely showing where the asset was liquidated is likely not enough for determining cost basis.

- Consider signing up for third-party crypto tax and accounting aggregator software that can automate much of the time-consuming tasks of cost basis tracking.

- Not all crypto tax and accounting software has the same level of quality or supports all of the types of transactions (e.g., DeFi, NFTs, and trade or business accounting vs. individual consumers). Also, consider whether the crypto tax and accounting software has controls in place to protect customer data, such as an independent System and Organization Controls 2 (SOC 2) report.

- Consider remaining consistent across tax years in determining how items of income, gain, or loss are treated.

- For example, treating staking rewards as income upon receipt in tax year 1 but not income upon receipt in tax year 2 may rise to the level of a nonautomatic accounting method change.

Charting the practitioner’s path through compliance corridors

How do I begin collecting digital asset information from clients?

The first step is asking clients the digital asset question found on most income tax returns. Although some tax preparation software may default the answer to “no,” practitioners should include this question in their client intake forms or annual client questionnaires.

Second, if clients responded “No” to the digital asset question in prior years but responded “Yes” in the current tax year, question whether the taxpayer may have unreported digital asset transactions in prior years.

Third, if clients have digital asset transactions for the 2025 tax year, begin requesting records, such as Forms 1099-DA or personal records substantiating cost basis, acquisition date, and any other applicable information, whether via personal records or digital asset tracking software.

Last, as this is not covered in the digital asset question found on most income tax returns, ask the client whether they acquired any spot crypto ETFs during the current or prior periods. These were launched in 2024, and most are nondistributing grantor trusts that will not report the underlying gain/loss activity of the fund on a Form 1099-B, Proceeds From Broker and Barter Exchange Transactions. You and your client will need to download tax information reports from the issuer’s website to properly account for the taxpayer’s allocable share of underlying fund sales of crypto. Starting in 2025, certain spot crypto ETFs that earn staking rewards may issue Forms 1099-B in certain cases for the underlying fund activity. This reporting will be on either an accrual-like basis (as earned by the fund) or on a cash-like basis (as distributed to the taxpayer). In the future, some of this Form 1099-B reporting may transition to Form 1099-DA reporting.

What are some of the most significant compliance challenges for the current filing season?

- Broker transition relief: The IRS has granted transition relief to brokers, which means that certain brokers may issue Forms 1099-DA up to one year late (i.e., February 2027). If a digital asset transaction was not accounted for on the client’s 2025 tax return and the client receives a Form 1099-DA for a 2025 transaction in 2027, the client may need to file an amended return to reconcile discrepancies in reporting. However, as mentioned before, receipt of a Form 1099-DA is not the triggering event for including an item of income, gain, or loss on a taxpayer’s tax return. If the transaction in question triggered an item of income, gain, or loss, it should likely be reported anyway.

- Reconciling mismatching basis: Although most brokers will not be reporting cost basis on Forms 1099-DA for the 2025 tax year, clients may receive Forms 1099-DA with cost basis information that does not match their records. Practitioners may need to reconcile the difference, determine the appropriate amounts on Form 8949, and add a note explaining the reconciliation.

- For example, some brokers may take the approach of providing a Form 1099-DA to the IRS without cost basis while also providing their customers with a summarized Form 1099-DA report for ease of filing information on the customer’s tax return.

- Transitioning from the universal method: For taxpayers transitioning from the universal method as discussed above, practitioners may need to inform their clients of the steps needed to comply with the transition, even if the client missed the safe-harbor deadline for prior-period penalty relief.

Where is cost basis information reported on a taxpayer’s tax return?

Form 8949 is used to report many digital asset transactions, including cost basis and acquisition date information, regardless of whether a Form 1099-DA is furnished by a broker to the taxpayer.

Are there any foreign reporting requirements for individuals holding digital assets?

Although the application of digital assets to foreign information-reporting requirements (i.e., Form 8938, Statement of Specified Foreign Financial Assets, and Financial Crimes Enforcement Network (FinCEN) Form 114, Report of Foreign Bank and Financial Accounts (FBAR)) remains unclear, FinCEN has noted in Notice 2020-2 that accounts holding foreign financial assets exceeding the reporting thresholds and digital assets would be reportable only from the perspective of nondigital assets exceeding the reporting thresholds.

AICPA advocacy and resources

- AICPA homepage for digital assets tax guidance and resources

- Advocacy, resources, podcasts, and more

- AICPA Digital Asset Tax Framework

- Questionnaire for Individual Clients — Digital Asset Activities

- AICPA homepage for digital assets and blockchain resources

— Nik Fahrer, CPA, is director and blockchain and digital assets practice leader with Forvis Mazars US in Colorado Springs, Colo. Jessalyn Dean, CPA, is a subject matter expert in tax information reporting and managing director of Dune Consultants. Daniel A. Hauffe, J.D., is senior manager–AICPA Tax Policy & Advocacy. Fahrer and Dean are members of, and Hauffe is staff liaison to, the AICPA Digital Assets Task Force. To comment on this article or to suggest an idea for another article, contact Paul Bonner at Paul.Bonner@aicpa-cima.com.