New IRS rules for digital content and cloud transactions

Editor: Jeffrey N. Bilsky, CPA

On Jan. 10, 2025, Treasury and the IRS released final regulations (T.D. 10022) addressing the classification of digital content and cloud transactions. Proposed regulations (REG–107420–24) were issued concurrently for determining the source of income derived from cloud transactions.

Broadly speaking, “digital content” means a computer program or other content, such as movies and music, in digital format. “Cloud transactions” refers to obtaining on–demand network access to computer hardware, digital content, or other similar resources. The new rules generally affect businesses that offer digital content or cloud transactions to customers.

The final cloud transactions regulations include several notable revisions to the proposed regulations released in August 2019, while the final regulations on digital content introduce a number of clarifications to existing regulations. Both the digital content and cloud transactions final regulations include examples applying the rules to resellers of digital content and cloud transactions.

The final regulations generally apply to tax years beginning on or after Jan. 14, 2025, although taxpayers may apply them to tax years beginning on or after Aug. 14, 2019, and all subsequent tax years, provided certain conditions are met.

This item provides a brief overview of the final and proposed regulations and focuses on their implications for businesses with reseller models.

Final digital content regulations

The final digital content regulations include several new definitions and rules, including the following:

- The scope of existing Regs. Sec. 1.861-18 is expanded to cover transactions involving “digital content,” whereas those regulations previously covered “computer programs.” “Digital content” is defined specifically as “a computer program or any other content, such as books, movies, and music, in digital format that is (A) protected by copyright law or (B) not protected by copyright law solely (1) due to the passage of time; or (2) because the creator dedicated the content to the public domain” (Regs. Sec. 1.861-18(a)(2)(i)).

- For transactions with multiple elements (including de minimis elements), the final digital content regulations replace the de minimis rule previously found in Regs. Sec. 1.861-18(b)(2) with a “predominant character” rule, which requires characterization based on the transaction’s predominant character. Such a determination is based on the transaction’s facts and circumstances and is generally based on the primary benefit or value the customer receives.

- Similar to how prior regulations categorized “computer programs,” Regs. Sec. 1.861-18 classifies digital content transactions into four categories:

- A transfer of a copyright in the digital content;

- A transfer of a copy of the digital content (a copyrighted article);

- The provision of services for the development or modification of the digital content; or

- The provision of know-how relating to the development of digital content (Regs. Sec. 1.861-18(b)(1)).

- The final digital content regulations also provide a new sourcing rule for sales of copyrighted articles that are sold and transferred through an electronic medium. Regs. Sec. 1.861-18(f)(2)(ii) provides that such sales are sourced to the customer’s billing address, unlike prior proposed regulations that would have sourced such transactions based on the location of download or installation onto the end user’s device used to access the digital content.

Final cloud regulations

The final cloud regulations, like the previously proposed regulations, apply to “cloud transactions,” broadly defined as transactions through which a person obtains on–demand network access to computer hardware, digital content (applying the same definition discussed above), or other similar resources.

Similar to the final digital content regulations, the final cloud regulations introduce a predominant–character rule for purposes of classifying a transaction with multiple elements. Further, and most notably, all cloud transactions are treated solely as the provision of services, replacing the previously proposed regulations’ requirement that taxpayers make a determination as to whether a cloud transaction should be characterized as the provision of services or a lease of property.

The final cloud regulations also include additional and updated examples for different types of business models, including resellers.

Proposed cloud sourcing regulations

The proposed cloud sourcing regulations issued alongside the final regulations introduce new rules on how to source gross income from cloud transactions. The previously proposed cloud regulations were silent on this topic.

More specifically, the proposed cloud sourcing regulations adopt a formulary approach to determine the source of income from cloud transactions, considering the location of intangible assets, employee functions, and tangible property involved. Each of these three factors is based on worldwide expenses that reflect the contributions of relevant personnel and assets. The U.S.-source portion of gross income from cloud transactions is calculated by multiplying total gross income from cloud transactions by a fraction, the numerator of which is the sum of U.S.-source amounts for each factor and the denominator of which is the sum of all three factors. The residual balance represents the foreign–source portion of gross income from cloud transactions. Further details of these three factors are provided below.

Intangible–property factor: The intangible–property factor measures the contribution of intangible assets to cloud transactions. It consists of the taxpayer’s specified research and experimental (R&E) expenditures under Sec. 174(b) (before amendment by the law known as the One Big Beautiful Bill Act, H.R. 1, P.L. 119–21) associated with cloud transactions in the same product line, and amortization and royalty expenses for intangible property directly used to provide the cloud transaction. R&E expenditures include all amounts incurred during the taxable year, whether deductible or not. When costs relate to multiple transactions, they are apportioned based on relative gross income.

Personnel factor: The personnel factor represents the total compensation paid to the taxpayer’s employees whose primary function is to directly contribute to the provision of the cloud transaction. This includes individuals engaged in managing, operating, and maintaining the technology and infrastructure supporting the cloud service. Although R&E personnel contribute directly to cloud transactions, their compensation is excluded from the personnel factor because it is included in the intangible–property factor. Additionally, compensation for employees performing business strategy, leadership, legal or compliance, marketing, communications, sales, business development, finance, accounting, clerical, human resources, administrative duties, or similar functions is also excluded. Similar to costs and expenses taken into account when computing the intangible–property factor, compensation paid to an employee whose primary function is to directly contribute to multiple cloud transactions must be allocated among cloud transactions based on the relative amount of time the employee spends contributing to each cloud transaction.

Tangible–property factor: The tangible–property factor equals the sum of the taxpayer’s depreciation expense for tangible property owned and rental expense for tangible property leased during the tax year, to the extent the property is directly used to provide the cloud transaction. Depreciation must be computed using the alternative depreciation system, without regard to Sec. 179 expensing or any additional first–year depreciation provisions.

Reseller examples

As noted above, both the final digital content regulations and the final cloud regulations introduced new examples pertaining to reseller business models.

The final digital content regulations provide an example of a reseller arrangement involving electronically delivered software (Regs. Sec. 1.861–18(h)(23)). In this example, a copyright owner hosts a computer program on its servers and grants a foreign affiliate the right to distribute digital copies to customers in the foreign affiliate’s jurisdiction (without the right to reproduce). The affiliate pays a fixed fee to the copyright owner for each copy of the program delivered and separately charges customers for perpetual use. The affiliate is responsible for managing the purchase/sale interactions with customers, including invoicing and collections, while the copyright owner creates and delivers the digital copies from its servers. The affiliate does not perform any functions to provide access to the computer program. The example concludes that these transactions are functionally and economically equivalent to back–to–back transfers of copyrighted articles, rather than transfers of copyright rights or services. Thus, the transaction is treated as a transfer of a copyrighted article from the copyright owner to the foreign affiliate, and then from the foreign affiliate to the customer. This example is depicted in the diagram “Transfer of a Copyrighted Article.”

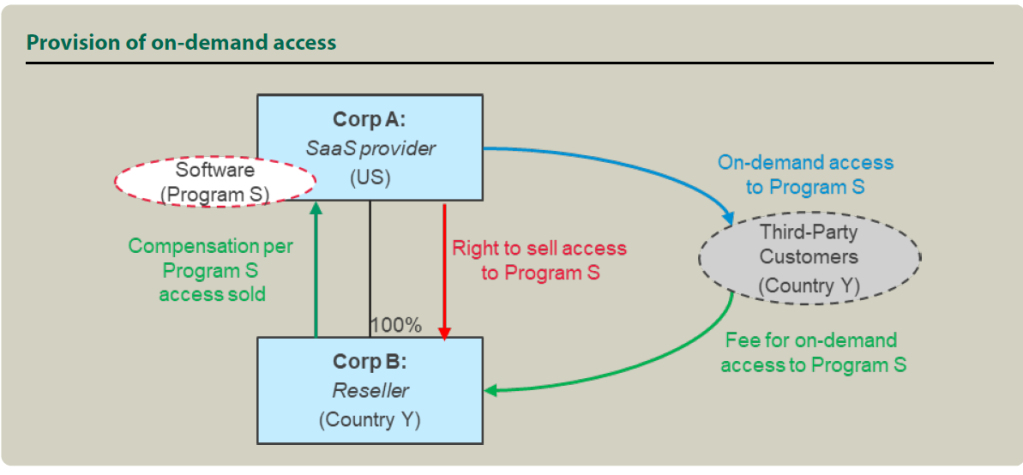

Similarly, the final cloud regulations include an example of a reseller of software as a service (Regs. Sec. 1.861–19(d)(10)). In this example, Corporation A owns the copyright to software that it hosts on its servers, which customers access only through the internet. Corporation A grants a foreign affiliate the right to sell access to the computer program to customers in its jurisdiction. The foreign affiliate is responsible for managing the purchase/sale interactions with customers, including invoicing and collections, while Corporation A is responsible for providing customers access to the computer program. The example concludes that Corporation A provides on–demand access to the computer program to its foreign affiliate, even though the foreign affiliate resells that access. The transaction between Corporation A and its foreign affiliate is treated as a cloud transaction and thus classified as the provision of services. The transaction between the foreign affiliate and its customers is also viewed as the provision of on–demand access to the computer program by the foreign affiliate and likewise classified as the provision of services. This example is depicted in the diagram “Provision of On–Demand Access.”

Implications for businesses with reseller arrangements

Providing digital content or cloud products through a reseller entity to customers in a particular jurisdiction is a relatively common supply chain model, both for U.S. and foreign owners of intellectual property (IP). Both examples above have implications for such businesses. While the examples indicate a U.S. copyright owner and a foreign affiliate, analogous treatment arguably would apply if the copyright owner were foreign and the reseller a U.S. entity.

In the case of a foreign software owner that sells U.S. customers access to its computer program through a U.S. reseller, the example at Regs. Sec. 1.861–19(d)(10) suggests that the payment from the U.S. reseller to the foreign software owner should be classified as a payment for services, as opposed to a license fee. This is significant because license fee payments are subject to U.S. withholding tax at a 30% rate (unless reduced under an applicable income tax treaty); conversely, payments for services rendered outside the United States are not subject to U.S. withholding tax. Here, the three–factor formula in the proposed cloud regulations may result in no U.S.-source income from cloud transactions (and, thus, no withholding required).

A similar result is expected if a U.S. tax resident provides access to software that it owns by way of a foreign reseller. While U.S. Treasury regulations are not binding on non–U.S. tax authorities, the above example provides an argument supporting the position that the payments made by the foreign reseller to the U.S. software owner should be treated as payments for services and, as such, not be subject to local withholding tax. Indeed, the preamble to the final cloud regulations states that this example was provided to address concerns that certain jurisdictions may treat such a payment as a royalty. This position may be particularly helpful to U.S. tax residents that are otherwise unable to claim a foreign tax credit for local withholding tax (e.g., due to being in a net operating loss position or an excess foreign tax credit position).

Foreign entities that own and sell digital content may also benefit. A foreign copyright owner may grant its U.S. affiliate the right to distribute (but not reproduce) digital copies to U.S. customers in exchange for a fixed fee for each copy delivered. Provided the U.S. affiliate is solely responsible for reseller operations as described in the example in the regulations (i.e., managing the purchase/sale interactions with customers, invoicing, and collections and not obtaining or exercising any copyrights), Regs. Sec. 1.861–18(h)(24) suggests that such a transaction should be treated as the sale of a copyrighted article rather than the transfer of copyrights or services. This is significant because treatment as the sale of a copyrighted article (rather than a lease) should result in no U.S. withholding tax being imposed on the payment if the benefits–and–burdens test set out at Regs. Sec. 1.861–18(f)(2) is met.

The above illustrations demonstrate the potential advantages taxpayers can obtain from proactive related–party supply chain planning.

Assessing the service supply chain

Given the many changes introduced in both the final regulations and the proposed cloud sourcing regulations, taxpayers engaged in the provision of digital content and cloud transactions should carefully review the new rules and assess their implications.

In light of the potentially beneficial implications of operating through a reseller structure, taxpayers providing such digital content and cloud transactions across borders should assess whether adjustments to their service supply chain model to incorporate a reseller approach could provide any advantages. Such an approach should allow transfer pricing, the taxpayer’s broader U.S. tax profile, non–U.S. tax implications, and commercial requirements, to be explored holistically.

Editor

Jeffrey N. Bilsky, CPA, is managing principal, Washington National Tax, with BDO USA, P.C. in Atlanta.

For additional information about these items, contact Bilsky at jbilsky@bdo.com.

Contributors are members of or associated with BDO USA, P.C.