The new CFC tax landscape after OBBBA

H.R. 1, P.L. 119-21, known as the One Big Beautiful Bill Act (OBBBA), introduced significant changes to the controlled foreign corporation (CFC) rules that affect U.S. taxpayers with foreign corporate interests. Two key amendments introduced under Section 70353 of the OBBBA are particularly noteworthy:

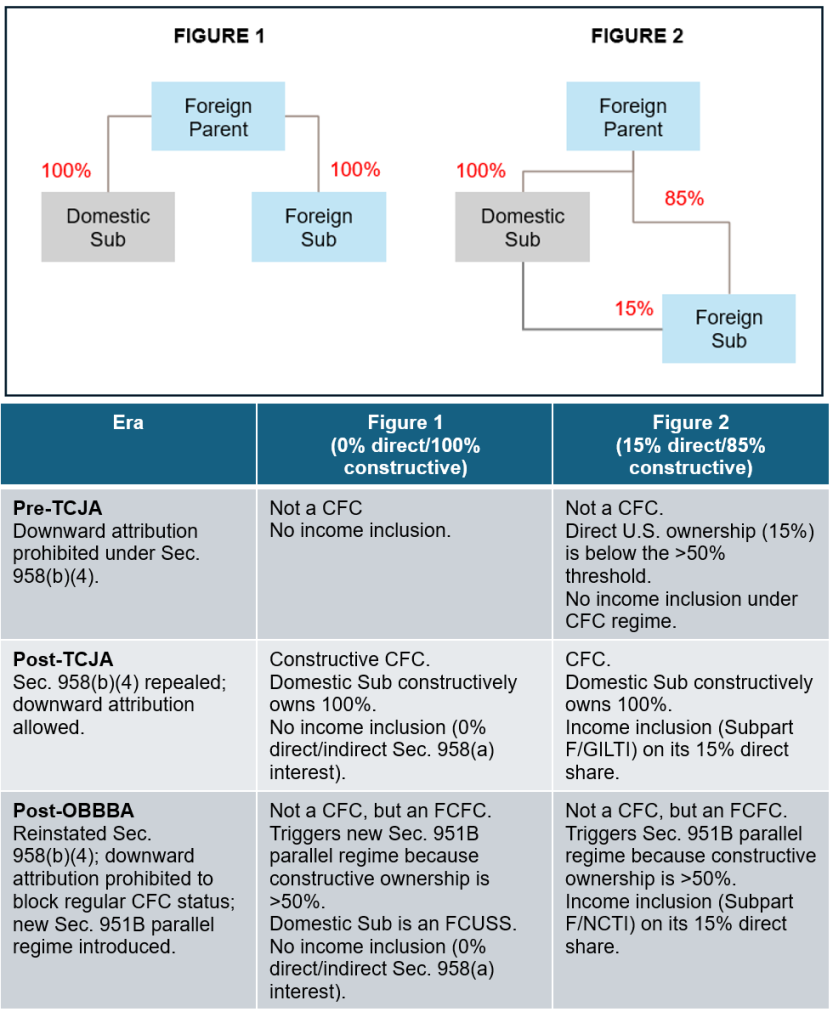

- Reinstatement of Sec. 958(b)(4): This provision prevents “downward attribution” by blocking the application of Sec. 318(a)(3). As a result, a U.S. domestic subsidiary will no longer be treated as owning stock in a foreign subsidiary that is owned by a foreign parent in the corporate ownership scenario illustrated in Figure 1 below.

- Introduction of Sec. 951B: This new section defines a “foreign controlled foreign corporation” (FCFC) and “foreign controlled United States shareholder” (FCUSS). In the corporate ownership scenario illustrated in Figure 2, Domestic Sub (an FCUSS) is now required to include in its income the earnings of Foreign Sub (an FCFC) under Subpart F or net CFC tested income (NCTI, formerly known as global intangible low-taxed income (GILTI)).

These amendments apply to tax years of foreign corporations beginning after Dec. 31, 2025.

US shareholder and CFC status

Broadly, a CFC is a foreign corporation that is more than 50% owned by U.S. shareholders by vote or value, directly, indirectly, or constructively. A “U.S. shareholder” for this purpose is defined as a U.S. person owning 10% or more of the combined voting power or total value of shares of the foreign corporation.

Stock ownership in a CFC can be held directly or indirectly through foreign entities under Sec. 958(a). Constructive ownership under Sec. 958(b) may be applied through three types of ownership attribution under Sec. 318(a) (with certain exceptions):

- Attribution among family members (Sec. 318(a)(1));

- Upward attribution from partnerships, estates, trusts, and corporations (Sec. 318(a)(2)); and

- Downward attribution to partnerships, estates, trusts, and corporations (Sec. 318(a)(3)).

Downward attribution and exception

Under Sec. 318(a)(3), stock owned directly or indirectly by partners, beneficiaries, or shareholders can be attributed to a partnership, estate, trust, or corporation. This “constructive ownership” means that the entity is treated as owning the stock owned by its partners, beneficiaries, or shareholders.

Before it was repealed in 2017 by the Tax Cuts and Jobs Act (TCJA), P.L. 115-97, Sec. 958(b)(4) provided an important exception by preventing stock owned by a foreign person from being attributed downward to a U.S. person. In other words, a U.S. entity could not be treated as owning stock held by a foreign person under Sec. 318(a)(3). For example, as illustrated in Figure 1, Domestic Sub would not be deemed to own stock in Foreign Sub that was actually owned by Foreign Parent.

Repeal of Sec. 958(b)(4)

The TCJA’s repeal of Sec. 958(b)(4) allowed downward attribution from foreign corporations to domestic corporations when determining U.S. shareholder status and whether a foreign corporation was a CFC. The legislative history explained that this change was intended to address transactions designed to “de-control” foreign subsidiaries, whereby U.S. shareholders reduced their ownership below CFC control thresholds while retaining meaningful economic participation in foreign earnings, to avoid Subpart F and GILTI taxation (H.R. Rep’t No. 115-409, 115th Cong., 1st Sess., Pt. 2, at 387 (2017)).

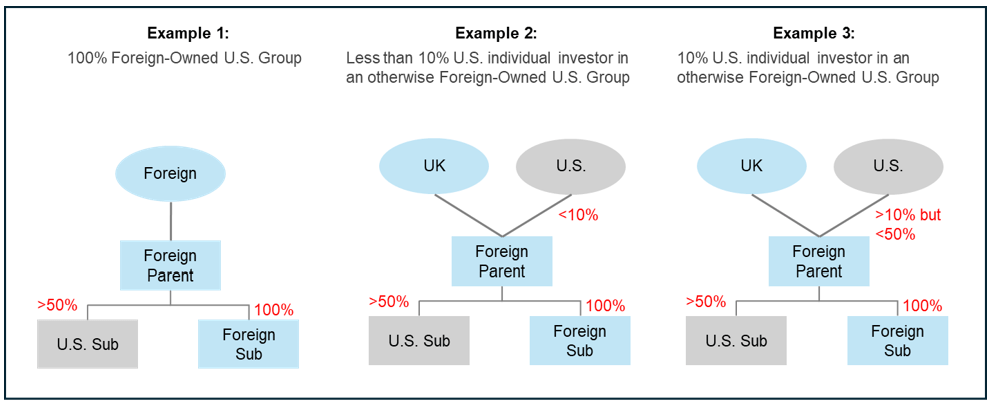

However, instead of narrowly targeting only these “de-control” transactions, Congress repealed Sec. 958(b)(4) entirely. This broad repeal significantly expanded the scope of the CFC rules. As a result, many more U.S. taxpayers with investments in foreign structures faced increased compliance burdens and became subject to income inclusions from CFCs that would not have applied under the prior rules. In Figure 1 above, Domestic Sub would have been treated as constructively owning stock of Foreign Sub that was directly owned by Foreign Parent as a result of the repeal. Accordingly, through this downward attribution, Domestic Sub was treated as a U.S. shareholder, and Foreign Sub was classified as a CFC. If, in addition, U.S. shareholders owned at least 10% of Foreign Parent — as illustrated in Example 3 below — those U.S. shareholders would have been subject to a Subpart F or GILTI income inclusion. Note that this income inclusion did not apply in Examples 1 and 2. This outcome arose because U.S. Sub was treated as owning more than 50% of Foreign Sub’s stock under the constructive ownership rules.

The return of Sec. 958(b)(4) and introduction of Sec. 951B

To address these unintended consequences, the OBBBA prospectively reinstated the general prohibition on foreign-to-domestic downward attribution by restoring Sec. 958(b)(4). This means that, for tax years of foreign corporations beginning after Dec. 31, 2025, stock owned by a foreign person can no longer be attributed downward to a U.S. person, returning to the pre-TCJA rule.

At the same time, the OBBBA introduced new Sec. 951B, which creates a new class of taxpayers subject to the Subpart F income inclusion rules under Sec. 951(a) and the NCTI inclusion rules under Sec. 951A(a). This targeted approach is designed to address only the specific “de-control” transactions that motivated the original TCJA change, rather than applying broadly to all foreign-to-domestic downward-attribution scenarios.

In summary, the OBBBA limits the scope of the TCJA’s changes, aiming to prevent unintended consequences for U.S. taxpayers while still addressing the targeted transactions Congress intended to tackle.

FCUSSes and FCFCs under Sec. 951B

Sec. 951B establishes a separate but parallel inclusion regime that targets the avoidance of CFC status, requiring FCUSSes of FCFCs to include Subpart F income, amounts determined under Sec. 956, and NCTI.

A FCUSS is defined as any U.S. person who would be a U.S. shareholder of a foreign corporation if (Sec. 951B(b)):

- Sec. 951(b) were applied by substituting “more than 50 percent” for “10 percent or more”; and

- Sec. 958(b) were applied without regard to Sec. 958(b)(4) (i.e., applied as if downward attribution from foreign persons to U.S. persons were permitted).

In effect, an FCUSS is any U.S. person that would own (directly, indirectly, or constructively) more than 50% of a foreign corporation if the prohibition on downward attribution under Sec. 958(b)(4) did not apply.

The status of an FCFC is determined with respect to an FCUSS. The term “foreign controlled foreign corporation” refers to a foreign corporation other than a CFC that would be classified as a CFC if (Sec. 951B(c)):

- Sec. 957(a) were applied by substituting “foreign controlled U.S. shareholder” for “U.S. shareholder”; and

- Sec. 958(b) were applied without regard to Sec. 958(b)(4) (i.e., applied as if downward attribution from foreign persons to U.S. persons were permitted).

Essentially, an FCFC is any foreign corporation that would be more than 50% owned (directly, indirectly, or constructively) by FCUSSes if the prohibition on downward attribution under Sec. 958(b)(4) did not apply.

Impact of Sec. 958(b)(4) restoration and new Sec. 951B

Some examples will help illustrate the impact of the restoration of Sec. 958(b)(4) and the introduction of new Sec. 951B on the classification of foreign subsidiaries and the application of U.S. tax rules. In the corporate ownership scenarios shown in Examples 1, 2, and 3 above, Foreign Sub may no longer be classified as a CFC. As a result, minority U.S. investors (the 10% U.S. investor in Foreign Parent in Example 3) will no longer be subject to phantom income inclusions or filing requirements for Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations.

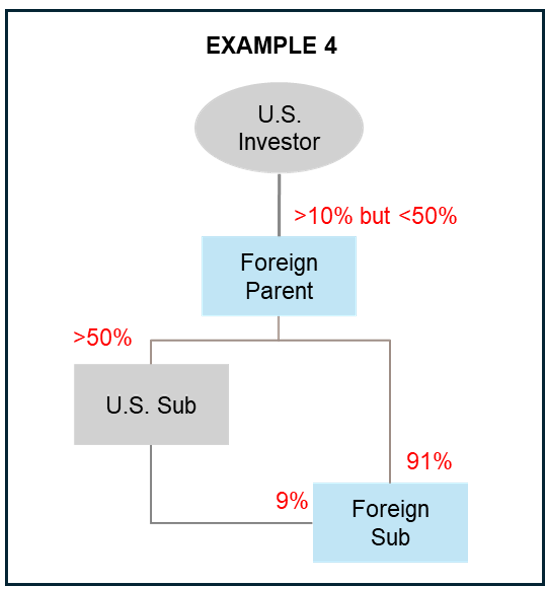

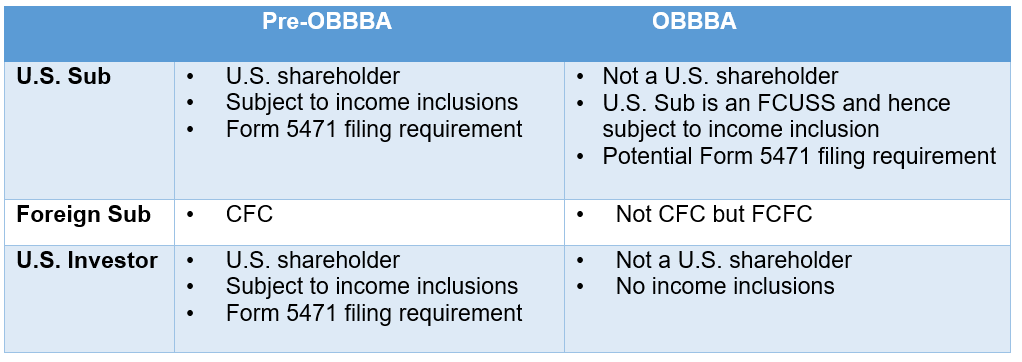

In Example 4, however, under Sec. 951B, U.S. Sub will be considered to constructively own 91% of Foreign Sub (in addition to the 9% directly owned interest) due to the downward attribution of Foreign Parent’s ownership in Foreign Sub. This attribution is relevant for purposes of qualifying U.S. Sub as an FCUSS and Foreign Sub as an FCFC. As a result, U.S. Sub will be subject to the CFC inclusion rules with respect to its 9% direct ownership in Foreign Sub, as required by Sec. 951B. However, U.S. Investor will not be considered an FCUSS of Foreign Sub and, therefore, will not have any income inclusion. See a summary of these effects in the table, “OBBBA Amendments and Prior Law Compared.”

OBBBA amendments and prior law compared

Portfolio-interest exemption

The restoration of Sec. 958(b)(4) has significant implications for cross-border financing structures, particularly in relation to the portfolio-interest exemption. Under the rules introduced by the TCJA, certain foreign subsidiaries such as Foreign Sub in Examples 1, 2, and 3 would have been classified as CFCs due to downward attribution. As a result, if U.S. Sub paid interest on a loan to such a foreign subsidiary, those payments would have been considered made to a related CFC under Sec. 881(c)(3)(C), thereby disqualifying the interest from the Sec. 881(c) portfolio-interest exemption and subjecting it to 30% statutory U.S. withholding tax, unless reduced by an applicable income tax treaty.

With the reinstatement of Sec. 958(b)(4), however, entities such as Foreign Sub in Examples 1, 2, and 3 are no longer treated as CFCs solely due to downward attribution. Consequently, interest paid by U.S. Sub to Foreign Sub may now qualify for the portfolio-interest exemption, provided all other requirements are met.

In Example 4, while Foreign Sub would be classified as an FCFC, it is unclear whether Treasury would exercise its regulatory authority under Sec. 951B(d) to treat an FCFC as a CFC for purposes of the portfolio-interest exemption rules. In the absence of pertinent guidance, an FCFC should not be considered a CFC for purposes of Sec. 881(c)(3)(C). Therefore, unless Treasury issues regulations to the contrary, interest payments to an FCFC would also appear to qualify for the portfolio-interest exemption.

These developments highlight the importance of reviewing existing and proposed financing structures in light of the restored attribution rules and the evolving regulatory regime.

CFC/PFIC overlap

With the restoration of Sec. 958(b)(4) under the OBBBA, many foreign corporations that were previously classified as “constructive CFCs” due to downward attribution will have lost their CFC status beginning in 2026. As a result, U.S. shareholders will no longer benefit from the CFC/passive foreign investment company (PFIC) overlap rule under Sec. 1297(d), which had shielded them from the PFIC regime during periods when the foreign corporation was treated as a CFC. Once CFC status is lost, U.S. shareholders must reassess their exposure to the PFIC rules and consider the need for timely elections or other planning.

Importantly, the introduction of Sec. 951B does not resolve this issue. The statutory language of Sec. 951B does not automatically extend the CFC/PFIC overlap rule to FCFCs. Unless Treasury issues specific guidance, an FCFC will not be treated as a CFC for purposes of Sec. 1297(d), and the overlap rule will not protect U.S. shareholders of an FCFC from the PFIC regime. This means that, absent further regulatory action, a foreign corporation such as Foreign Sub could be classified as a PFIC with respect to U.S. shareholders, even if it is subject to the new FCFC rules.

In practice, this creates significant uncertainty and potential exposure for U.S. shareholders and U.S. corporations with interests in foreign entities that are no longer CFCs but may be classified as FCFCs. Taxpayers should carefully review their ownership structures and proactively assess the PFIC implications for tax years beginning after Dec. 31, 2025, to avoid unexpected adverse tax consequences.

Advantages, but with complications

The OBBBA’s reinstatement of Sec. 958(b)(4) and introduction of Sec. 951B mark a significant recalibration of the CFC rules. By restoring the prohibition on foreign-to-domestic downward attribution, Congress has narrowed the scope of CFC status, reducing the compliance burden and unintended income inclusions for many U.S. taxpayers with foreign interests. At the same time, the new Sec. 951B regime ensures that targeted de-control structures remain subject to Subpart F and NCTI inclusions, closing the loophole that motivated the TCJA’s original repeal of the downward-attribution rule.

However, these changes also give rise to new complexities. The parallel FCUSS/FCFC regime introduces new reporting and inclusion requirements, while the loss of CFC status for many foreign corporations revives PFIC exposure for U.S. shareholders. The impact on the portfolio-interest exemption and the absence of automatic CFC/PFIC overlap protection for FCFCs add further uncertainty. Taxpayers must closely monitor forthcoming Treasury guidance to clarify the interaction of these rules, particularly regarding foreign tax credits, previously taxed earnings and profits (PTEP), and reporting obligations.

More specifically, affected taxpayers should consider taking the following steps:

- Review entity classifications: Reassess all foreign ownership structures to determine which entities will lose or gain CFC status, and identify any U.S. persons who will be classified as FCUSSes under the new Sec. 951B regime.

- Evaluate tax exposure: Model the impact of Subpart F, Sec. 956, and NCTI inclusions for both CFCs and FCFCs, and reassess exposure to the PFIC regime for entities losing CFC status.

- Update compliance processes: Prepare for changes to Form 5471 and related reporting, and verify that all affected entities and shareholders are identified for tax years beginning after Dec. 31, 2025.

- Assess financing structures: Revisit cross-border financing arrangements to determine continued eligibility for the portfolio-interest exemption in light of the restored attribution rules.

- Monitor regulatory developments: Stay abreast of Treasury and IRS guidance on Sec. 951B, especially as it relates to foreign tax credits, PTEP ordering, basket assignment, and the CFC/PFIC overlap.

- Coordinate globally: Engage with foreign parent companies, subsidiaries, and other stakeholders to confirm coordinated compliance and to address any necessary restructuring.

— Shaiq Ibrahim, CPA, E.A., is a tax senior manager, International Tax Services, and Grace Shen, CPA, MBA, is a tax managing director, International Tax Services, both with BDO USA in New York City. To comment on this article or to suggest an idea for another article, contact Paul Bonner at Paul.Bonner@aicpa-cima.com.