State tax history at the United States’ 250th anniversary

Editor: Brian Myers, CPA

July 4, 2026, is the 250th anniversary of the adoption of the Declaration of Independence by the Continental Congress composed of 56 members representing the 13 colonies. One of numerous “injuries and usurpations” by the kings of Great Britain listed as reasons to declare that the colonies should be “Free and Independent States” was the British crown’s “imposing Taxes on us without our Consent”— a statement better known as “taxation without representation.”

In honor of the 250th anniversary of this country’s independence and the relevance of taxation in the call for that independence, this column highlights some significant events and players in the history of multistate taxation, with an emphasis on the last 75 years. This history is rich with fascinating U.S. Supreme Court cases over many decades, several of which are still regularly cited by courts; challenges in identifying when the U.S. Constitution allows states to impose taxes; cases determining the legality of various taxes and their breadth under U.S. and state constitutions; and significant and ongoing changes in how we live and do business that challenge tax policy considerations. This column cannot address all of this rich history; it focuses on some key elements and the continuing relevance of this history to today’s multistate tax scene. And to test your knowledge, try out the “Quiz on State Tax Firsts” at the end of this article.

Acts of Congress

1777 pre–Constitution: The Articles of Confederation, adopted on Nov. 15, 1777, provided that defense and “general welfare” expenses be paid from a “common treasury” funded by the states, with state legislatures having the authority to lay and levy taxes.1 This was preceded by a decision on Sept. 10, 1777, to appoint a committee to recommend that states impose taxes.2 Since 1777, Congress, presidents, governors, and state legislatures have formed numerous committees to study taxation.

Statehood and tax restrictions: The 13 original states joined the federal union by ratifying the Constitution. Later states were admitted by acts of Congress.3 These laws sometimes included tax limitations. For example, the Act of June 23, 1836 (24th Congress), to admit Michigan prescribed that the state “shall in no case and under no pretence whatsoever, impose any tax, assessment or imposition of any description upon any of the lands of the United States within its limits.” The Act of Sept. 9, 1850 (31st Congress), admitting California to the union went further: “[I]n no case shall non–resident proprietors, who are citizens of the United States, be taxed higher than residents,” and no “tax, impost, or duty” shall be imposed on use of “all the navigable waters within the said State” as “common highways.”

16th Amendment: Prior to ratification of the 16th Amendment to the U.S. Constitution in February 1913, the federal government relied on customs, duties, excise taxes, inheritance tax, and a temporary income tax during the Civil War. The 16th Amendment allowed for an income tax, which affected all states, even states that did not impose an income tax. For example, after 1913, taxing decisions of state lawmakers would include consideration of whether taxpayers could reduce their federal income taxes by state and local taxes paid. The Revenue Act of 1964, P.L. 88–272, provided a specific list of deductible taxes. The Tax Reform Act of 1986, P.L. 99–514, eliminated the ability for individuals to deduct state and local sales taxes but reinstated their deductibility in 2004 as an alternative to deducting state and local income taxes. In 2017, the Tax Cuts and Jobs Act, P.L. 115–97, imposed a $10,000 limit on an individual’s state and local tax (SALT) deduction.4 This led a majority of states, supported by the IRS via Notice 2020–75, to impose passthrough entity taxes (PTETs) to help some taxpayers obtain a greater SALT deduction.5

Federal income tax changes and states’ needs for revenue result in regular attention by state lawmakers to federal conformity considerations. In addition, major and minor tax proposals of Congress often lead states to make recommendations to Congress, particularly where the tax will have an adverse effect, such as imposition of a national sales tax or other type of broad–based consumption tax.6

P.L. 86–272 and the federal study of state taxation: The U.S. Constitution gives Congress the power to regulate commerce among the states (the Commerce Clause). For state taxes, this power generally comes into play when taxpayers challenge a state’s authority to impose a particular tax on them. A rare example of Congress’s exercising this authority to enact legislation came in 1959 in response to the U.S. Supreme Court decision in Northwestern States Portland Cement Co. v. Minnesota, 358 U.S. 450 (1959), which found valid the state’s imposition of tax on a company’s income “properly apportioned” to the state and “reasonably attributable to” business activities in the state. Concerned about possible overreach by states, Congress enacted the Interstate Income Tax Act of 1959, better known as P.L. 86–272, specifying when a state can impose net income taxes on a business selling tangible personal property.7 Basically, if the company’s only activity in the state is the solicitation of orders that are approved and shipped from outside the state, the company does not have nexus in the state for income tax purposes.

P.L. 86–272 continues to generate issues on its application, including those due to changes in how business is conducted today versus in 1959. Efforts by Congress over several decades to update this law, such as to broaden it beyond income taxes and the sale of tangible personal property, have failed.

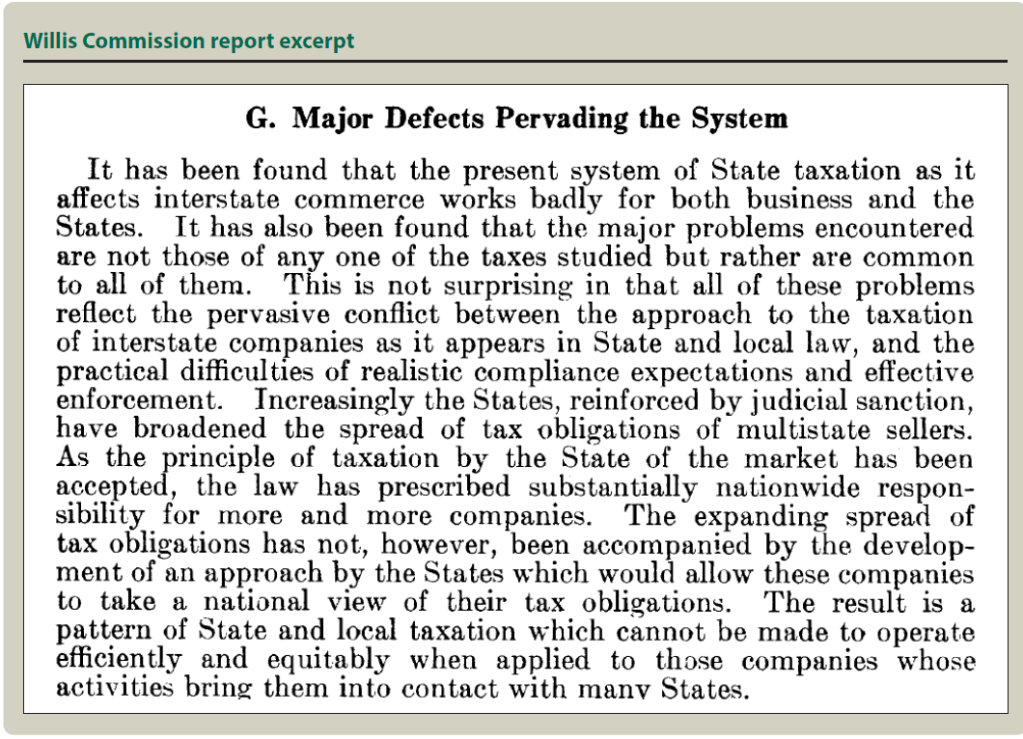

Congress intended that P.L. 86–272 be temporary while it conducted a study of state taxation called for by the legislation. Lacking an expiration date, this law remains in its original form, providing an income tax nexus rule drafted long before today’s ways of doing business were imagined. The congressional study by the so–called Willis Commission produced a report in the early 1960s exceeding 1,000 pages, addressing “all matters pertaining” to state taxation of business activities in interstate commerce. For a sense of the issues the commission addressed and their continuing relevance, see the excerpt from Volume 4 of the report (page 1127), “Willis Commission Report Excerpt.”

The Internet Tax Freedom Act: The internet’s emergence in the 1990s as a new way of conducting commerce raised and exacerbated lingering multistate tax issues regarding nexus. A new business model that made it easy to have customers in all states while having a physical presence in only a few states raised concerns for states, primarily loss of income tax revenues and growth in hard–to–collect use taxes. Many lawmakers and businesses had concerns about new laws impeding e–commerce’s growth. The congressional remedy that emerged was the 1998 Internet Tax Freedom Act (ITFA) (Title XI of P.L. 105–277).

The ITFA imposed a three–year moratorium preventing states from imposing new taxes on internet access and any multiple or discriminatory taxes on e–commerce. This was later extended and made permanent.8 This law also created the Advisory Commission on Electronic Commerce (ACEC) to “conduct a thorough study of Federal, State and local, and international taxation and tariff treatment of transactions using the Internet and Internet access and other comparable intrastate, interstate or international sales activities.”9

The focus on state tax issues in e–commerce has evolved more broadly today to activities involving digital goods and services, including actions by some states to create new taxes, such as Maryland’s digital advertising tax. The ITFA remains relevant here if taxation of digital items (via the internet) treats digital activity differently from its equivalent, such as print advertising. Congress and the states will likely continue to work on these issues and possible updates to P.L. 86–272 for many more years.

State taxation of retirement income: In 1996, Congress exercised its Commerce Clause powers over interstate commerce but outside the business context. With P.L. 104–95 (Jan. 10, 1996), Congress prohibited any state from imposing income tax on any retirement income of an individual who is not a resident or domiciliary of that state. This law also prevents this income from being taxed in more than one state (such as in both the state where the pension was earned (and taxes deferred) and the state where the retiree lives when collecting the pension income).

The House Judiciary Committee, however, recognized “the rights of States to raise revenues in a manner of their own choosing” and acknowledged that “Congress should restrict State taxing authority only when such action is clearly necessary. The Committee concludes, however, that the practice of taxing nonresidents’ pension income represents such a case. Despite the legal and conceptual bases for pension source taxes, the burdens imposed on retirees, especially those with relatively low incomes, are all too often simply unreasonable.”10

US Supreme Court decisions

The U.S. Supreme Court arguably plays the most significant role in multistate taxation and in shaping its history with various twists and turns. Since the early 1800s, there have been numerous cases on the states’ power to tax activities of the federal government and when states may impose taxes on activities and income of multistate businesses, discussed next.11

An early landmark case still cited today, McCulloch v. Maryland, 17 U.S. 316 (1819), held that Maryland did not have authority to impose taxes on a federal bank. The Supreme Court did acknowledge the taxing power of states but noted it had restrictions. Per the Court:

[T]he power of taxation is one of vital importance; that it is retained by the States; that it is not abridged by the grant of a similar power to the Government of the Union; that it is to be concurrently exercised by the two Governments — are truths which have never been denied. But such is the paramount character of the Constitution that its capacity to withdraw any subject from the action of even this power is admitted. The States are expressly forbidden to lay any duties on imports or exports except what may be absolutely necessary for executing their inspection laws. If the obligation of this prohibition must be conceded — if it may restrain a State from the exercise of its taxing power on imports and exports — the same paramount character would seem to restrain, as it certainly may restrain, a State from such other exercise of this power as is in its nature incompatible with, and repugnant to, the constitutional laws of the Union.12

Nexus rulings of the Supreme Court have generally followed changes in ways of conducting business from storefronts to catalogs to e–commerce. Highlights of this history:

- Miller Brothers Co. v. Maryland, 347 U.S. 340 (1954): The Due Process Clause of the 14th Amendment prohibits Maryland from imposing sales tax on a Delaware business selling to customers from Maryland inside the business’s store in Delaware, with purchases sometimes delivered to the customer by common carrier or the seller’s own truck.13

- National Bellas Hess v. Dept. of Revenue, 386 U.S. 753 (1967): Per both the Due Process Clause of the 14th Amendment and the Commerce Clause, a state may not impose sales and use tax collection obligations on a seller if their only connection with in-state customers is by common carrier or by mail.

- Quill Corp. v. North Dakota,504 U.S. 298 (1992): When a seller purposefully directs sales activities to a state (such as by shipping catalogs to businesses in the state), the Due Process Clause does not prohibit a state from imposing sales and use tax collection obligations. However, a state’s enforcement of such duties poses an “unconstitutional burden on interstate commerce” if the seller does not have a physical presence in the state.

- South Dakota v. Wayfair, Inc., 585 U.S. 162 (2018): The physical-presence rule of the Quill decision is “unsound and incorrect,” and substantial nexus such as significant business activity in the state is sufficient for a state to impose tax obligations on a business.

Despite the span of years for these four cases, the last three quoted the Supreme Court’s explanation in Miller Brothers for the meaning of the Due Process Clause. In Miller Brothers, the Court stated that it was a “time–honored concept: that due process requires some definite link, some minimum connection, between a state and the person, property, or transaction it seeks to tax.”14

The progression of these nexus decisions leaves the authority for states to tax multistate activities mostly as Commerce Clause matters within the bounds for Congress to resolve. Continuing but slow efforts in this area may lead Congress to evaluate whether today’s variety of economic nexus standards among states can be made simpler and more certain. For more on court decisions and other determining developments, see “Timeline of State Taxation Events Related to Federal Taxes” at the end of this article.

Looking backward and forward: Our changing economy and society

The types of state taxes and how they are measured has been influenced by a long history of changes in our economy and society — how we live and do business. For example, as described above, changes from in–store commerce to catalogs to e–commerce changed how the Supreme Court interpreted key constitutional parameters affecting state taxing authority in multistate transactions.

Changes in transportation from personal modes of travel (such as horse–drawn carriage) to use of railroads and buses brought about new tax issues and evolving solutions. For example, the Court addressed assessment of property taxes on railroads in Union Pacific Railway Co. v. Cheyenne, 113 U.S. 516 (1885), which led to continued advances in how property taxes and income taxes should be apportioned among states.

The Great Depression resulted in a drop in state income taxes, leading states to enact sales and use taxes.

Changes in how we work, from in employers’ offices to working remotely from home or even from multiple locations, are likely to change tax laws, such as those to simplify and standardize tax determinations (e.g., how many days an employee must be in a state before state income taxes are owed).

Technological advances have shaped state tax history, such as noted earlier for e–commerce. These advances will likely shape future history in simplifying taxation, such as through better use of digital data and artificial intelligence to apportion business income among states or collecting and remitting sales taxes at the point of sale and avoiding the need to file tax returns. Technological advances will continue to raise new issues for state taxation, including whether robots should be taxed, whether increased energy usage of some technologies should be taxed, and even how changes in outer space activities affect state taxes.

No doubt, the continued history of state taxation will still involve state authority to tax, while also bringing new questions we cannot even imagine today.

Quiz on state tax firsts

Which state was the first to impose (answers below):

- A personal income tax?

- A corporate income tax?

- A sales tax?

- An inheritance tax?

- A gasoline excise tax?

- A form of a value-added tax (VAT)?

- A digital advertising tax?

Answers:

- Pennsylvania in 1840 (Walczak, Kaeding, and Drenkard, “Pennsylvania: A 21st Century Tax Code for the Commonwealth,” Tax Foundation (2018)).

- Wisconsin in 1911 (Emanuel, “When Did Your State Adopt Its Corporate Income Tax?,” Tax Foundation (June 19, 2014)).

- Mississippi in 1932; many states followed, as another revenue source was needed due to the Great Depression (Multistate Tax Commission (MTC), “History and Terminology“).

- Pennsylvania in 1826 (TaxEDU Glossary, “Inheritance Tax,” Tax Foundation).

- Oregon in 1919 (Oregon.gov, “Fuels Tax History“).

- Michigan in 1953, with its business activities tax, which was akin to a VAT (Emanuel, “When Did Your State Adopt Its Corporate Income Tax?,” Tax Foundation (June 19, 2014)).

- Maryland in 2021 (MTC, above).

Timeline of state taxation events related to federal taxes

1777 — Congress appoints a committee to recommend that states begin imposing taxes to assist federal operations.

1819 — McCulloch v. Maryland holds that a state may not impose a tax on a federal bank.

1909 — Alabama is first state to ratify the 16th Amendment to the U.S. Constitution.

1935 — Right to inspect federal individual tax returns given to state tax officials (via the Revenue Act of 1935, P.L. 74–407).

1949 — The IRS starts a pilot program to exchange abstracts of audits with state tax agencies.

1966 — The IRS begins providing information to state agencies using magnetic media.

1970 — Volunteer Income Tax Assistance (VITA) program launches to help low–income individuals with federal and state income tax filings.

1972 — IRS Service Centers in Fresno, Calif., and Memphis, Tenn., start processing returns. While not the first IRS operations in states, the location of these major offices brings a significant number of jobs to a state.

1972 — P.L. 92–512 (Oct. 20, 1972) added Secs. 6361—6365 to allow the IRS to collect and administer “qualified State individual income taxes” of the state if an agreement was in effect. Repealed in 1990 by the Omnibus Budget Reconciliation Act, P.L. 101–508; no state signed up for this option.

1983 — International Fuel Tax Agreement (IFTA) for streamlined, joint collection of state fuel taxes on interstate motor carriers starts. In 1991, Congress enacts the Intermodal Surface Transportation Efficiency Act, P.L. 102–240, making the IFTA mandatory for enforcement of any state fuel use tax. Today the agreement includes the 48 contiguous states and 10 Canadian provinces.

1989 — Taxpayers in 36 states could file returns electronically, leading states to also support e–filing (Rev. Proc. 89–57 and its later updates).

2015 — The IRS formed the Security Summit, a coalition of state tax agencies and private-sector companies involved in tax preparation and software development that work together to identify and address identity theft and similar data security matters (IRS, “About the Security Summit“).

2025 — Reduction in workforce and funding at the IRS puts pressure on states to increase their audit activity and provide more taxpayer services.

Contributors

Annette Nellen, CPA, CGMA, Esq., is a professor in the Department of Accounting and Finance at San José State University in San José, Calif.; a member of the AICPA State and Local Taxation Technical Resource Panel (SALT TRP); and a past chair of the AICPA Tax Executive Committee. She also is the editor of The Tax Adviser’s Campus to Clients column. Brian Myers, CPA, is a partner at Crowe LLP in Indianapolis and chair of the SALT TRP. For more information about this column, contact thetaxadviser@aicpa.org.

Footnotes

2Treasury, IRS Historical Fact Book: A Chronology, 1646–1992, p. 14.

3U.S. Constitution, Article IV, Section 3, Clause 1.

4Amended by the law commonly known as the One Big Beautiful Bill Act, H.R. 1, P.L. 119-21, to temporarily raise the limit to $40,000, adjusted for inflation and subject to an adjusted gross income phaseout. For a history of the SALT deduction, see Congressional Research Service, Federal Deductibility of State and Local Taxes (Oct. 16, 2024).

5See AICPA PTET map and related resources.

6During the 1990s, several hearings were held in Congress on a flat tax, sales tax, and other types of consumption taxes to replace all or a portion of the federal income tax. Significant reports produced on the effect of such proposed changes on states include U.S. Government Accountability Office Rep’t No. GGD-90-50, State Tax Officials Have Concerns About a Federal Consumption Tax (March 1990); Joint Committee on Taxation, Impact on State and Local Governments and Tax-Exempt Organizations of Replacing the Federal Income Tax (JCS-4-96) (April 30, 1996); and California Franchise Tax Board, The Impact of the Flat Tax on California, 1995.

7For the history leading up to enactment of P.L. 86-272, see Nellen, “Public Law 86-272 Reaches Its 60-Year Anniversary,” Tax Notes State (Sept. 9, 2019).

8See Congressional Research Service, The Internet Tax Freedom Act and Federal Preemption (Oct. 18, 2021).

9ITFA, §1102(g)(1). The ACEC’s report was submitted to Congress in April 2000. The report and various related documents can be found at https://govinfo.library.unt.edu/ecommerce/press.htm.

10H.R. Rep’t No. 104-389, 104th Cong. 1st Sess. 5 (1995).

11Another area of state taxation addressed by the Court involved when (and how) a state may consider unitary concepts of worldwide income of business activities in imposing income tax. See, for example, Container Corp. of America v. Franchise Tax Board, 463 U.S. 159 (1983), and Barclays Bank PLC v. Franchise Tax Board of California, 512 U.S. 298 (1994).

12McCulloch, 17 U.S. at 425.

13A dissenting opinion in Miller Brothers noted that the seller’s choice to regularly deliver goods to Maryland using its own truck posed no issue under the Due Process Clause to allow the state to impose tax collection obligations on such sales delivered in state.

14Miller Brothers, 347 U.S. at 344–45.