Calculating and presenting state income tax effects under ASC Topic 740

Editor: Annette Nellen, Esq., CPA, CGMA

A corporation is required to pay income tax to any state or locality that levies one if the corporation has nexus there. These state income tax payments are deductible in the corporation’s federal income tax calculation, so paying the state–level tax makes the federal income tax expense lower than it otherwise would be. The combined income tax burden across jurisdictions is therefore not the sum of the statutory rates. Rather, it reflects the interplay of the two systems, resulting in a lower federal expense once the benefit of deducting the state expense is considered.

Using a cumulative example, this column illustrates how public business entities (PBEs) incorporate state income taxes into the income tax provision. Specifically, it walks the reader through calculating and constructing the current and deferred income tax expense breakout and the effective tax rate reconciliation, both required disclosures for PBEs as part of the income tax footnote. The accompanying Excel file provides full calculations of each step of the in–text example with explanatory notes, so the reader is encouraged to examine the Excel worksheets alongside the tables in this column. The Excel file also provides additional fact patterns for the user to complete after the steps of the cumulative example are understood.

This example is presented for use in an undergraduate or graduate–level income tax course but should also be of interest for in–house training at a CPA firm.

Cumulative example

Income tax rates

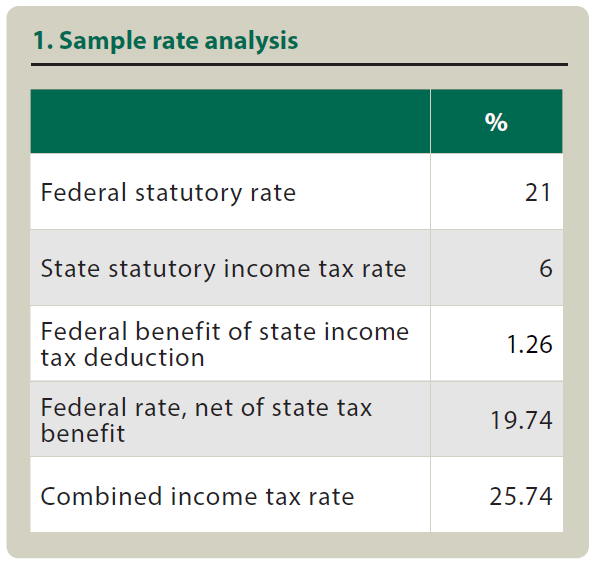

The table “1. Sample Rate Analysis” illustrates the interaction of jurisdictional income taxes assuming a domestic, U.S.-domiciled PBE that apportions 100% of its income to one state. The United States has a 21% statutory rate, and the state has a 6% statutory rate with no modifications to income. In this example, the federal benefit of the state deduction equals 1.26% (6% × 21%), effectively reducing the burden of the federal rate to 19.74% (21% – 1.26%). Therefore, the combined net burden across both federal and state jurisdictions for the PBE is 25.74% (19.74% + 6%).

Calculating current and deferred income tax expense

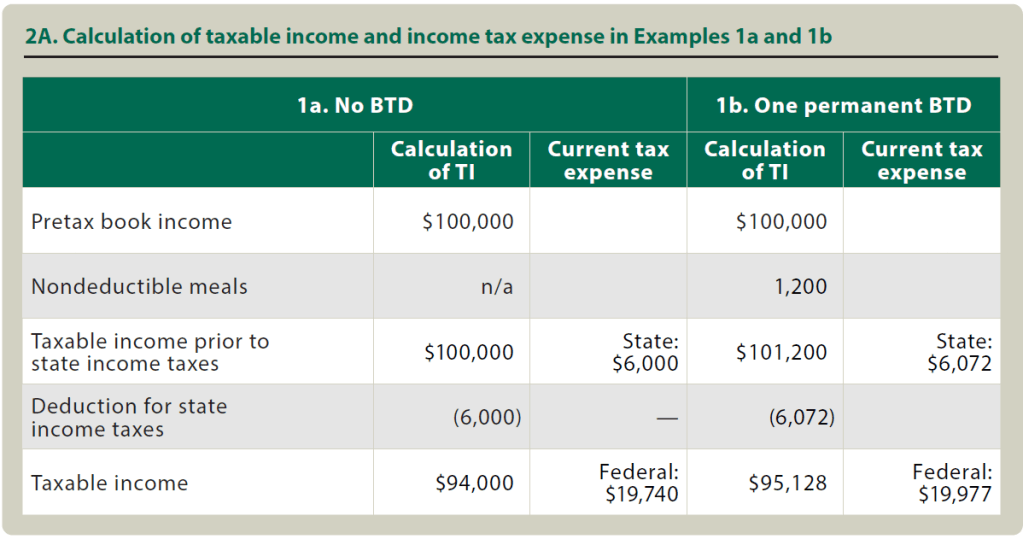

Example 1a: No BTD: The PBE reports pretax income for financial purposes of $100,000 prior to income taxes for both federal and state jurisdictions, all from continuing operations. The PBE has no book–tax differences (BTDs). As such, its taxable income prior to the state tax deduction equals the pretax book income of $100,000. The state will tax this amount at 6%, generating $6,000 of current state tax expense for the corporation. After deducting the state income tax for federal purposes, federal taxable income is $94,000. Applying the 21% federal statutory rate to this amount produces current federal income tax expense of $19,740. Because there are no temporary differences, there is no deferred tax expense for either jurisdiction.

The table “2A. Calculation of Taxable Income and Income Tax Expense in Examples 1a and 1b” presents the calculation of federal taxable income (TI) and associated current tax expense amounts for this fact pattern in the first pair of columns. Note that the total current income tax expense across the two jurisdictions is $25,740 ($6,000 + $19,740), consistent with the 25.74% combined rate presented in Table 1 multiplied by taxable income prior to state income taxes of $100,000.

Example 1b: One permanent BTD: Now assume the PBE has one permanent book–tax difference; specifically, it has $1,200 of nondeductible meals expenses. In this instance the PBE will add $1,200 to its pretax book income to reverse out the nondeductible portion of meals expenses, yielding taxable income prior to state income taxes of $101,200 and current state tax expense of $6,072 ($101,200 × 6%). Incorporating the state tax deduction at the federal level yields federal taxable income of $95,128, which generates $19,977 of federal current tax expense at the 21% federal rate.

In this scenario, total tax expense across jurisdictions increases to $26,049 ($6,072 + $19,977), which is $309 higher than when there was no permanent difference. The amount of this increase is consistent with the combined tax effect of the lost $1,200 deduction ($1,200 × 25.74% = $309).

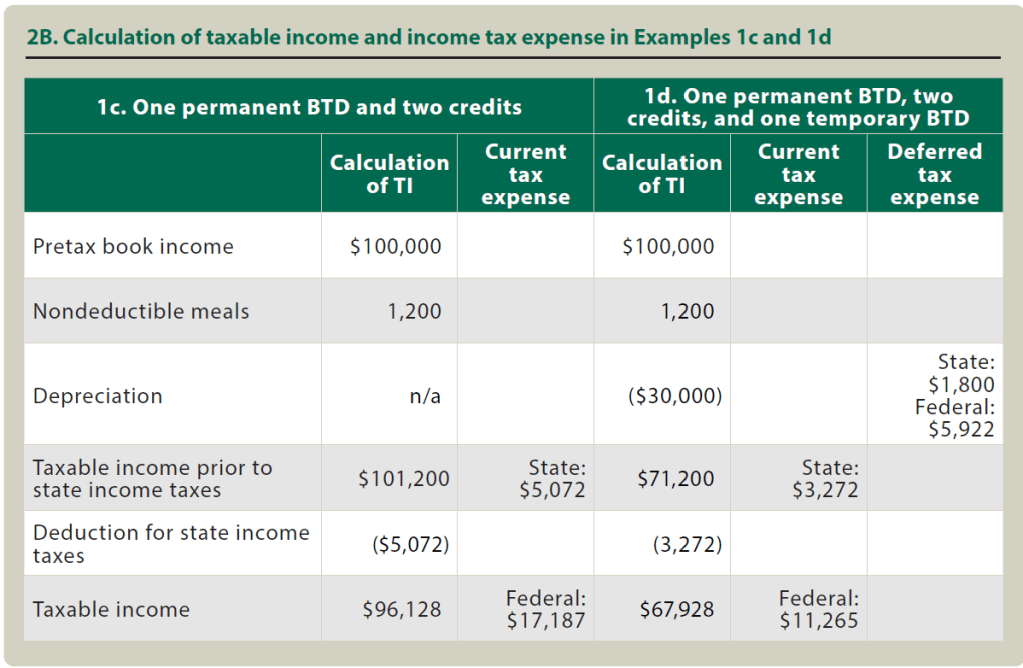

Example 1c: One permanent BTD and two credits: This example retains the permanent BTD from Example 1b and introduces two business credits: a federal credit of $3,000 and a state credit of $1,000. The credit amounts do not affect the calculation of taxable income prior to the state tax deduction, so that is the same as in Example 1b. Instead, the credits directly decrease the current tax expense for each jurisdiction.

The state credit reduces the current state income tax expense from $6,072 to $5,072, but that also means the federal deduction is $1,000 smaller in Example 1c than in Example 1b. Applying the 21% federal rate to the resulting $96,128 of federal taxable income produces a $20,187 pre–credit tax liability, which is reduced by the $3,000 federal credit to $17,187. The first pair of columns in the table “2B. Calculation of Taxable Income and Income Tax Expense in Examples 1c and 1d” presents these results.

Adding federal and state tax expense in Example 1c yields a total current tax provision of $22,259 ($5,072 + $17,187), which is $3,790 lower than Example 1b (not $4,000 lower, which is the sum of the credits). This difference encompasses the $1,000 state tax credit benefit, $210 reduced federal tax benefit from the relatively smaller state tax deduction ($1,000 × 21% = $210), and the $3,000 federal tax credit benefit.

Example 1d. One permanent BTD, two credits, and one temporary BTD: This example retains the previous assumptions and introduces a temporary difference. In this iteration, assume the PBE has tax depreciation in excess of book depreciation of $30,000. Because depreciation for tax purposes is greater than for financial purposes, the PBE will subtract $30,000 from pretax book income to reach taxable income prior to the state tax deduction. The process for calculating state and federal current tax expense is the same as in prior versions of the problem and yields the current provision numbers presented in the second set of columns in Table 2B.

FASB ASC Paragraph 740–10–25–2 requires the future tax effect of an item to be reflected in the current–year financial statements, so the PBE will report the deferred effects of the depreciation differential this year as well. Specifically, it will record a deferred tax liability (a credit) to reflect lower future tax depreciation relative to future financial depreciation and a corresponding increase to deferred tax expense (a debit) as part of the same journal entry.

Because the depreciable asset will be fully expensed for both sets of books over time, it will ultimately face the same interplay between state and federal income tax rates described in Table 1. Thus, the PBE will apply the statutory state rate to the temporary difference to yield a $1,800 ($30,000 × 6%) increase in deferred tax expense from the state–level tax. It will apply the federal statutory rate net of the state benefit to the temporary difference to yield federal deferred tax expense of $5,922 ($30,000 × 19.74%). These deferred expense numbers are shown in the rightmost column of Table 2B.

Footnote disclosure of income tax expense by type and jurisdiction

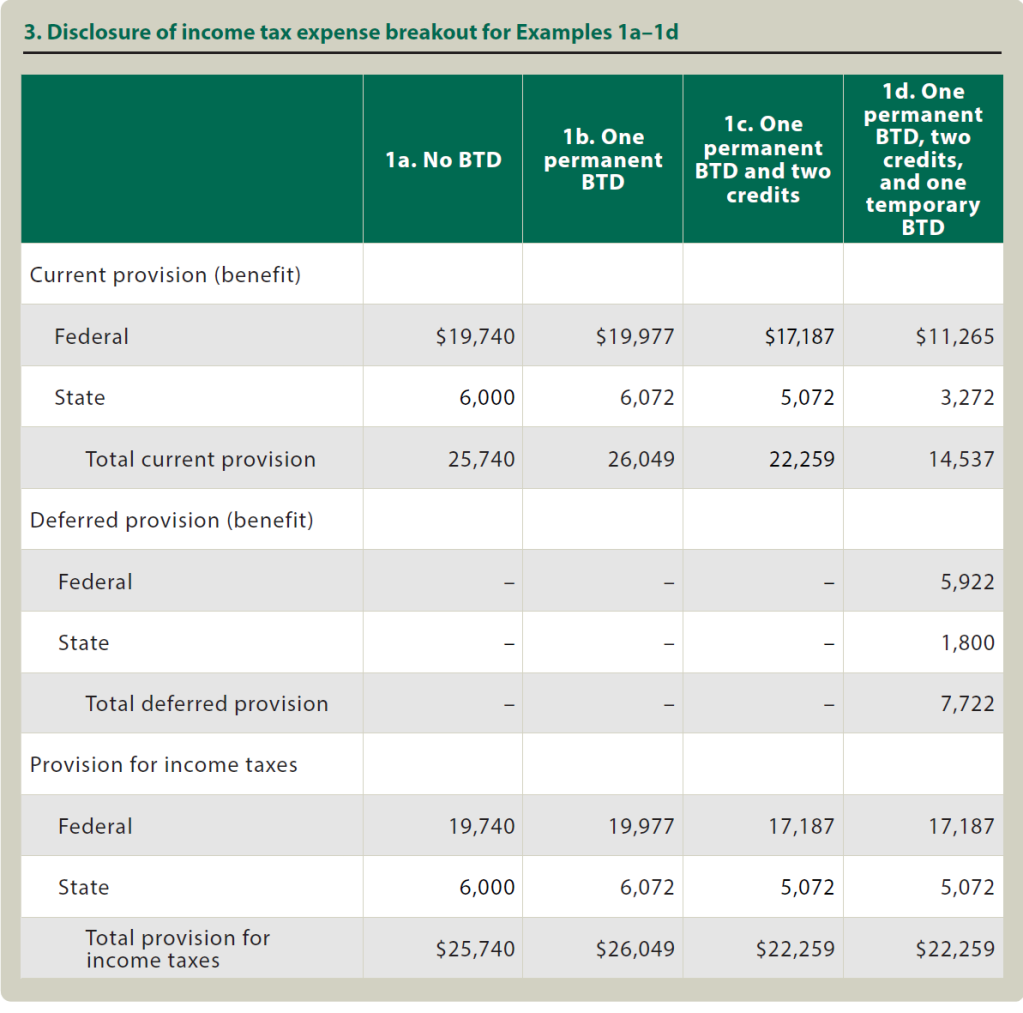

Under ASC Paragraph 740–10–50–10B, PBEs must disclose total income tax expense by federal, state, and foreign components, and many entities also disclose the current and deferred portions in the same way. The information in Tables 2A and 2B provides the data necessary to construct the current/deferred income tax provision breakout, which is presented in Table 3 for every iteration of Example 1. (No foreign line item is shown because the company is domestic.)

One important point to note from the table “3. Disclosure of Income Tax Expense Breakout for Examples 1a –1d” is that the total provision for income taxes between columns 3 and 4 (without and with a temporary difference) is the same; the only difference in those columns is the allocation between current and deferred tax expense. In contrast, permanent differences do affect the total income tax expense provision, illustrated by comparing Examples 1a and 1b in the first two columns of Table 3.

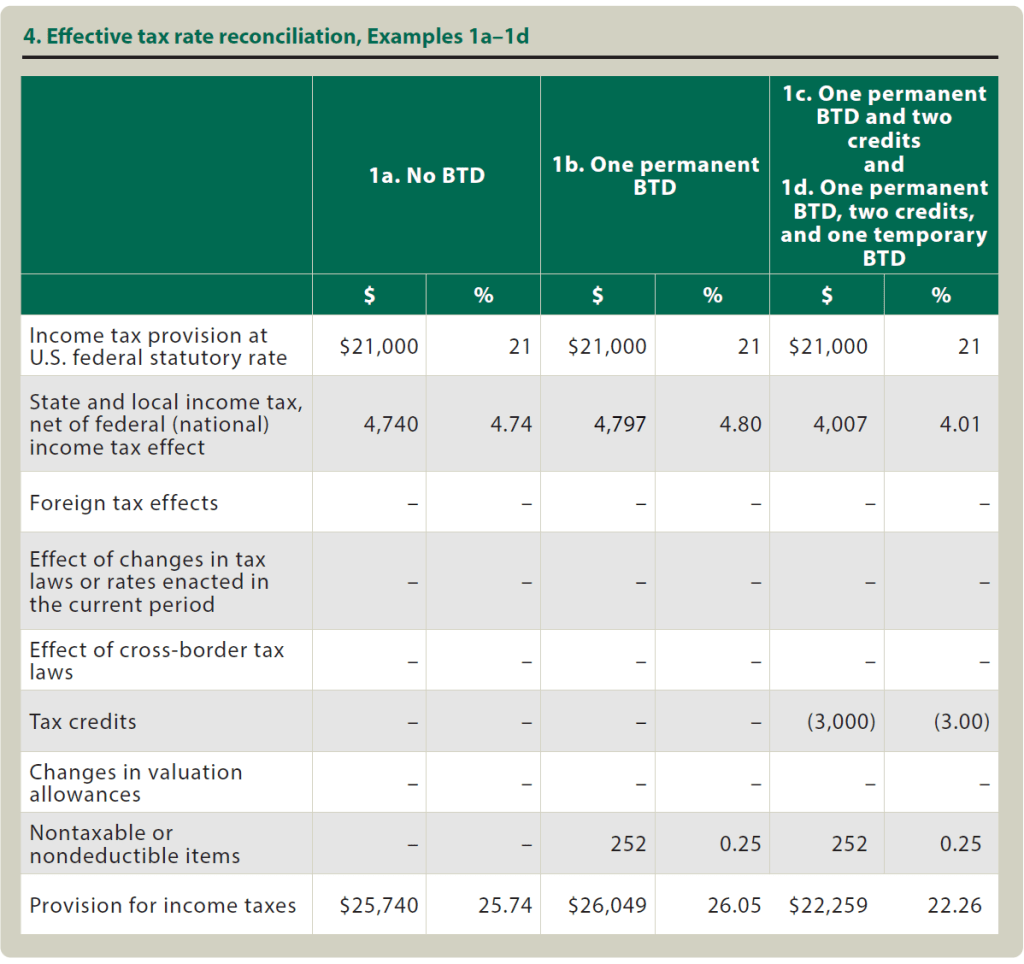

Effective tax rate reconciliation

The effective income tax rate reconciliation, required in tabular form for PBEs per ASC Paragraph 740–10–50–12A, examines the total provision for income taxes using a different approach than the current/deferred breakout. The rate reconciliation starts with a hypothetical calculation of what the income tax expense would be if the entire pretax book income was taxed only, but entirely, at the federal statutory rate in the country of domicile. From that theoretical starting point, the table’s reconciling line items incrementally incorporate the effects of various items, including additional jurisdictions, tax credits, and permanent differences in accounting between financial accounting and tax.

Table “4. Effective Tax Rate Reconciliation,Examples 1a–1d” shows the rate reconciliation for all versions of the cumulative example. Because pretax financial income is held constant throughout the problem, the hypothetical federal tax expense starting point equals $21,000 ($100,000 × 21%) for Examples 1a–1d.

The starting point for the second line item, “State and Local Income Tax, Net of Federal (National) Income Tax Effect,” is theoretically similar to the federal starting point. A company will first multiply its pretax book income by the state statutory rate. From that amount, the PBE will subtract the associated federal benefit of deducting that amount on the federal return. (For a PBE with multiple states, the entity combines the effect of all states into one line item, along with any additional income taxes by localities.)

To calculate the state line item for Example 1a, the PBE will multiply pretax book income of $100,000 by the state’s 6% state rate, yielding $6,000. (Note that this number is also the total state provision in Table 3.) A corresponding $6,000 deduction on the federal return would generate $1,260 of federal tax savings ($6,000 × 21%). Therefore, the net result of taxation at the state level is an increase in total income tax expense of $4,740 ($6,000 – $1,260), reported in the first pair of columns in Table 4. (For all categories in the rate reconciliation, the percentage is calculated by dividing the dollar amount for that category by pretax book income.)

The total provision in the rate reconciliation of $25,740 is the same as in the current/deferred breakout in Table 3. The total expense will always be the same between the two required disclosures because the same underlying items of analysis are simply being approached and aggregated in a different way.

The column “1b. One Permanent BTD” shows the effect of incorporating a permanent BTD in the rate reconciliation. ASC Paragraph 740–10–50–12A stipulates the “nontaxable or nondeductible items” line item only reflects federal effects of the permanent differences, with state effects reported with the state line item. Thus, the “Nontaxable or Nondeductible Items” entry shows the effect of not being able to deduct $1,200 of expense only at the federal level, increasing the tax provision by $252 ($1,200 × 21%). The state cost of nondeductibility is $72 ($1,200 × 6%), and that amount is incorporated into the state tax line item. When added to the $6,000 hypothetical state starting point, the total state tax expense prior to effects of the federal deduction equals $6,072, which again ties to the total state provision for this fact pattern in Table 3. Deducting this amount federally would generate $1,275 of federal tax savings ($6,072 × 21%), so the overall effect of state taxation is $4,797 ($6,072 – $1,275), as shown in the middle pair of columns in Table 4.

To understand the difference in the stateeffects category caused by the permanent difference from another angle, notice from Table 3 that state taxes are $72 higher in Example 1b than in Example 1a ($6,072 instead of $6,000). Once deducted on the federal return, this $72 increase would save the entity $15 in federal income taxes ($72 × 21%). Combining the $72 additional state expense with the related $15 in federal tax savings explains why the state line item in Table 4 is $57 higher for Example 1b than for Example 1a.

The federal and state tax credits (of $3,000 and $1,000, respectively) in Example 1c affect two categories in the rate reconciliation. Similar to the reporting of permanent differences, ASC Paragraph 740–10–50–12A requires that the tax credits line item only reflect federal credits and that state effects be reported as part of the state line item. As such, the “Tax Credits” line item shows the benefit of a full $3,000 reduction in federal tax expense, shown in the last pair of columns in Table 4.

The effect of state credits will be another component of the state tax line item. Specifically, the $1,000 state credit will reduce the hypothetical state tax levy to $5,072 ($6,072 – $1,000; the same state provision total as in Table 3), and that state tax expense would produce federal tax savings of $1,065 ($5,072 × 21%). The net effect of state taxes in this scenario is therefore $4,007 ($5,072 – $1,065), also reported in the final pair of columns of Table 4.

Moving to Example 1d introduces a temporary difference. As previously discussed, while temporary differences shift tax expense between the current and deferred provision, they generate no difference in total income tax expense. Therefore, the PBE’s difference in depreciation will have no effect on the rate reconciliation. As such, the rate reconciliation for Examples 1c and 1d are the same and are presented together in Table 4.

Furthering education

Whether a corporation must pay income tax to a particular state depends on whether it has nexus in that state, a determination that is beyond the scope of this column. For additional discussion on this and other areas related to state taxes and the income tax provision, please refer to Letourneau, “ASC Topic 740 and State Taxes Continue to Require Due Diligence,”55–4 The Tax Adviser 19 (April 2024). For a fundamental discussion of how to construct the income tax provision, please see Evans, “Applying Updated ASC Topic 740 Requirements for the Income Tax Footnote,“56–11 The Tax Adviser 58 (November 2025), which incorporates updated reporting requirements and discusses nontabulated state tax disclosures as well.

One of the most significant resources for learning in a college environment is a visit from a practitioner who assists clients with ASC Topic 740 planning and compliance. In addition to stories from the field or a technical walk–through of mechanics of the provision, the practitioner could provide a software demonstration of a hypothetical client with single–state nexus.

To solidify a technical understanding of the mechanics of the state portion of the income tax provision, the reader is encouraged to work on the additional examples provided in the accompanying Excel file. Example 2a provides a fact pattern with multiple temporary and permanent differences, and Example 2b adds a federal and state credit to the fact pattern. Example 3 provides a scenario with multiple book–tax differences, both permanent and temporary. Similarly, Example 4 incorporates both types of differences between financial and tax accounting, as well as one state–level credit.

After learning the processes in this column, readers will understand the underlying drivers and distinctive approaches of two important portions of the provision footnote. With this knowledge, they will be better able to understand footnote disclosures as well as the calculations performed by software programs used by corporations and accounting firms.

Contributors

Allison L. Evans, CPA, Ph.D., is an associate professor of accounting at the University of North Carolina Wilmington. Annette Nellen, Esq., CPA, CGMA, is a professor in the Department of Accounting and Finance at San José State University in San José, Calif., and is a past chair of the AICPA Tax Executive Committee. For more information about this column, contact thetaxadviser@aicpa.org.

MEMBER RESOURCES

Article

Letourneau, “ASC Topic 740 and State Taxes Continue to Require Due Diligence,” 55-4 The Tax Adviser 19 (April 2024)

Tax accounting resources

FASB ASC 740, Income Taxes: Disclosure Requirements

ASU 2023-09 Income Tax Disclosures

TQA Section 3300.03-.05, FASB ASC 740 Implications of the One Big Beautiful Bill Act

CPE self-study

Income Tax Accounting: Book vs. Tax, Provisions, and SALT — Tax Staff Essentials